Elevate the payments experience you deliver...

The future of commerce is the future of payments. Simply stated, few things have a deeper impact on every aspect of your business.

And whether that business is in consumer goods, retail, apparel and luxury, restaurants and food services, or agriculture, we can provide customized, end-to-end solutions that make customers' experiences faster, easier and more secure across channels.

on your customers and your business?

Stefan Jensen

Vice President, Treasurer, Sephora

Josh Janos

VP, Marketplace, Macy’s, Inc.

Nancy Romain

Treasury Team Leader at Domino’s Pizza

with these 5 major trends

Accept contactless payments with Tap to Pay on iPhone

Now you can accept in-person, contactless payments right on your iPhone—no extra card readers or hardware needed4.

Read the latest

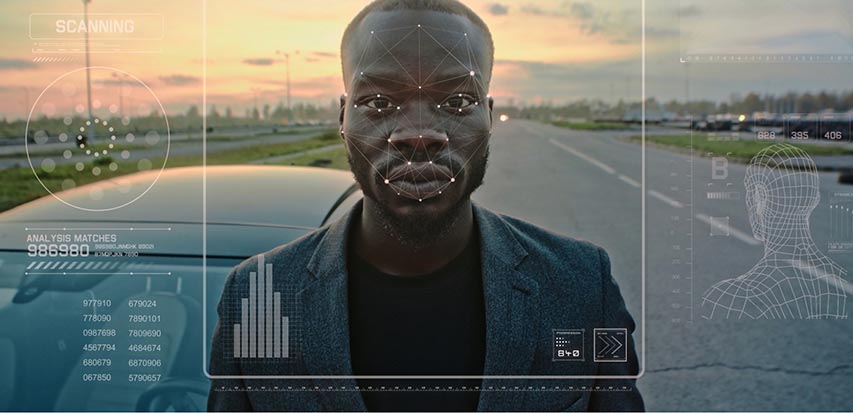

Discover biometrics, the new face of payments

See how biometrics payments can fuel the speed and efficiency of the checkout experience.

Future capabilities of biometrics are under development; features and timelines are subject to change at the bank’s sole discretion.

See what’s new

3 billion users

Simplify commerce with omnichannel payments

Build a top-notch, end-to-end payments journey across shopping, purchasing, delivery and returns.

Start your journey

See tomorrow’s opportunities today with biometrics personalized commerce

Look into the future of payments, as personalized commerce unlocks new insights, experiences and business opportunities.

Learn more

Tap into the social commerce explosion

Explore the rapidly growing branch of e-commerce that uses social networks and digital media to power transactions.

LEARN MORE

Look to our full offering of solutions to help grow your revenue.

Commerce solutions

Transform B2C and B2B experiences with the next generation suite of commerce solutions by J.P. Morgan Payments.

Working capital

With rising interest rates, supply chain disruptions and increased inventory requirements, doing business today is challenging.

Treasured

Treasurers are changing the world - and given digital transformation, collaborating across departments to inform effective outcomes is on the rise.

Analytics and insights solutions

Our data solutions help you harness all your data into actionable insights while helping you navigate rapidly-changing economic environments with confidence.

Contact Sales

Get in touch with an experienced J.P. Morgan representative to learn more.

For customer service inquiries, existing Merchant Services clients may contact 1-888-886-8869 or email merchant.priority.support@chase.com.

2 McKinsey 2020

3 PBOC publication, U.S. Bureau of Economic Analysis publication, European Commission reports, Trading Economics Estimates; NielsonIQ - 2023 Retail Landscape

4 Tap to Pay on iPhone requires the latest version of iOS. Update to the latest version by going to Settings › General › Software Update. Tap Download and Install. Some contactless cards may not be accepted. The Contactless Symbol is a trademark owned by and used with permission of EMVCo, LLC. Tap to Pay on iPhone is not available in all markets. View Tap to Pay countries and regions. For more details, see https://developer.apple.com/tap-to-pay/.

Apple and the Apple logo are trademarks of Apple Inc., registered in the U.S. and other countries. App Store is a service mark of Apple Inc.

5 Goode Intelligence