It takes a village to elevate the shopping experience. Brand managers, customer experience directors, gig workers and small businesses all play a crucial role, and the last member of this team is the treasurer. That’s because payments are a strategic enabler for many new shopping experiences, and treasurers are critical to bring many of these growth opportunities to life. They also pose considerable challenges for treasurers – understanding the payments model needed to commercialize new sales channels, managing new flows and exposures from these channels, and mitigating working capital impacts from supply chain shifts. Treasurers’ role in navigating the impacts of the growth initiatives places them in a critical seat at the strategic table, influencing and guiding their organization.

Expanding sales channels

As customer expectations shift at an accelerated rate, businesses should expand their sales channels to reach new customers and markets. Incorporating payments into the end-to-end experience is necessary from checkout to navigating cross-currency considerations.

One example of this innovation is within the fast-moving consumer goods (FMCG) sector. Most brands are engaged in a business-to-business (B2B) model within this space, but they’re moving to direct-to-consumer (D2C) models. In the B2B model, a toothpaste brand may have received a single $1 million payment from Walmart in exchange for providing dozens of toothpaste crates. In the D2C model, they may experience 500,000 customers across the globe paying $2 for a single product of toothpaste. The treasurer has to receive consumer payment methods such as credit cards, digital wallets and alternative methods of payments in addition to managing the impacts of a significantly higher-volume and lower-value flow.

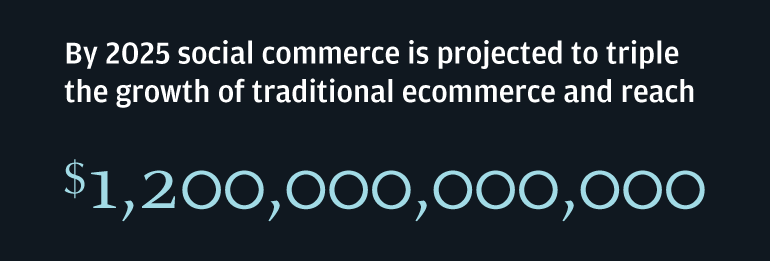

By 2025 social commerce is projected to triple the growth of traditional ecommerce and reach

$1,200,000,000,000

Below are some key considerations:

-

Expanding to multi-party commerce:

Businesses are creating platforms such as marketplaces and ecosystems that serve as a one-stop-shop for consumers. Seller wallets can streamline payments and enhance loyalty but are complex in execution. For instance, the business may hold cash in those wallets that belongs to a third party —often referred to as third-party money (3PM) — which leads to various licensing, legal, regulatory and commercial considerations. In addition, innovative payout options such as split payments could impact the treasurer’s processing and reconciliation.

-

Elevating in-store experience:

As eCommerce continues to rise in popularity, payment innovation can elevate the in-store customer experience. One example is through differentiated checkout experiences. Imagine the consumer trying on products virtually within stores after which the sales associate completes the transaction on the spot via a mobile device. Through this experience, commerce now meets consumers wherever they’re at across the entire journey.

-

Digital collections:

Employees, small business retailers and large suppliers can reap the benefits of payment innovation as well. One major opportunity is within digital collections. For years, some beverage companies have received cash payment after delivering products to small businesses or bars. With payments innovation, the same brands could now collect digitally from small businesses. Switching from cash to digital payments enhances the small brand’s customer experience and more importantly improves the beverage brands’ working capital.

-

Employee pay-outs:

Large brands that employ gig and seasonal workers can benefit from payment advancements that foster early wage access. Treasurers can leverage real-time payments and prepaid cards to allow these employees to access their earnings on demand, which research indicates is a substantial benefit to these employees and can serve as a way to retain employees.

Managing new flows

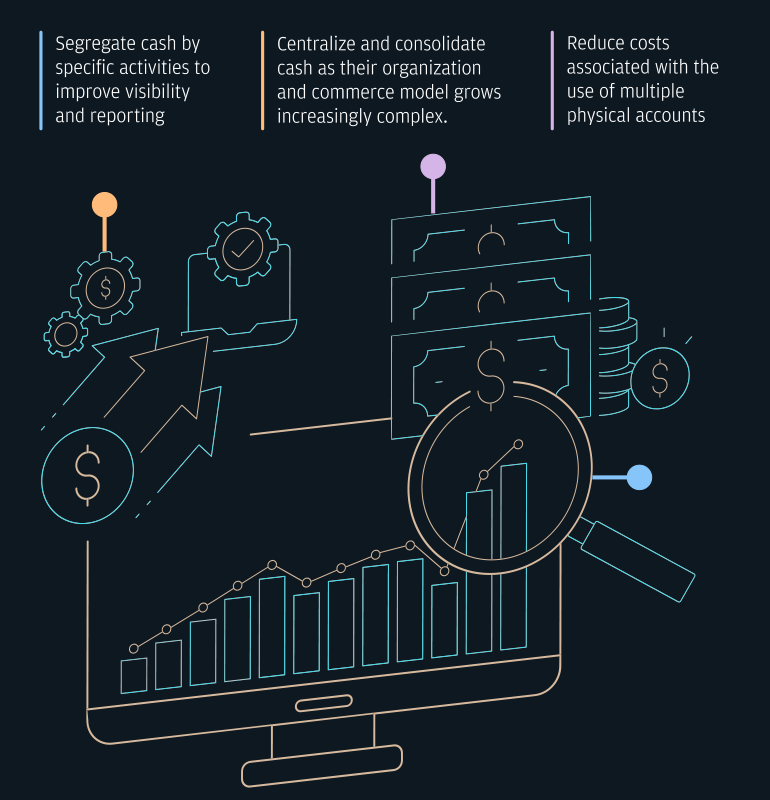

With these new shifts, treasurers should consider updating their systems and processes to stay ahead and manage the new inflows and outflows. One way is through adopting a sub-ledger structure with virtual accounts. Through this structure, treasurers can support audience- or business-specific requirements from a reporting and accounting perspective.

Treasurers can also benefit from sub-ledgers in a few ways:

- Segregate cash by specific activities to improve visibility and reporting.

- Centralize and consolidate cash as their organization and commerce model grows increasingly complex.

- Reduce costs associated with the use of multiple physical accounts.

Treasures will also want to better understand how new commerce and the flow of money impacts their FX exposure. Below are a few questions that they’ll want to consider:

-

Are new commerce models driving regional shifts to supply-chains or capturing new consumer markets?

-

What are the new FX payments from consumers and to sellers?

-

Are any of these new exposures in trapped cash markets?

-

Do any new currency exposures occur in markets with more complex requirements?

-

Is the increased exposure aligned to a larger growth strategy?

In many instances, making larger and more complex enhancements is necessary. For example, multi-party commerce models may subject brands and operators to licensing and certification requirements. Brands may want to offer a financial ecosystem to the sellers on its platform, which can include FX management. Doing this requires companies to decide whether they want to be in the flow of funds (or not). Those who want to avoid this complexity should engage treasury early in the process to ensure their banking and payment partners remain out of the flow of funds.

Evolving supply chains

Most consumer goods and retail supply chains have been under pressure in recent years, and new commerce models are compounding these shifts. The last few years exacerbated the need for reliable supply-chains, triggering long-term strategy shifts that impact treasurers in the following five ways:

-

Nearshoring:

Many consumer good companies are mitigating supply chain delays by shifting manufacturing facilities closer to three key hubs: North America, Europe and East and Southeast Asia. For instance, Latin America is expected to gain $78 billion in exports from short-term nearshoring strategies1. Treasurers can help manage the new FX exposure and cash needs to meet the increased payment obligations in Latin America.

-

China + 1:

Many organizations have been complementing their supply chains beyond China. The primary beneficiaries of the China + 1 strategy are Vietnam, Thailand, Indonesia, Malaysia and other low-cost southeastern Asian markets. Treasurers can help navigate the complex liquidity and capital movement requirements that are often in these markets.

-

ESG-driven shifts:

Supply chains are also levers to advance Environmental, Social and Governance agendas. At the recent UN Climate Change Conferences (COP26 and COP27), consumer goods brands and agriculture companies alike have committed to sustainability such as reducing deforestation from the soy and cattle supply chains or moving to low-carbon materials to reduce emissions. Treasury manages FX and working capital in these situations, and more importantly, they can work with procurement and bank partners to reward suppliers who support their initiatives with improved supplier financing rates.

-

Powering small business suppliers:

Small businesses are critical to consumer goods and retail sector, especially as consumers demand more locally-sourced products. Suppliers can offer their small-to-medium business partners virtual card solutions like single-use accounts. These benefits allow small businesses faster and easier ways to get paid, which can improve their days sales outstanding (DSO) and working capital while reducing paper-based transactions and costs. With small businesses being the lifeblood of communities, empowering these partners – customers, distributors, and suppliers – can also advance the diversity, equity and inclusion agenda.

-

Improving supply chain resiliency and flexibility:

As consumer preferences evolve at an accelerated rate, inventory management should become increasingly agile and flexible. Treasurers can consider inventory financing to help businesses better manage inventory demand influxes at critical periods. Inventory financing programs can help leverage the resources of a bank partner to pay for production (one of an organization’s largest expenses). This can be particularly useful during periods of long delays between paying for inventory and receiving payment from retailers and customers.

Through these innovations, treasurers are prepared to help transform customer experiences. This transformation takes a team: brand managers, customer experience directors, channel leads, procurement partners, and treasury. Every player has a unique role in paving the path toward the future of shopping.

To learn more about how we can support your business, please contact your J.P. Morgan representative.

References

Nearshoring can add annual $78 bln in exports from Latin America and Caribbean. IADB. (n.d.). Retrieved February 28, 2023, from https://www.iadb.org/en/news/nearshoring-can-add-annual-78-bln-exports-latin-america-and-caribbean

Reimagining shopping is more important than ever

Customers expect innovative and convenient shopping experiences, so businesses are innovating around how customers make purchases and engage with brands. Payments is one of these innovations.

Read more about the Future of Shopping

View more Future of Shopping insights

Join us as we explore how specific key industries are affected, how you can future-proof, and what that means for the future.

Deposits held in non-U.S. branches are not FDIC insured. All rights reserved. The statements herein are confidential and proprietary and not intended to be legally binding. Not all products and services are available in all geographical areas. Visit jpmorgan.com/disclosures/payments for further disclosures and disclaimers related to this content.