Previous article

Previous article

WIRED REPORTS

WHERE OPEN BANKING GOES NEXT

With global momentum building, these are the big ideas set to change our financial lives.

15 minute read

FEATURE

Imagine a world where your financial life runs quietly in the background—smooth, seamless and automatic, like a well-tuned engine. Your banking apps reshuffle funds to prevent overdrafts before they happen. Paying online just involves a frictionless bank-to-bank transfer. All the information about your money is accessible in one spot—no tab-hopping or multiple portals to navigate.

This is the promise of open banking: a global shift in the financial world’s plumbing, unfolding at different speeds and in different ways around the globe. All initiatives, however, share the common aim of creating a financial ecosystem that is more transparent, efficient and ultimately more beneficial to consumers and businesses alike.

At its heart, open banking is about consumers granting third parties access to their banking data—account details, spending history—in exchange for more personalized and innovative financial experiences. The idea is underpinned by application programming interfaces (APIs), a term that refers to rules and protocols that let one program request services or data from another. Think of these as digital bridges that allow multiple parties to share information, managing the associated risk of doing so between themselves.

This kind of data sharing can enable valued-adding services. Account aggregation services, for instance, allow consumers to view and manage multiple financial accounts from different institutions in a single interface. “Open banking is about giving people control over their financial data,” says Helen Child, CEO of Open Banking Excellence. “It democratizes banking information, and ultimately helps you manage your money better.” The same technology also makes it possible to send payments directly between bank accounts, though this currently lacks the same protections as traditional card networks, which are governed by clearly defined rules and facilitate the whole transaction.

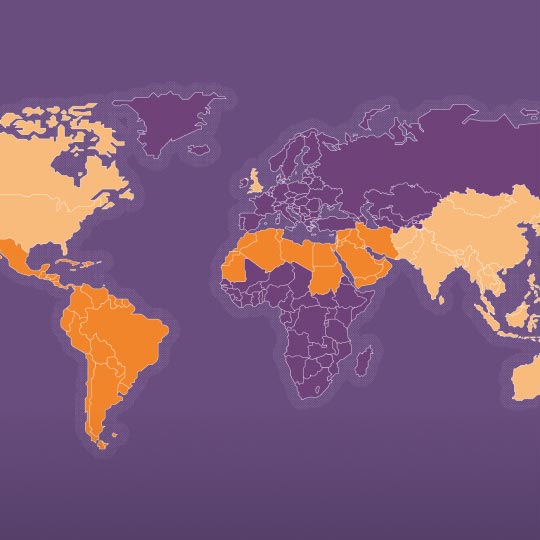

Ninety-five jurisdictions around the world, from the Middle East to Asia Pacific to the Americas, have now adopted some form of open banking initiative.1 One forecast predicts that, by 2029, there will be 645 million total open banking users, up from 183 million in 2025.2

DIFFERENT PATHS TO SUCCESS

Countries vary in their implementation strategies, but approaches fall into two broad camps: market-led or regulation-driven. Both have their own advantages.

Studies show that regulatory-led open banking is typically implemented around 22% faster than the market-led approach.3 The UK and Europe are key examples of places where open banking is governed by robust regulatory frameworks. The Revised Payment Services Directive (PSD2) set the regulatory bedrock for these markets in 2015—this aimed to create a standardized framework for open banking across the EU.4 It mandated banks to allow third-party providers access to customer account information, so long as they have the customer’s consent. This has led to a Cambrian explosion of fintech companies that see an opportunity to transform how money and financial data move around.

The U.S., on the other hand, is an exemplum of market-driven open banking. A vibrant ecosystem has evolved organically over decades, with innovation coming not only from fintech challengers, but also from large banks and other financial services companies. Today, millions of Americans use open banking practices in their financial lives.5 Non-binding principles, such as those issued by the U.S. Consumer Financial Protection Bureau (CFPB) in 2017, have helped the country build a robust data sharing market.6

Despite every market having its own dynamics, open banking as a broad ideal has gained significant traction internationally. Some of the greatest impacts have been felt in emerging markets—places that are in the process of rapid growth and industrialization, increasing economic development and improving standards of living—since it has radically transformed financial inclusion. Take India, for example, where open banking was implemented as part of the “India Stack” of state-run technologies and APIs. The stack included Aadhaar (a national ID scheme), the Unified Payments Interface (an instant payments system), and an Account Aggregators (open finance) framework, all part of an initiative to increase access to financial services. As of March 2025, the country reported more than 550 million accounts had been created.7

“Open banking is about giving

people control over their

financial data.”

“Open banking is just one leg of a three-legged stool. Payments are the second leg, and the third leg is digital identity,” says Ozone API’s Eyal Sivan, who is also the host of the Mr. Open Banking podcast. Digital identity is the online persona or representation of an individual or organization, encompassing attributes such as usernames, passwords and online behavior that are used to authenticate and verify identity in digital interactions and transactions. “The three of them move together, and regions that have had those three things as separate initiatives are starting to realize these are fundamentally related. Places like India completely understood that early on.”

GET READY FOR THE FUTURE

Interest in open banking is growing sharply. “We are now in a situation where everyone around the globe is talking about how they can do open banking and how fast they want to go,” says Stefano Vaccino, CEO of Yapily, a UK-based open banking API platform. “A few years ago, it was ‘if,’ now it’s actually ‘when’ and ‘how fast.’ It is happening everywhere.”

A few recent developments are attracting particular attention. The upcoming PSD3, which is currently under development, aims to harmonize open banking rules across the European Economic Area to create a better user experience by introducing common standards across the continent and simplifying the ability to access user data.

“Common shared standards for the secure exchange of financial data, based on your consent, means that no matter who you’re dealing with in the financial ecosystem—big bank, small bank, credit union or fintech—all of them work the same way,” says Sivan. He likens this to the way the USB or HTTP standards work in computing. Nobody owns them, but everybody can use them.

“It changes everything,” he says. “The second you introduce common open standards, you lower the cost of entry, you invite many more participants to play and you create a common foundation for a whole universe of innovation to be built.”

The desire for common standards has also put open banking in the spotlight for America recently, too. Although American progress has been driven primarily by the market, in recent years regulators have aimed to formalize data sharing practices.

The CFPB finalized its data aggregation rule at the end of 2024. However, the CFPB is reconsidering the rule at the end of 2025 in light of litigation, and is now reviewing its statutory authority and potential risks to data privacy and information security arising from its original rulemaking.8 In some quarters this has caused consternation, but others have accentuated the positive.9

“The U.S. actually has the best open finance market in the world,” argued one notable fintech commentator, who contended that it now should embrace its late-mover advantage in light of the fact that “where robust regulation exists, open finance hasn’t lived up to its promise,” and seize the moment to build “a better ecosystem even without regulation.”10 In particular, they continued, the U.S. system should take a cue from the card networks, which realized that a clear liability framework was essential to develop user confidence in the system—and put this in place themselves.11

As open banking regimes emerge and mature around the world—whatever course they chart—the prospect grows of greater standardization and interoperability across borders, and with it a more globalized era of financial services comes into view.

So, the question is: As open banking quietly, steadily rewires the financial system, what are the emerging trends that stand to reshape our financial lives in the years to come?

“A few years ago, it was

‘if’, now it’s actually

‘when’ and ‘how

fast.’ It is happening

everywhere.”

PAY BY BANK’S NEXT FRONTIERS

Look around. Most likely, every object you can see has at least one payment attached to it. But most people never give payments a second thought. Payments just happen.

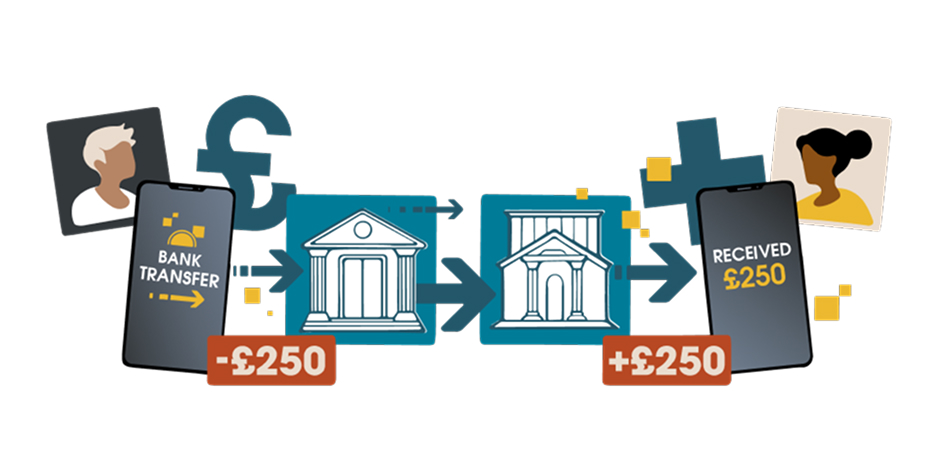

The reality is that behind the scenes there is a complex web of different systems and infrastructure providers, known as “rails,” that operate in concert to move your money into the vendor’s account. Account-to-account (A2A) payments, also known as “pay by bank,” allow people to pay merchants directly at a lower cost to the merchant.

The name may be confusing because every payment goes ultimately from one account to another. But A2A refers to doing that via national clearing systems. While it has long been possible to send money between bank accounts via an online transfer, this hasn’t been a standard way to pay. Open banking A2A payments make the process quicker and less manual, by mandating the automatic sharing of the necessary information to initiate a payment.

There are other benefits as well. Since it’s facilitated by banks, A2A enjoys bank-grade security, such as strong customer authentication. And as countries adopt real-time payment systems, A2A also becomes a notably fast way to transact. “This is why open banking adoption will be very significant in the U.S.,” says Vaccino. “Payment schemes were super slow for many years. But you now have real-time payment rails such as ACH, RTP and FedNow, and we are seeing banks adopting them.”

“ There is a cheaper,

simpler way

to move money.”

Open banking payments are growing. Simone Martinelli, CEO of open banking payments company Volume, says A2A adoption in the UK was “extremely low” in the first five years of open banking, but that is now rapidly changing. “Since the start of 2023, we’ve seen growth above 20 percent month-on-month, reaching a peak of 40 percent. So it is skyrocketing,” he says. In absolute terms, however, they are still relatively small fry for consumer purchases. Globally, just seven percent of e-commerce transactions happen via A2A.12 Yet proponents are bullish. “I think we will move to instant, easy payments over national infrastructure,” says Todd Clyde, the CEO of open banking payments fintech Token.io.

So, what will it take to get from here to there?

One aspect is elevating the user experience. Some companies are exploring how QR codes, for instance, could bring A2A to physical point-of-sale. Others are addressing the online A2A experience. Volume, for example, provides a “one-click” button for online merchants to integrate into their checkouts with minimal setup. This connects to users’ banking apps, allowing them to initiate a payment with just one action rather than moving between multiple screens and apps. Others still are convinced that integrating open banking with digital wallets is the key, noting that countries with large numbers of A2A transactions are ones where those payments happen not via open banking protocols, but through digital wallet-based schemes.13

Another crucial aspect is security. Of particular importance is how dispute resolution mechanisms work under A2A payments. Credit cards hold a strong reputation for security and consumer protections against unauthorized payments fraud, with part of their costs going directly to fraud prevention and making customers whole, even if the money is not recovered from a merchant or scammer. By definition, no cards are involved in an A2A payment, meaning those safeguards don’t exist. An argument could be made that the reduction of friction—and the interconnected nature of open banking through a web of third parties—in fact presents new opportunities for cybercrime, as fraud prevention is more challenging in a real-time context.

Ian Morrin, Head of Payments at open banking platform Tink, says that this is an area where progress is being made. “When it comes to improving protections, there is strong industry momentum at the moment,” he says, noting that in June 2025, the next stage of Visa A2A was announced.14 “That’s bringing an enhanced framework to Pay by Bank, and Tink is excited to be one of the first members of this new solution. Visa A2A connects banks and third-party providers under a common rulebook, which will increase buy-in and boost consumer trust in Pay by Bank. UK consumers and businesses using Pay by Bank will benefit from a similar level of protection typically associated with card payments.”

The jury’s out on how long A2A could take to go mainstream in consumer payments, and what it means for the payments landscape of the future. Clyde predicts, simply: “There is a cheaper, simpler way to move money.”

FINANCIAL INCLUSION

Lending has one universal truth: Giving out the money is easy, but getting it back is difficult. The greater the uncertainty, the higher the interest rate to compensate for the risk. Traditionally, lenders have used credit bureaus to score this risk as well as to cut out “bad” borrowers.

Misha Esipov, CEO of credit analytics company Nova Credit, says the existing credit bureau system does not fairly serve a large share of the global population. He estimates more than 100 million Americans alone are “misunderstood” by the credit bureaus, and shut out from access unnecessarily. This includes the credit-invisible segment—those with a “thin file” or no file at all—who are often recent immigrants to a country, young adults, students, or people later in life. Often this segment has real assets, but hasn’t been consistently borrowing to be able to show they can afford financing to buy, say, a car.

This is an area where open banking can help. One of the most compelling use cases is in promoting financial inclusion, in particular by bringing credit products to users currently excluded from them.

“It involves using deposit data and transaction-level data to create a more complete picture of someone’s financial health,” says Esipov. “Some people have also made mistakes through missing a payment here or there, which tanks their conventional credit score, but their underlying financial health is great. They generate consistent income, they’re saving, they never reach overdraft.”

Transaction data—as opposed to a credit score—can allow lenders to more accurately see whether someone can afford a loan, by modeling and forecasting cash flows in real time. This lets lenders serve a wider range of customer segments while also protecting their own balance sheets. The opportunity is greatest in places such as India and Brazil because credit bureau coverage is only as good as consumer credit penetration. Approximately 119 million Indians monitor their credit out of a population of 1.4 billion.15,16

“You could see a world

where the whole

credit bureau system

gets replaced with

open banking.”

Lending based on transaction data is itself not new. But in the past this was only an option if you were borrowing from the bank that looked after your money. This new approach changes the status quo, but also, in turn, has the potential to improve the picture for traditional lenders. In the UK, open banking-based lender Salad, for instance, helps borrowers enter the established financial system. “We re-report data back into the credit reference agencies, so we can help borrowers build their credit score,” says Alex Marsh, Chair of Salad.

So, how will this play out in the longer term? Esipov thinks there’s no reason why the open banking approach couldn’t become the norm. “You could see a world where the whole credit bureau system gets replaced with open banking. If you were to rebuild the whole system now, you would rebuild it using open banking,” he says. “Because all the information about who you are and how you earn, and your financial health, is captured in your bank account.”

If this happens, he says, it would be transformative for so many. “Access to capital accelerates time. You can use your potential from the future to give you the ability to move faster in the present. The availability of funds and capital, and credit access, can accelerate economic mobility and a whole host of other things. That’s why the mission behind credit access is so important.”

NEXT, OPEN FINANCE... THEN OPEN EVERYTHING

Listen to those in the open banking space, and two terms are constantly repeated: open finance and open everything.

While it is still early days for the rollout of open banking, regulators, entrepreneurs and investors have been quick to foresee the expansion of the model to go beyond basic account and transaction data and to include a wider variety of financial sources and products. This idea is widely called “open finance.”

Open finance would be made possible via the same data sharing mechanisms and consent-based flows governing open banking, only covering a wider scope of data. It’s the network that would grow, not the technology that would change. Clearly, easy user control of access to data by third parties would be key to building sufficient trust for this to be possible.

“The nub of it is connecting more than just a basic bank account, whether that’s access to your investments, your mortgage, your credit card or tax information,” says Paul LaRusso, CEO of open finance startup Akoya. “It’s more inclusive of your whole financial life.”

What started as a way to transform the banking sector is therefore expected to broaden into additional market segments like wealth management, insurance products, pensions and other investments.

So what’s stopping this from happening right now? Practicalities. The financial services industry is one of the most heavily regulated and intricately organized sectors globally. The complexity problem is further compounded by the typically slow speed of change and the ongoing need to integrate with legacy systems.

These are not seen as insurmountable barriers, however. In the UK, for instance, many are hoping emerging regulations, such as the Data (Use and Access) Bill, will help. Others argue that even with open banking, building other digital infrastructure is also necessary if new entrants and products are to surface.

But we know that solving the issue is, in principle, possible. In Brazil, which established open banking later than the UK and EU, the expansion into open finance has already begun.

“Today we have 57 million people participating in the open finance system,” says Luciana Kairalla, General Manager of Open Finance at Nubank, the Brazilian neobank with more than 123 million customers across Latin America.

The “open everything”

thesis is that

incorporating even more

data sources confers

ever greater benefits.

One of the chief motivators is, once again, credit. By incorporating even more aspects of someone’s financial picture—more than simply transaction history and cash flow—more people can gain access to the credit they need. “The message that ‘by sharing more data, we might be able to give a more compelling credit offer to you’ was a message that was really winning with most of our customers, because liquidity is really important for the Brazilian population,” she says.

It is not hard to imagine how many of the promises—and risks—of AI could feed into the open finance vision. Its ability to process natural language may allow it to function as a personal financial advisor. “I can see a world where AI becomes more of a decision-maker and action-taker, with permissions and guardrails that the consumer has established,” says LaRusso. “An example of that could be looking for the best interest rate or yield on an account.”

Think how much time and money that could save. Today, consumers might get notifications of interest rate changes, but researching better rates and switching accounts is an arduous process—and many don’t wish to spare the time. “You could see something in the future where you’ve given permission to a secure artificial intelligence service to not only find the deal but execute the switch on your behalf,” says LaRusso.

And why stop at strictly financial data? The “open everything” thesis is that incorporating even more data sources confers ever greater benefits. Health data might feed into life insurance products to bring you a lower premium, or into pension products to help you more accurately plan for old age. Utilities data could lead to lower bills for consumers by helping them to more easily—perhaps even automatically—compare prices and switch providers.

In Australia, open everything is already becoming reality.17 The country has introduced open data standards across its economy to encompass multiple sectors such as energy and telecoms. “Once you bring all these different data sets together, you exponentially increase the number of use cases you can support, because you’ve got a lot more data to work with,” says Ozone API’s Eyal Sivan.

In fact, he says, the sky’s the limit. Once people get used to sharing their data based on their consent, and controlling how their data is used, they may naturally say: Wait a minute, what about my social data? What about my search data? What about my e-commerce data? Isn’t that also mine?

“When we get there, well, that’s a completely new internet,” he says. “Open banking is very much the thin end of the wedge.”

SOURCES: WWW.JPMORGAN.COM/PAYMENTS-UNBOUND/SOURCES

ILLUSTRATION: ANDREW NYE

Related content

MAGAZINE

Volume 6: Open Banking Is Just Getting Started Volume 5: Game Changer Volume 4: Ready Payer One Volume 3: Bank to the Future Volume 2: The New World of Commerce Volume 1: The Money Revolution Browse all articlesWEBINARS

View all webinarsMORE

Download a copy of volume 6 Get a physical copy of volume 6 Become a featured client J.P. Morgan Payments