Previous article

Previous article

J.P. MORGAN PAYMENTS

Payment innovation will drive financial inclusion

4 minute read

ESG matters more than ever, and new finance tools will have a powerful role to play

J.P. MORGAN OP-ED

The spotlight on environmental, social and governance (ESG) factors is rapidly transforming all industries. Most companies are aiming to be more climate-conscious, socially-active and relevant in the eyes of their consumer and investors. It’s changing investment, too. According to J.P. Morgan research, total ESG assets under management are now more than $7 trillion.

However, the ESG landscape is continually shifting and, as these goals come into sharper focus, companies are also becoming more nuanced in how they address sustainability. Rather than focus on ESG as a catch-all term, businesses are designing specific initiatives to produce tangible outcomes in each of those three areas, and are looking at the bigger picture of how those outcomes align with agendas such as the United Nations’ Sustainable Development Goals (UN SDGs).

Crucially, the way businesses handle payments can play a key role in aiding to reduce inequality, drive economic growth and improve lives. New kinds of payment tools can help promote financial inclusion, especially among low-income earners, micro-communities or those in developing countries. Two key ideas—and places where companies can really make a difference—are earned wage access and remittances.

Earned wage access

Money earned is often spent more rationally than money loaned, and earned wage access (EWA) can help a company’s employees gain faster and more flexible access to the money they earn. Employers do this by smoothing out the income cycle to reduce reliance on costly payday loans or other short term credit such as overdrafts and credit cards. Typically, an EWA solution will integrate with an employer’s payroll system via an app that provides visibility of wages earned for the month, as well as a tool that allows workers to draw down wages before payday. Functionality can include services such as using earned wages to pay utility bills. In South Africa, J.P. Morgan research observed that users were given access to 25 percent of their salary through an EWA platform, but that only 12-14 percent of funds were actually used on average. This highlights how earned wages are used more conservatively than borrowed money and can help promote financial literacy.

EWA effectively provides the flexibility found in the gig economy—such as real-time payouts— within the traditional corporate payroll space. In a time of inflation and squeezed living standards, these tools can help individuals better manage their living expenses, allowing them instant access to money earned, and avoid unnecessary overdraft fees or late payment charges.

Remittances

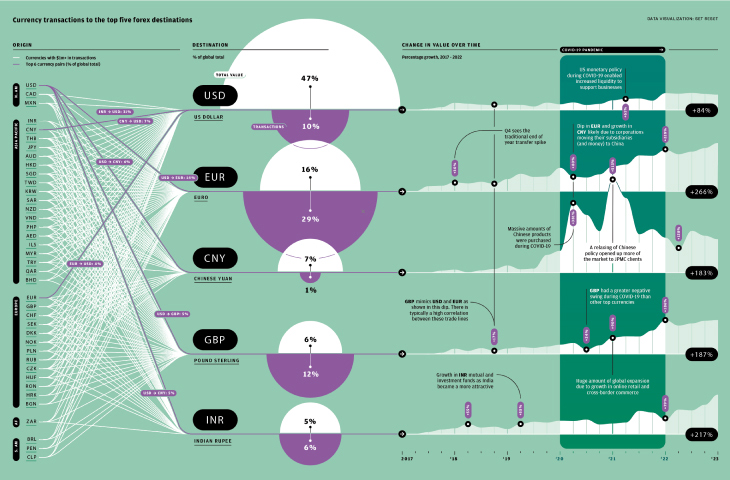

Banks themselves also have a role to play in inclusion. According to the World Bank, global remittances to middle- and low-income countries totalled $626 billion in 2022. These remittances are typically non-commercial payments, sent by foreign workers to family members in their home countries, and can often form key pillars of the economy of these countries. For example, monthly remittances to Sri Lanka are almost $400 million. Low fees on these individual, low-value transactions are especially crucial to the senders—every cent incurred in fees could make a difference to their family back home.

Time is also of the essence. However, cross-border payments are complex and time-consuming, as banking systems are usually closed-loop structures that are specific to each county, with little integration. Banks have been historically slow in addressing these consumer-to-consumer remittance problems, yet a raft of new digital payment tools are being made available by financial institutions, and tech companies are making it much easier and faster to send money across borders. These tools are far more secure than informal channels and can be the first financial product used by many people on lower incomes. They can also form a stepping-stone to accessing further financial services and achieving better financial health.

Remittances can be crucial for families who struggle to pay for basics such as food and rent. A digital remittance solution can cut transfer times by days, which means recipients are able to access the money much more quickly.

At the same time, businesses also need ways to transfer money across borders that mimic the ease of domestic payments systems, with low fees and transparent processes. This can be vital for small businesses with operations, suppliers or workers in multiple countries. The longer term upshot? Sustained and inclusive economic growth.

Providing fast and secure ways for people to receive payments, whether accessing their wages or receiving remittances, can play a major role in supporting equitable development and encouraging global growth.

J.P. MORGAN