The venture capital ecosystem had a turbulent time in 2023. Deal-making activity slowed across the board, adding pressure to founders to be more thoughtful in funding their startups’ growth. With differences in negotiating power, investor access, and competition for dollars—coupled with a dynamic seed fundraising environment—raising equity capital is never easy.

Seed fundraising activity slows

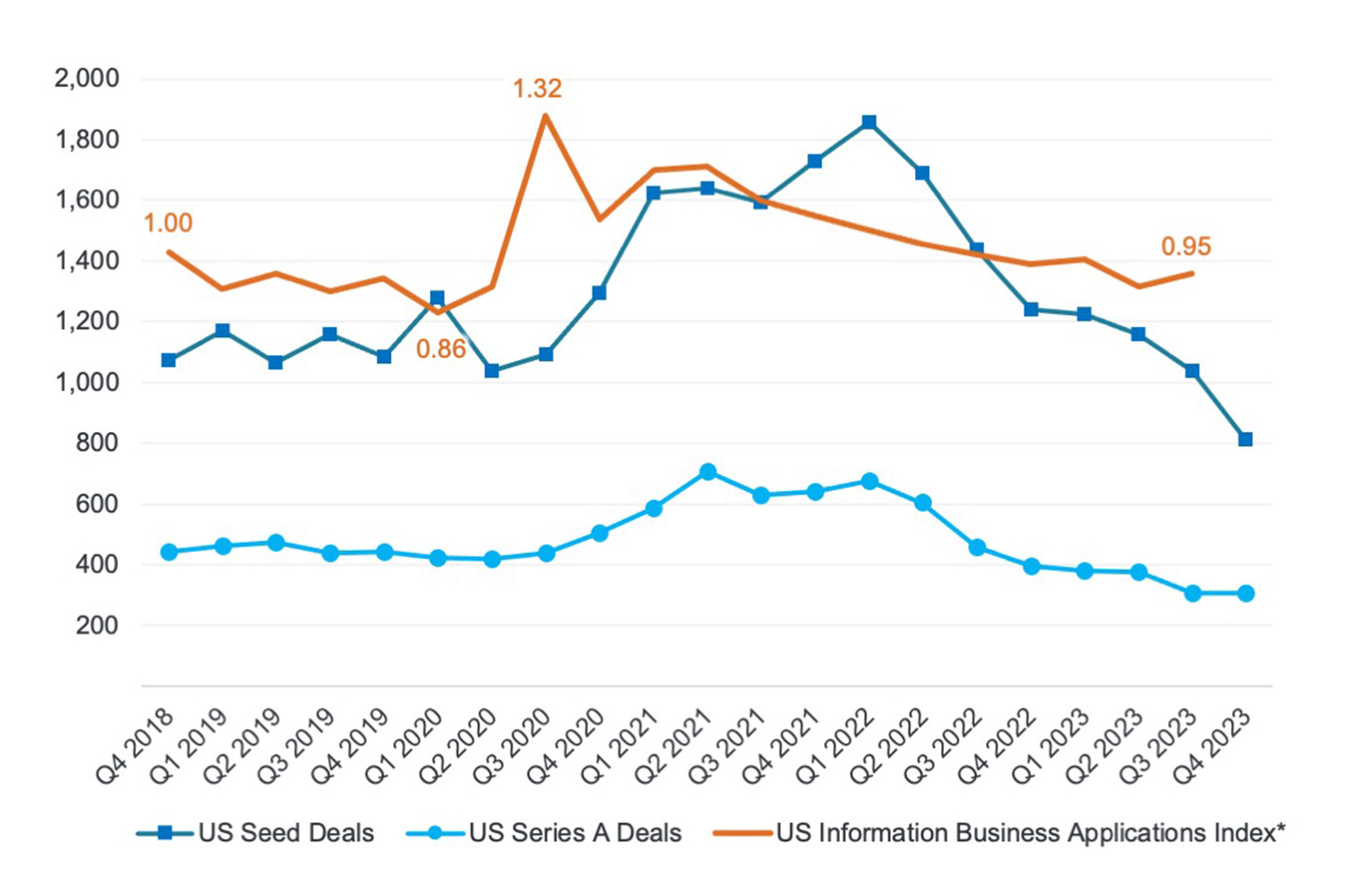

Unlike later-stage investment activity, early-stage investment has historically been less sensitive to the economic environment, public market performance and the business cycle. However, as macroeconomic factors dragged down total U.S. venture investment from its 2021-22 peak, the number of seed deals declined 56% between Q1 2022 and Q4 2023, even though company formations remained stable.

U.S. early-stage deal trends and information company formation (indexed to Q4 2018)

Seed fundraising activity slows

The graph shows how US seed deals, US Series A deals, and the US Information Business Applications Index have trended from late 2018 to Q4 2023. The US Information Business Applications index and the number of Series A deals have stayed relatively steady in the last few years, while the number of US seed deals have trended downward starting from its peak in Q1 2022. Specifically, the number of seed deals declined 56% between Q1 2022 and Q4 2023, reaching its lowest point in the last five years.

*High propensity business applications. Business applications that have a high propensity of turning into businesses with payroll.

Source: PitchBook and U.S. Census Bureau.

Interestingly, while activity declined, the founders who were able to close a seed deal (between Q3 and Q4 2023) did so at a historically high valuation, raising more on average than any other period before. This is especially surprising given “negotiating power,” determined by PitchBook’s VC Dealmaking Indicator, has swung back in the investor’s favor. Which begs the question: Has the nature of a seed round changed indefinitely?

The changing face of seed

By comparing seed fundraising metrics across notable periods—pre-pandemic (Q4 2019), peak seed (Q1 2022) and today (Q4 2023)—we can get a sense of the underlying drivers.

| Cohort Stats | Pre-Pandemic Q4 2019 | Peak-Seed Q1 2022 | Today Q4 2023 |

|---|---|---|---|

| Number of US Seed Deals | 1,085 | 1,859 | 811 |

| Median Deal Size | $1.9M | $2.3M | $3.0M |

| Deal Size Range (25th - 75th) | $0.8M - $3.3M | $1.0M - $4.8M | $1.3M - $5.1M |

| Median Pre-Money Valuation | $7.0M | $10.0M | $12.0M |

| Pre-Money Valuation Range (25th - 75th) | $4.0M - $10.0M | $6.0M - $18.3M | $7.4M - $20.0M |

| Median Valuation Step-Up | 1.6x | 2.1x | 1.6x |

| Dealmaking Indicator (Neutral = 50)* | 41 | 6 | 85 |

*Per PitchBook’s VC Dealmaking Indicator.

Source: PitchBook.

The pre-pandemic period was at a point when venture capital was establishing itself as a prominent asset class. Capital inflows were growing, and the ecosystem was well-balanced. Negotiating power was fairly even between founders and investors, and deal sizes and valuations both stayed within a tight range. By contrast, the period of peak seed had almost double the amount of deals. The high rate of deal activity plus competition from new entrants for the “best” deals left investors scurrying, therefore, limiting their ability to negotiate pricing and conduct thorough due diligence. The result was favorable for many founders raising money as they leveraged their negotiating power to raise more capital at higher valuations. Unsurprisingly, both deal size and valuation ranges grew, with a median step-up in valuation of 2.1x.

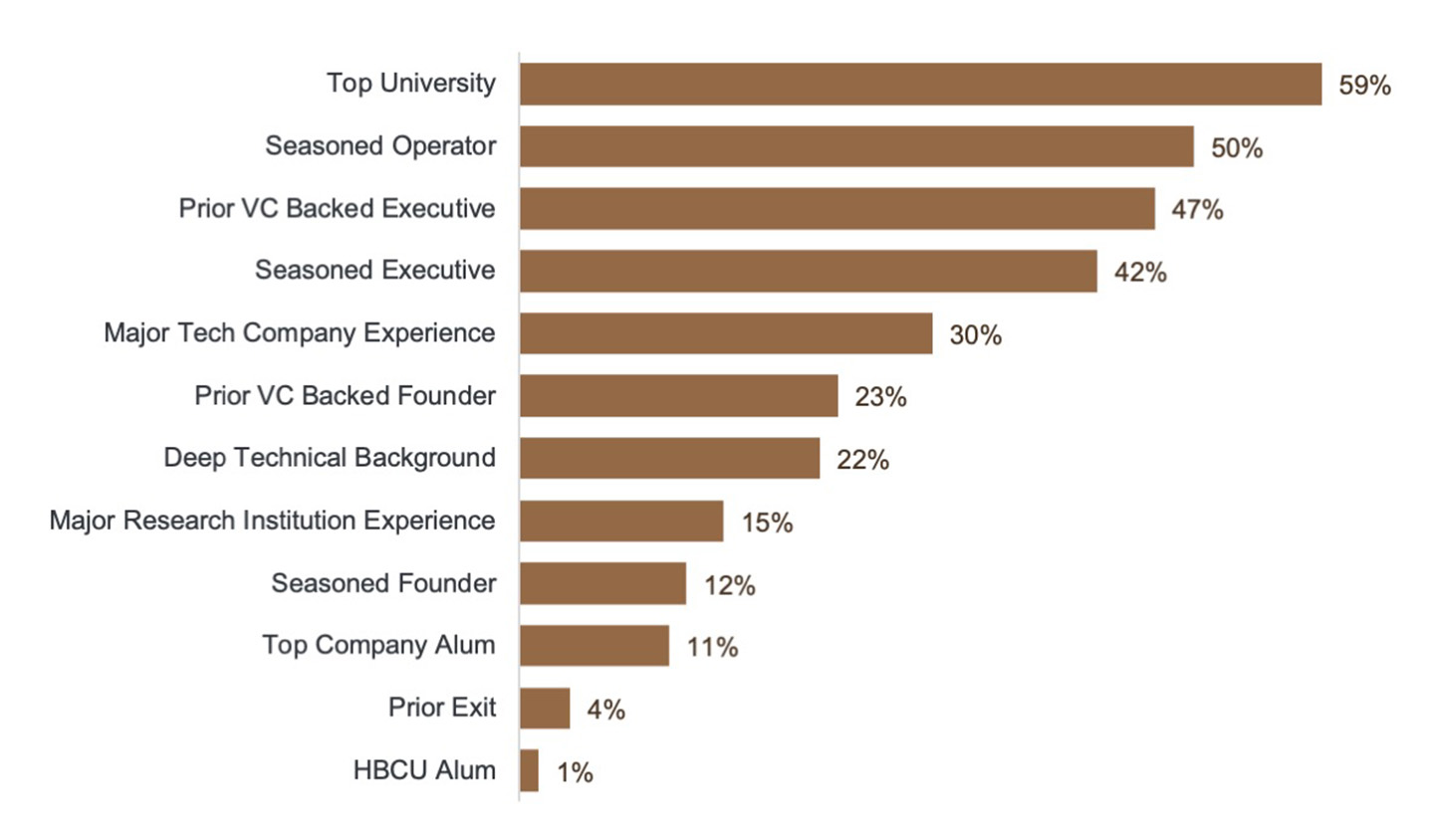

Today, the pricing of seed deals has remained elevated, but the number of deals closing has fallen back to pre-pandemic levels. Investors have slowed their activity and are more selective when making investments. As such, negotiating power has swung drastically from founder-friendly in Q1 2022 to investor-friendly in Q4 2023. The most recent seed cohort is surprisingly concentrated in New York (13% of deals) followed by San Francisco (8% of deals), although California as a whole dominates (26% of deals). From a sector standpoint, unsurprisingly, software-as-a-service (16%) and artificial intelligence (15%) dominate as percentage of total deals. The background of founders is always important, especially for seed-stage startups. Using data from Harmonic, we see that founders who were able to raise a seed round in Q3 2023 likely attended a top university and had prior experience in the industry.

Background of startup founders that raised a seed round in Q3 2023

Background of Startup Founders that raised a Seed round in Q3 2023 Seed

The bar graph lists background characteristics of startup founders that raised a seed round in Q3 2023, ranking them from most to least common. The top two most common qualities of founders in this cohort included having graduated from a top university (59%) and prior experience in the industry (50%), which illustrates how investors see these characteristics as important attributes of founders.

Bridging the gap

Founders should take note of the more cautious approach investors are taking influenced by the current macroeconomic backdrop. Valuations at the early stage have been on an upward trend, but the range has become wider. Founders should be realistic on how their company stacks up against its peers from an investment perspective. To help support a target valuation, founders should have a plan that includes a product roadmap, financial model and the level of hiring required to get to break-even. Founders also need to research alternatives. Maybe the company isn’t ready for institutional investment and the demands it brings. The Small Business Innovation Research (SBIR) and Small Business Technology Transfer (STTR) offer government-funded programs to support research and development via grants and contracts. The National Science Foundation has many opportunities for entrepreneurs, including funding from the “America’s Seed Fund” program.

Coming to terms

Speaking to early-stage investors about the most important attribute they look for in the current environment, the founder’s (and teams) profile is the major focus. A strong leadership team with prior startup experience and a goal of pursuing a large market opportunity with a clear need is ideal. In addition, it is important to see founders who are resilient (amid a turbulent market) and stubbornly motivated to succeed. Other important considerations are the current and future state of competition, how much the technology has been de-risked and how differentiated the startup’s offering is in market. The main factors that will work against founders raising capital today are lack of startup and industry experience, developing an undifferentiated solution, and if the technology/market is viewed as too early.

Closing the round

To increase their probability of success, founders should:

- Pack their calendars to increase their chances of finding the right investor.

- Clearly articulate the problem they’re solving, the team’s relevant experience, the market opportunity, and why their offerings are uniquely positioned to succeed.

- Consistently read the room during pitches and adapt to the investor team in front of them.

- Be curious and open to questions and feedback. Ask clarifying questions during negotiations.

- Be persistent.

- Be timely with responses to diligence questions.

- Avoid getting attached to a valuation. Valuations don’t reflect your worth, so don’t take it personally.

- Maintain good relationships with existing investors and always look to build relationships with new ones.

Let’s build your future, together

Our Innovation Economy Banking team has the expertise, network and solutions to guide founders, investors and startups through every stage of growth. Learn more about how we can help your company achieve its goals at jpmorgan.com/innovationeconomy.

© 2024 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A. Member FDIC. Visit jpmorgan.com/cb-disclaimer for disclosures and disclaimers related to this content.