Previous article

Previous article

WIRED REPORTS

What’s the future for Western “super apps”?

3 minute read

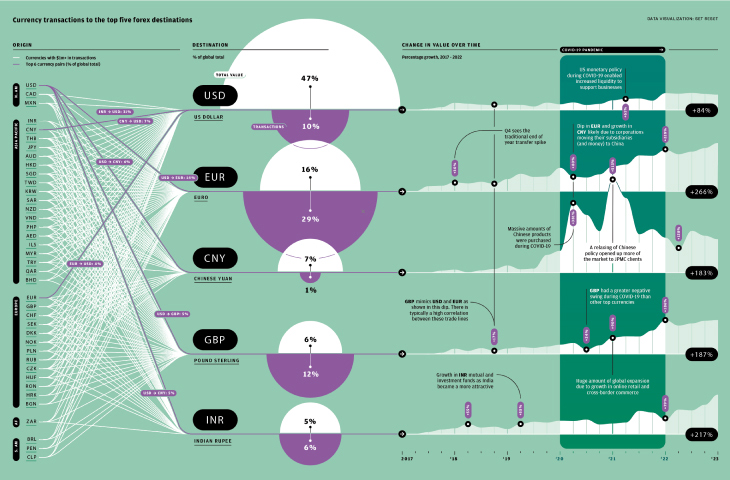

TWO SIDES OF THE SAME COIN

Super apps create a single interface to unify a broad ecosystem of service such as messaging, e-commerce and transport. With consumers making all of their purchases within one walled garden, the user engagement and data benefits are obvious and enormous. These apps have become a major part of the Chinese technology landscape, so we asked two leading experts: Could the concept successfully break through in Western markets?

Related Solution

Commerce solutions

Our commerce solutions allow you to create an amazing shopping experience without sacrificing resiliency and peace of mind.

Don’t expect Asian-style super apps any time soon...

“The first reason is that the U.S. has a history of a more fragmented app market. Generally speaking, the country has a lot more competition and less customer capture by any one app today. This fragmentation also applies to many Western markets more broadly. And there is just this general aversion in the West to knowingly relying on a single firm for the majority of everyday products and services.

The West also has an aversion to feature bloat. I think Western customers generally like less clutter than Asian customers when it comes to interfaces and apps. The other consideration is the comparatively slow adoption of digital payment systems [in the West]. A decent definition of a super app would include a common payment system embedded in the app. In the U.S., in terms of people’s willingness to use digital mechanisms to transact, I think things have come a long way. But even there, there’s still some aversion: Certainly a lot more so than in Asia. And in areas of continental Europe, cash is still the norm.

Finally, there’s the regulatory landscape. At the time the super apps started out in China, there were far fewer restrictions than you see in Western countries. That allowed them to become large, but it’s not something that the Western companies have the luxury of avoiding today.

...But there’s hope that we might see “quasi-super” versions

“The business-to-business side is where we’re likely to see this play out first. The U.S. has 30 million small businesses, give or take. To run a business, they have to go through selling, marketing, managing inventories, accounting and legal forecasting among other considerations. That’s currently spread across multiple apps. So app companies realize the value in stitching all these together in one bucket. Companies are already trying to get into this space.

On the business-to-consumer side, people have been moving into the super app space, or what I would call “quasi-super apps”, for a fairly long time.

By 2025, we’re likely to start seeing some of the changes in this space play out at scale. You’re definitely seeing the development of super apps in travel and hospitality. You have ride-hailing companies moving from transport and food delivery into hospitality. You see it in entertainment, where you have audio-streaming companies going beyond radio into podcasts and a bunch of other services. Then you have logistics more broadly, where e-commerce giants are trying to push services like medical consultation, pharmacies, and groceries, in addition to content streaming and e-commerce, which takes it more into the super app space.

Regulations are making it harder for tech companies to profit from acquiring third-party user data, or sharing their own data with other companies. But you don’t have an issue with that regulation if all the apps are running on your infrastructure.”

SOURCES: AS PER WIRED, MAY 2024

ILLUSTRATION: ADOBE STOCK / MACROVECTOR

MAGAZINE

Volume 5: Game Changer Volume 4: Ready Payer One Volume 3: Bank to the Future Volume 2: The New World of Commerce Volume 1: The Money Revolution Browse all articlesWEBINARS

View all webinarsMORE

Download a copy of volume 5 Get a physical copy of volume 5 Become a featured client J.P. Morgan Payments