Previous article

Previous article WIRED REPORTS

What’s next for Asia-Pacific?

5 minute read

Asia-Pacific (APAC) is a region like no other in the world, being home to a multitude of currencies, languages —and

regulatory regimes

REGIONAL TREND WATCH

Macroeconomic volatility and uncertainty, higher cost of funding, and the need to diversify supply chains are particular concerns for businesses operating in the APAC region. But what sets APAC apart is the access to enormous technology talent pools that are adept at resolving problems through the use of artificial intelligence, process automation, and data analysis.

One result of this is the region’s leadership in adopting new real-time payments methods, plus API and cloud-based payments technologies, which has led to the emergence of popular digital wallets and sophisticated digital banking providers. These in turn are transforming e-commerce and leading the swift rise of new business approaches, such as

direct-to-consumer, usage-based pricing, and subscription models. Meanwhile, online platforms that once catered to a single niche are expanding through partnerships with firms in other sectors, giving rise to multi-industry, region-wide ecosystems.

This has made the region a cradle of innovation when it comes to fintech, and a must-follow space for those interested in where payments go next. Here are six telling developments..

Click on a number below for more information on each country

1

India

Could its real-time payments system go global?

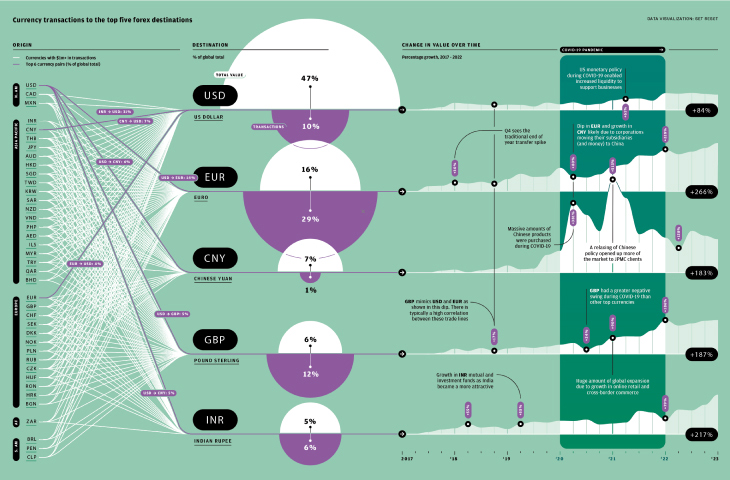

India’s Unified Payments Interface (UPI), which allows instant peer-to-peer and person-to-merchant payments via mobile devices, is fast expanding internationally through partnerships in several countries including Singapore and the UAE. The National Payments Corporation of India (NPCI) is also enabling UPI capabilities using phone numbers for accounts in India held by Indian residents residing overseas. Developed by the NPCI in 2016, UPI is a major reason that India leads the world in real-time payments (RTP) – an estimated eight billion RTP transactions happen every month. The country’s central bank also recently launched India’s Central Bank Digital Currency (CBDC), the digital rupee. While still in its initial stages, a digital rupee on an interoperable blockchain can help facilitate real-time cross-border transactions without intermediaries and usher in an era of cheaper, more efficient currency management.

2

MAINLAND CHINA

Moving towards digital currency

With the expansion of the digital renminbi or ‘e-CNY’ pilot for retail users in 23 cities in 2022, China became the largest economy to offer a Central Bank Digital Currency (CBDC) at scale. Users are now able to access their e-CNY in wallets on mobile apps. In parallel with the launch, the country’s popular online platforms are now allowing for e-CNY as a method of payment. Supported by the country’s existing retail payment infrastructure, the e-CNY system will help bolster China’s digital economy through a more secure form of currency, enhance financial inclusion, and drive greater efficiency. e-CNY has so far been used primarily for domestic retail payments, but there is potential for adoption across corporate and personal businesses in the near future.

3

HONG KONG SAR, CHINA

EXPANDING RMB TREASURY CAPABILITIES

A major international financial center in Asia, Hong Kong serves as an important gateway to mainland China and is the largest center for conducting offshore renminbi (CNH) financing activities. As the renminbi (RMB) grows in popularity as an international payment currency, there is increasing demand from both foreign multinationals and China headquartered companies for CNH payments capabilities, such as flexible CNH FX rate optimization. The city’s central bank is also committed to expanding RMB liquidity in the region through enhancements to the RMB Liquidity Facility, as well as introducing additional risk management products such as Swap Connect.

4

SINGAPORE

BLOCKCHAIN IS ENABLING INNOVATION

Singapore continues to make strides when it comes to pioneering innovative ideas across the payments ecosystem. In 2016, the Monetary Authority of Singapore (MAS) along with industry players including J.P. Morgan, began experimenting with blockchain under the banner ‘Project Ubin’. Over five years, this explored how distributed ledger technology (DLT) could be used in everything from decentralized netting of payments to the ‘delivery-vs-payment’ (DvP) settlement process commonly used for securities. The success of this work is paving the way for commercialization such as a joint venture among DBS Bank, J.P. Morgan, Temasek and Standard Chartered which plans to operate a blockchain based, multi-currency clearing and settlement platform called Patrior. Now, the MAS continues to work on key initiatives to further advance DLT usage such as instant cross-border exchange and settlement of foreign currency transactions, as well as the programmable digital Singapore dollar. Current work on decentralized finance (DeFi) applications looks at how tokenized government bonds, Japanese yen and Singapore dollar deposits can demonstrate new models of trading, clearing and settlement.

5

JAPAN

NEW IDEAS CHANGING CASH DOMINANCE

Despite a plethora of digital payment choices in addition to credit and debit cards, cash remains the dominant medium of exchange in Japan. That is likely to change as the authorities have introduced a “Cashless Vision”with an aim to increase cashless transactions to 40 percent by 2025. To help achieve its goals, the Japanese government is set to introduce a system that will allow companies to pay a portion of salaries into e-wallets on mobile devices by spring 2023, alleviating the need to draw cash from ATMs. Such convenience coupled with discounts offered by these new payment providers will likely help drive the shift towards a cashless society. The transition to cashless payments is also expected to help overseas workers receive salaries without needing to open bank accounts, further expand financial services innovation in the market, and promote growth.

6

AUSTRALIA & NEW ZEALAND

ALTERNATIVE PAYMENTS METHODS SURGE

The digital payment landscape in Australia and New Zealand has undergone significant changes in recent years. Cash and checks have been largely replaced as major forms of payments, with digital alternatives such as e-wallets, real-time peer-to-peer transfers and ‘buy now, pay later’ (BNPL) services achieving mainstream adoption. According to the Australian Treasury, almost half of the country’s population today make contactless payments using mobile and wearable devices. Real-time payments, launched in 2018, already account for a third of total peer-to-peer payments, and there are more than five million active BNPL users today. The trend towards a more digitized payments ecosystem is only expected to grow, driven by the rise in e-commerce, high mobile penetration and changing consumer behaviors that favor more instantaneous as well as convenient forms of payments.

Click on a number below for more information on each country

Could its real-time payments system go global?

India’s Unified Payments Interface (UPI), which allows instant peer-to-peer and person-to-merchant payments via mobile devices, is fast expanding internationally through partnerships in several countries including Singapore and the UAE. The National Payments Corporation of India (NPCI) is also enabling UPI capabilities using phone numbers for accounts in India held by Indian residents residing overseas. Developed by the NPCI in 2016, UPI is a major reason that India leads the world in real-time payments (RTP) – an estimated eight billion RTP transactions happen every month. The country’s central bank also recently launched India’s Central Bank Digital Currency (CBDC), the digital rupee. While still in its initial stages, a digital rupee on an interoperable blockchain can help facilitate real-time cross-border transactions without intermediaries and usher in an era of cheaper, more efficient currency management.

Moving towards digital currency

With the expansion of the digital renminbi or ‘e-CNY’ pilot for retail users in 23 cities in 2022, China became the largest economy to offer a Central Bank Digital Currency (CBDC) at scale. Users are now able to access their e-CNY in wallets on mobile apps. In parallel with the launch, the country’s popular online platforms are now allowing for e-CNY as a method of payment. Supported by the country’s existing retail payment infrastructure, the e-CNY system will help bolster China’s digital economy through a more secure form of currency, enhance financial inclusion, and drive greater efficiency. e-CNY has so far been used primarily for domestic retail payments, but there is potential for adoption across corporate and personal businesses in the near future.

EXPANDING RMB TREASURY CAPABILITIES

A major international financial center in Asia, Hong Kong serves as an important gateway to mainland China and is the largest center for conducting offshore renminbi (CNH) financing activities. As the renminbi (RMB) grows in popularity as an international payment currency, there is increasing demand from both foreign multinationals and China headquartered companies for CNH payments capabilities, such as flexible CNH FX rate optimization. The city’s central bank is also committed to expanding RMB liquidity in the region through enhancements to the RMB Liquidity Facility, as well as introducing additional risk management products such as Swap Connect.

BLOCKCHAIN IS ENABLING INNOVATION

Singapore continues to make strides when it comes to pioneering innovative ideas across the payments ecosystem. In 2016, the Monetary Authority of Singapore (MAS) along with industry players including J.P. Morgan, began experimenting with blockchain under the banner ‘Project Ubin’. Over five years, this explored how distributed ledger technology (DLT) could be used in everything from decentralized netting of payments to the ‘delivery-vs-payment’ (DvP) settlement process commonly used for securities. The success of this work is paving the way for commercialization such as a joint venture among DBS Bank, J.P. Morgan, Temasek and Standard Chartered which plans to operate a blockchain based, multi-currency clearing and settlement platform called Patrior. Now, the MAS continues to work on key initiatives to further advance DLT usage such as instant cross-border exchange and settlement of foreign currency transactions, as well as the programmable digital Singapore dollar. Current work on decentralized finance (DeFi) applications looks at how tokenized government bonds, Japanese yen and Singapore dollar deposits can demonstrate new models of trading, clearing and settlement.

NEW IDEAS CHANGING CASH DOMINANCE

Despite a plethora of digital payment choices in addition to credit and debit cards, cash remains the dominant medium of exchange in Japan. That is likely to change as the authorities have introduced a “Cashless Vision”with an aim to increase cashless transactions to 40 percent by 2025. To help achieve its goals, the Japanese government is set to introduce a system that will allow companies to pay a portion of salaries into e-wallets on mobile devices by spring 2023, alleviating the need to draw cash from ATMs. Such convenience coupled with discounts offered by these new payment providers will likely help drive the shift towards a cashless society. The transition to cashless payments is also expected to help overseas workers receive salaries without needing to open bank accounts, further expand financial services innovation in the market, and promote growth.

ALTERNATIVE PAYMENTS METHODS SURGE

The digital payment landscape in Australia and New Zealand has undergone significant changes in recent years. Cash and checks have been largely replaced as major forms of payments, with digital alternatives such as e-wallets, real-time peer-to-peer transfers and ‘buy now, pay later’ (BNPL) services achieving mainstream adoption. According to the Australian Treasury, almost half of the country’s population today make contactless payments using mobile and wearable devices. Real-time payments, launched in 2018, already account for a third of total peer-to-peer payments, and there are more than five million active BNPL users today. The trend towards a more digitized payments ecosystem is only expected to grow, driven by the rise in e-commerce, high mobile penetration and changing consumer behaviors that favor more instantaneous as well as convenient forms of payments.