Despite a challenging few years, healthcare leaders are relatively optimistic about the economy and their financial performance for the year ahead.

Our 2023 Business Leaders Outlook survey gathered feedback from leaders of midsize healthcare organizations — those with annual revenues between $20 million and $500 million. The results show that just under half (48%) of healthcare executives have an optimistic outlook about the national economy. That’s a dramatically more upbeat position than the findings across all U.S. industries, where only 22% are optimistic about the national economy.

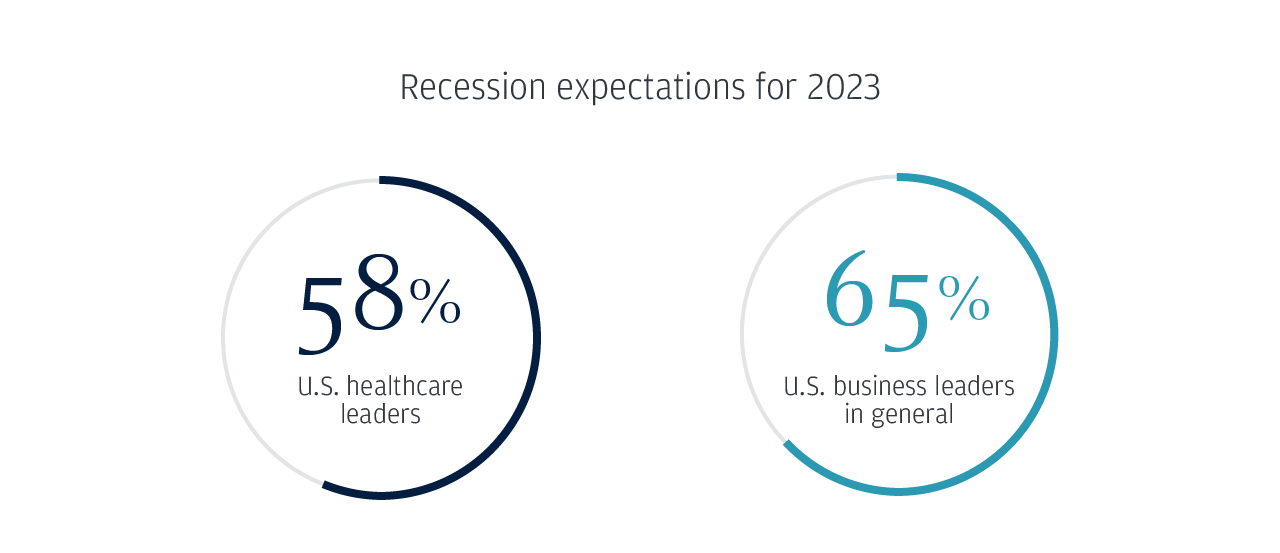

A commanding 91% of respondents expect to maintain or increase their revenue and sales this year, and 87% expect to maintain or increase profits—even as 58% expect a recession in 2023.

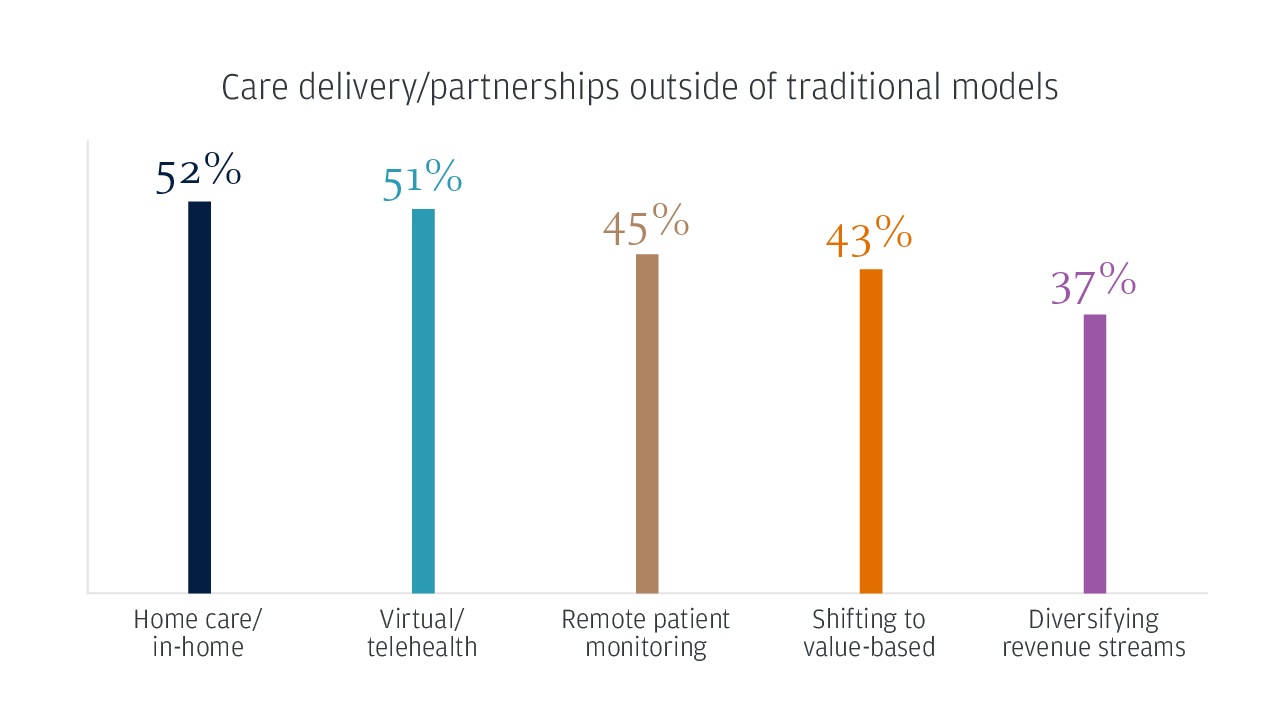

The survey also reflects the consumer-driven transformation happening in healthcare. Nine in 10 industry leaders identified at least one way they plan to evolve beyond their traditional models, with a majority considering in-home care (52%) and virtual care (51%).

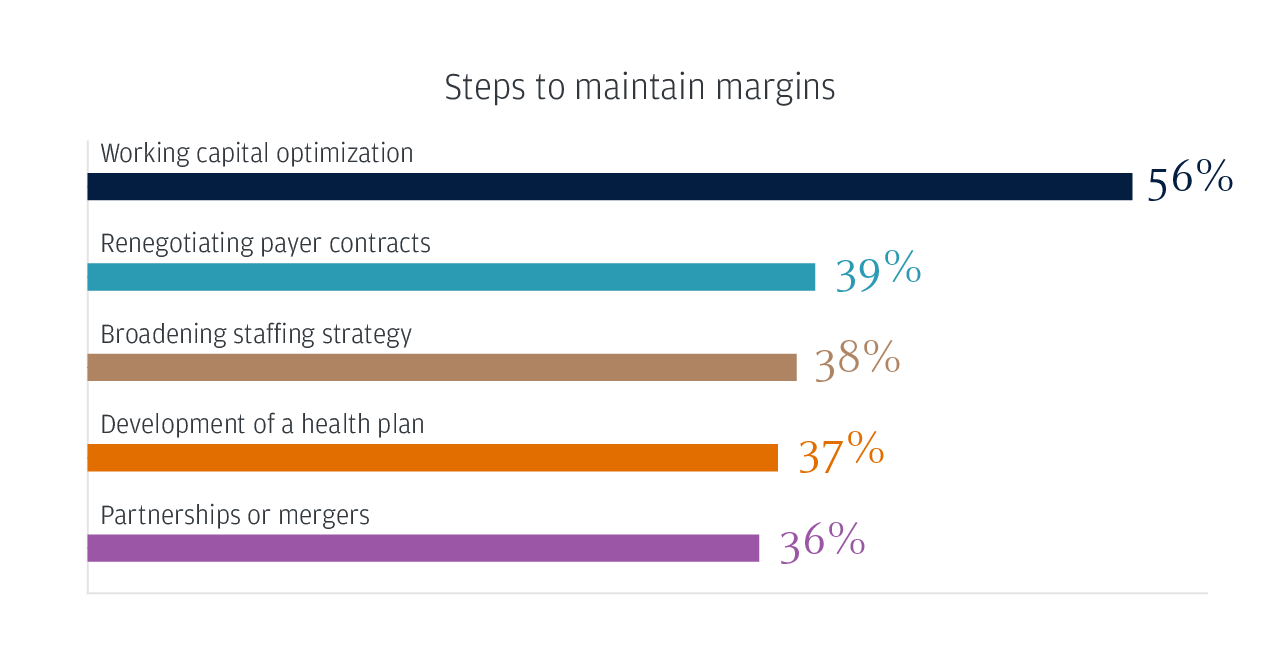

On the labor front, 76% of respondents said they plan to maintain or add to their headcount. More than half (56%) of businesses are taking steps to optimize their working capital, and 38% are broadening their staffing strategy to maintain margins.

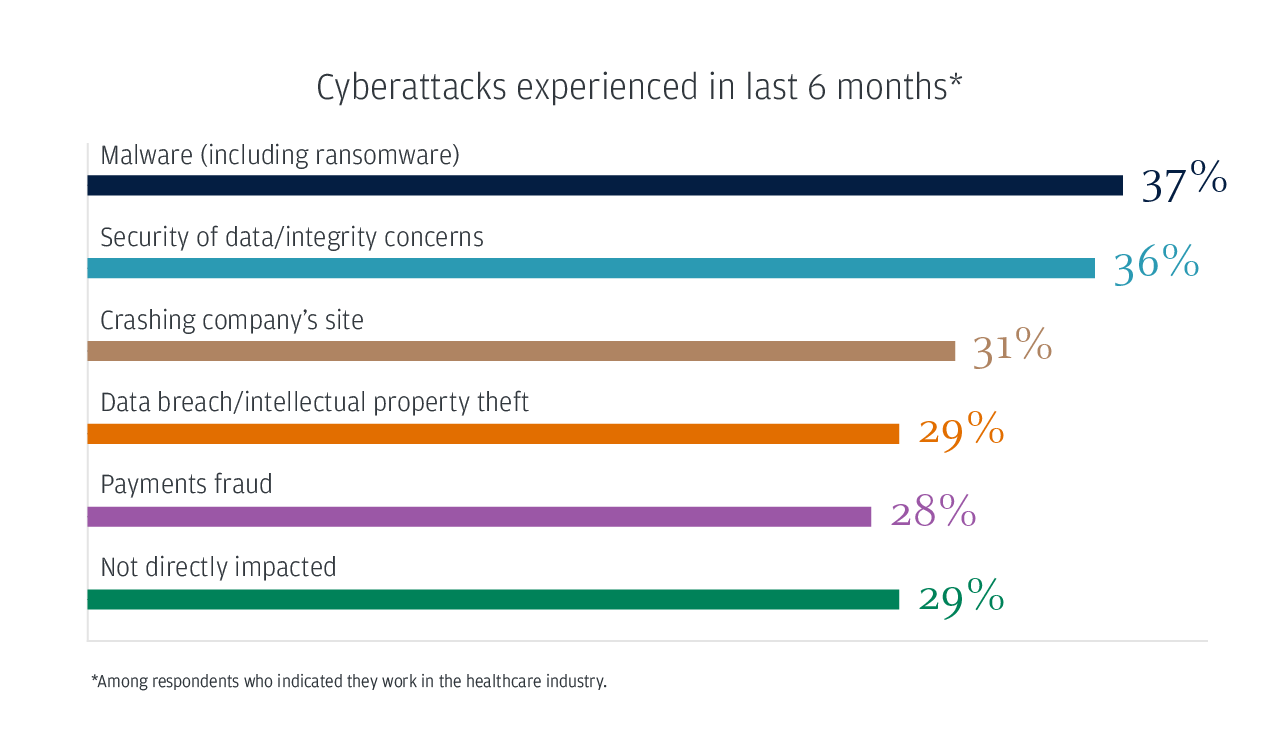

Cybersecurity and fraud remain a widespread threat to the healthcare industry. More than two-thirds (71%) of those surveyed indicated they have been directly impacted by cyberattacks in the last six months.

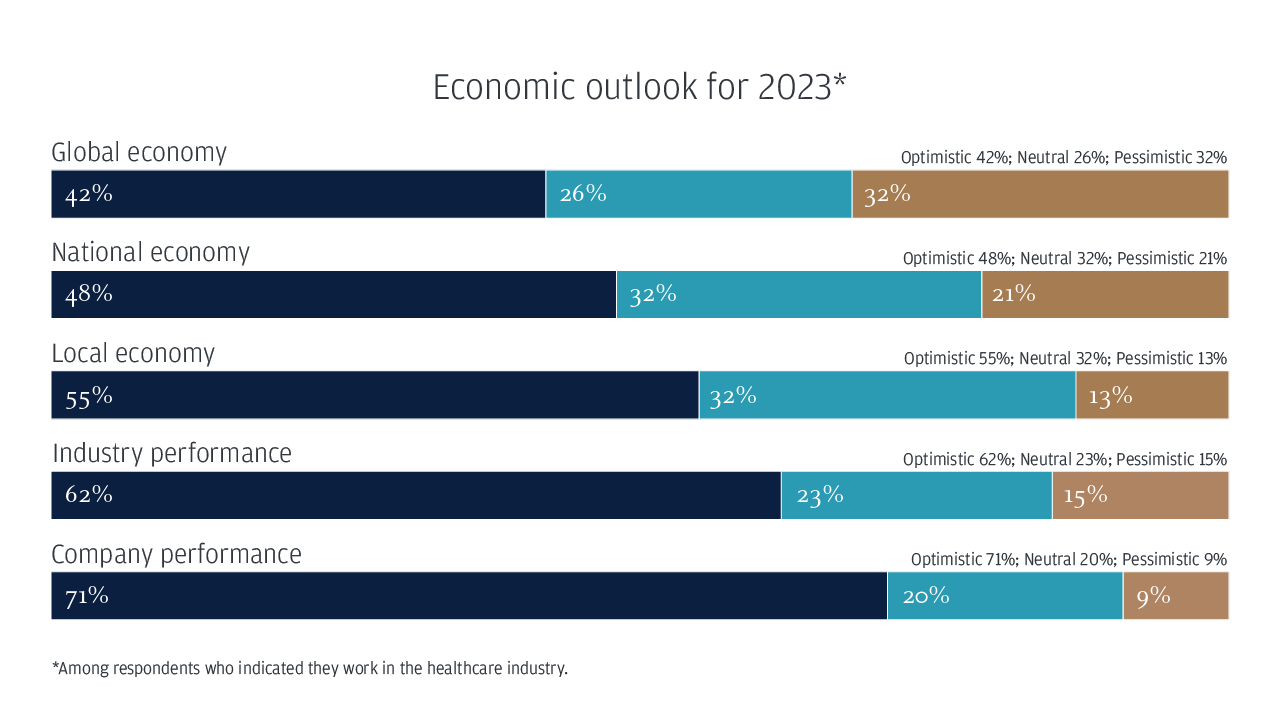

Economic outlook for 2023*

Global economy: Optimistic 42%; Neutral 26%; Pessimistic 32%

National economy: Optimistic 48%; Neutral 32%; Pessimistic 21%

Local economy: Optimistic 55%; Neutral 32%; Pessimistic 13%

Industry performance: Optimistic 62%; Neutral 23%; Pessimistic 15%

Company performance: Optimistic 71%; Neutral 20%; Pessimistic 9%

*Among respondents who indicated they work in the healthcare industry.

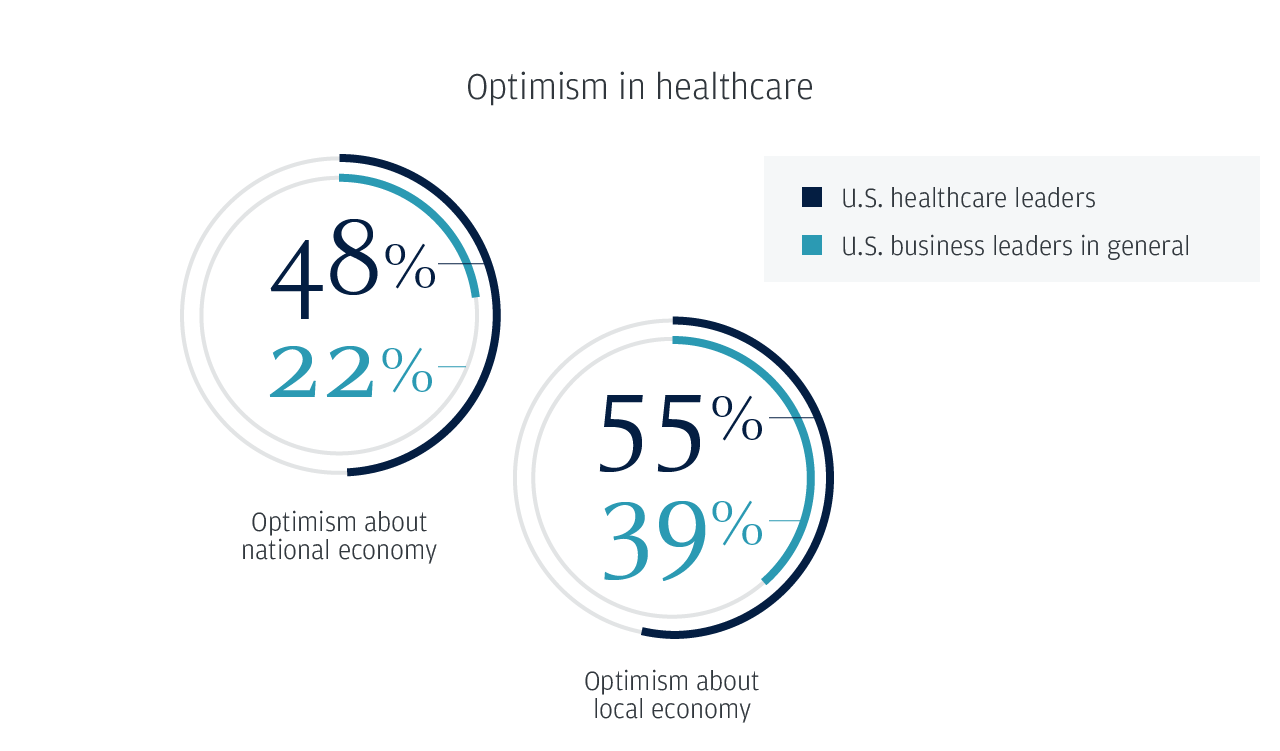

More positive than others

Healthcare leaders are significantly more optimistic about the national and local economy than U.S. survey respondents across all industries.

Optimism in healthcare

Optimism about national economy

U.S. healthcare leaders: 48%

U.S. business leaders in general: 22%

Optimism about local economy

U.S. healthcare leaders: 55%

U.S. business leaders in general: 39%

Recession expectations for 2023

U.S. healthcare leaders: 58%

U.S. business leaders in general: 65%

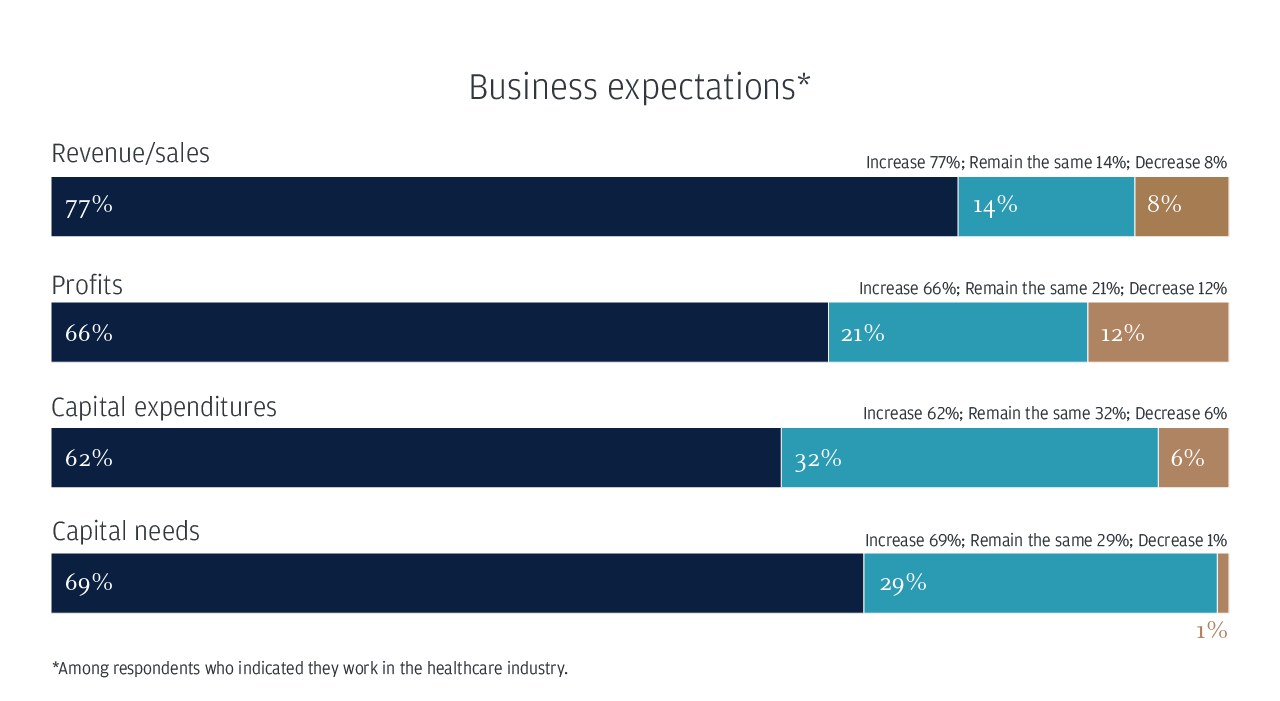

Bullish on their own businesses

More than nine in 10 healthcare executives (91%) expect their revenues to hold steady or increase in 2023. An even greater percentage (94%) expect their capital expenditures to remain the same or increase.

Business expectations*

Revenue/sales: Increase 77%; Remain the same 14%; Decrease 8%

Profits: Increase 66%; Remain the same 21%; Decrease 12%

Capital expenditures: Increase 62%; Remain the same 32%; Decrease 6%

Capital needs: Increase 69%; Remain the same 29%; Decrease 1%

*Among respondents who indicated they work in the healthcare industry.

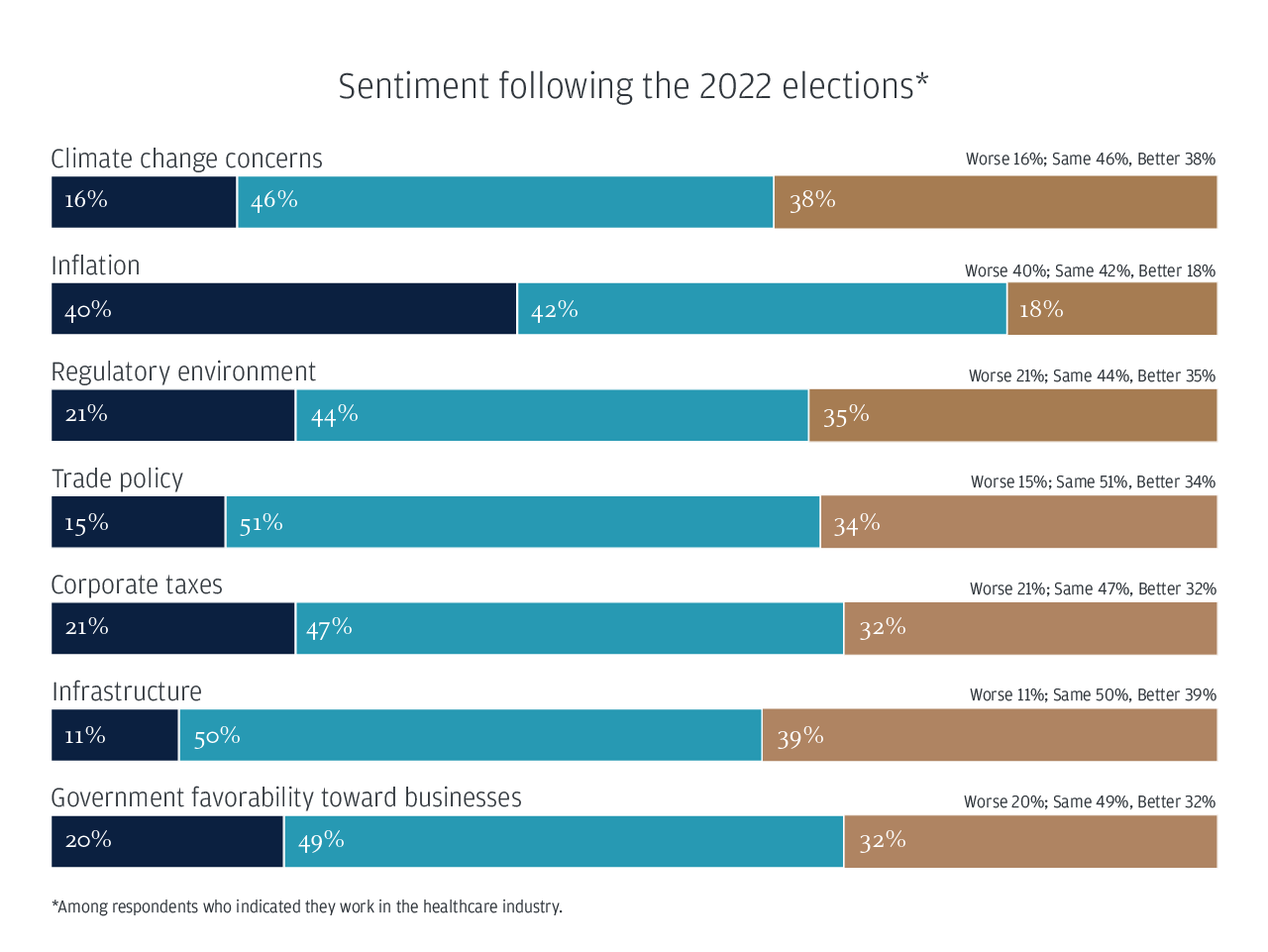

Election effects

Healthcare leaders generally don’t expect many changes due to recent elections.

Sentiment following the 2022 elections*

Climate change concerns: Worse 16%; Same 46%; Better 38%

Inflation: Worse 40%; Same 42%; Better 18%

Regulatory environment: Worse 21%; Same 44%; Better 35%

Trade policy: Worse 15%; Same 51%; Better 34%

Corporate taxes: Worse 21%; Same 47%; Better 32%

Infrastructure: Worse 11%; Same 50%; Better 39%

Government favorability toward businesses: Worse 20%; Same 49%; Better 32%

*Among respondents who indicated they work in the healthcare industry.

Business challenges

Healthcare organizations face a variety of challenges today. Among them: inflation, snarled supply chains and a shortage of available workers.

Top ways companies are adapting to inflation*

Raising prices: 53%

Making changes to purchasing: 48%

Automating more processes: 46%

Changing pricing model: 36%

Prioritizing most profitable products: 32%

Strategic stockpiling: 27%

*Among respondents who work in the healthcare industry and indicated they are experiencing inflation.

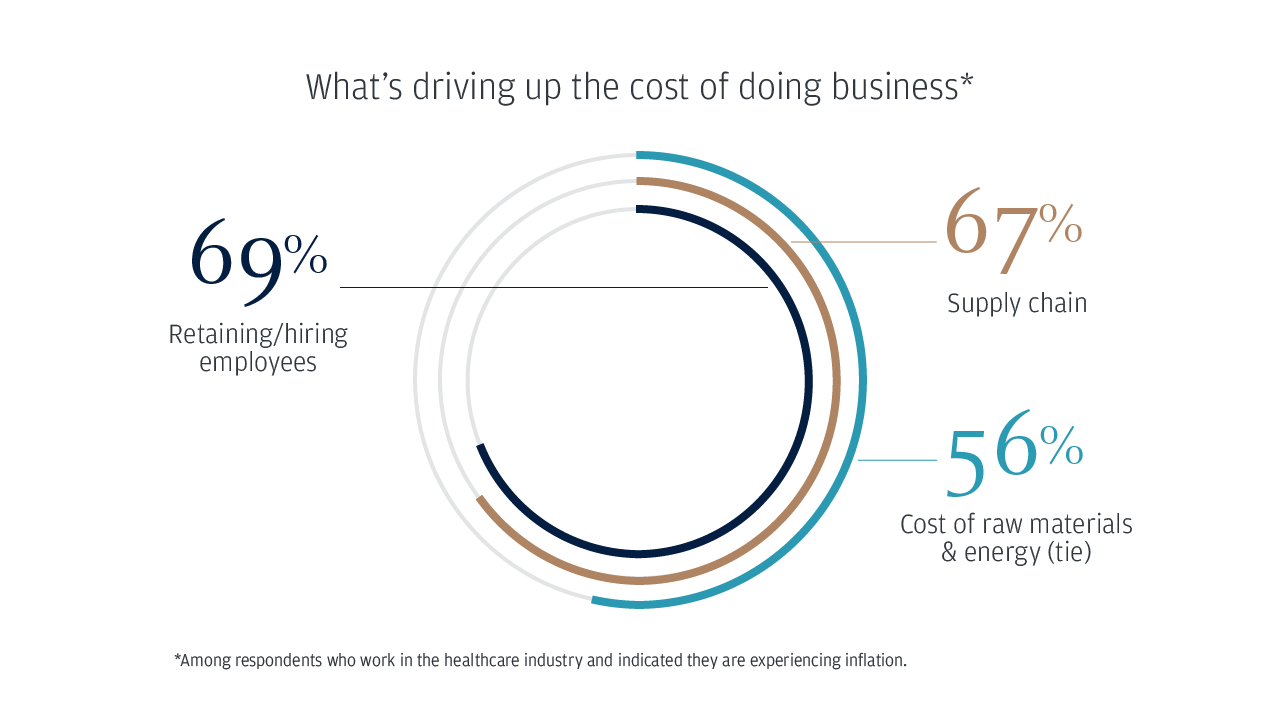

What’s driving up the cost of doing business*

Retaining/hiring employees: 69%

Supply chain: 67%

Cost of raw materials & energy (tie): 56%

*Among respondents who work in the healthcare industry and indicated they are experiencing inflation.

Steps to maintain margins

Working capital optimization: 56%

Renegotiating payer contracts: 39%

Broadening staffing strategy: 38%

Development of a health plan: 37%

Partnerships or mergers: 36%

Top responses to the labor shortage*

Increase wages and/or benefits: 57%

Provide flexible work location: 57%

Offer flexible hours: 56%

Offer upskilling/training: 49%

Invest in automation: 47%

*Among respondents in the healthcare industry who indicated they are planning to increase staff or maintain their current headcount.

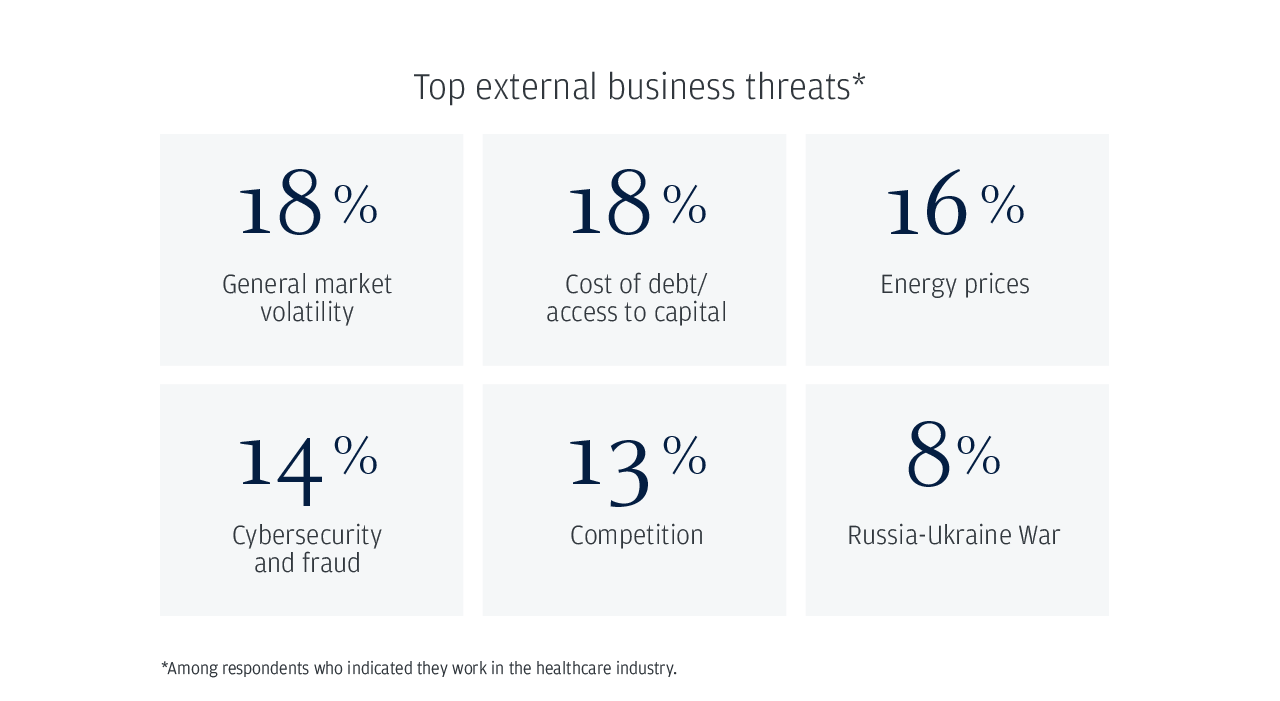

Top external business threats*

General market volatility: 18%

Cost of debt/access to capital: 18%

Energy prices: 16%

Cybersecurity and fraud: 14%

Competition: 13%

Russia-Ukraine War: 8%

*Among respondents who indicated they work in the healthcare industry.

Cyberattacks experienced in last 6 months*

Malware (including ransomware): 37%

Security of data/integrity concerns: 36%

Crashing company’s site: 31%

Data breach/intellectual property theft: 29%

Payments fraud: 28%

Not directly impacted: 29%

*Among respondents who indicated they work in the healthcare industry.

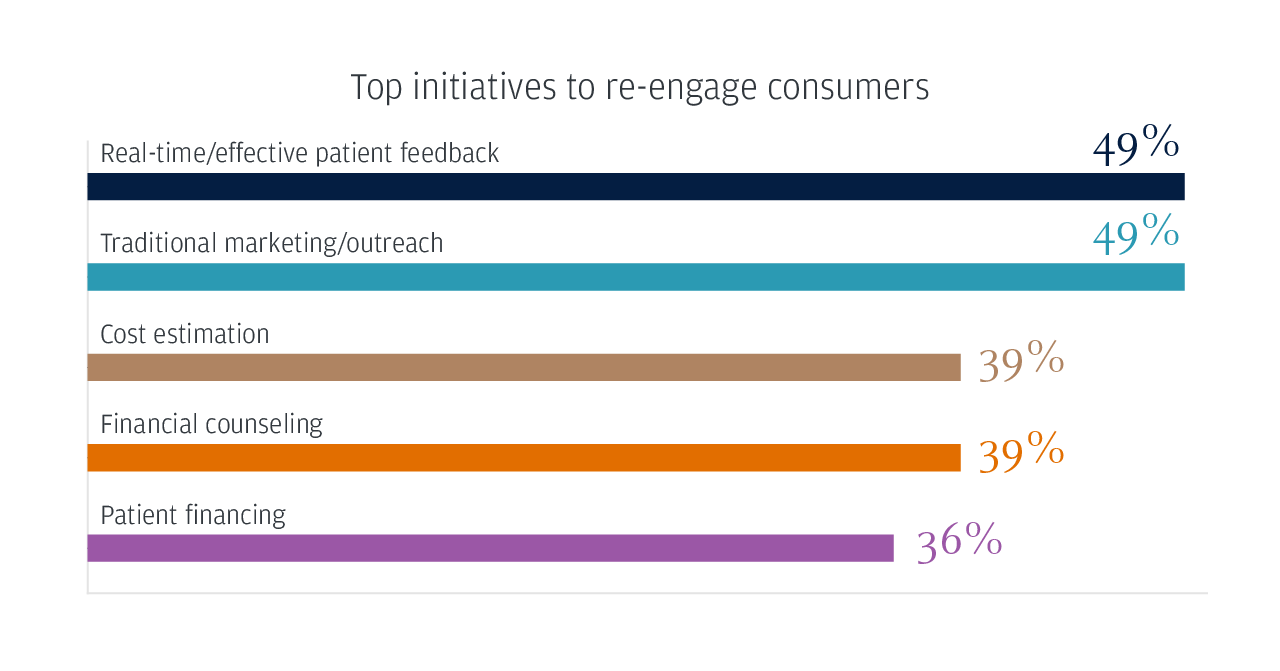

Meeting patient needs

Healthcare leaders are finding innovative ways to deliver alternative methods of care and re-engage consumers in a post-pandemic environment.

Care delivery/partnerships outside of traditional models

Home care/in-home: 52%

Virtual/telehealth: 51%

Remote patient monitoring: 45%

Shifting to value-based: 43%

Diversifying revenue streams: 37%

Top initiatives to re-engage consumers

Real-time/effective patient feedback: 49%

Traditional marketing/outreach: 49%

Cost estimation: 39%

Financial counseling: 39%

Patient financing: 36%

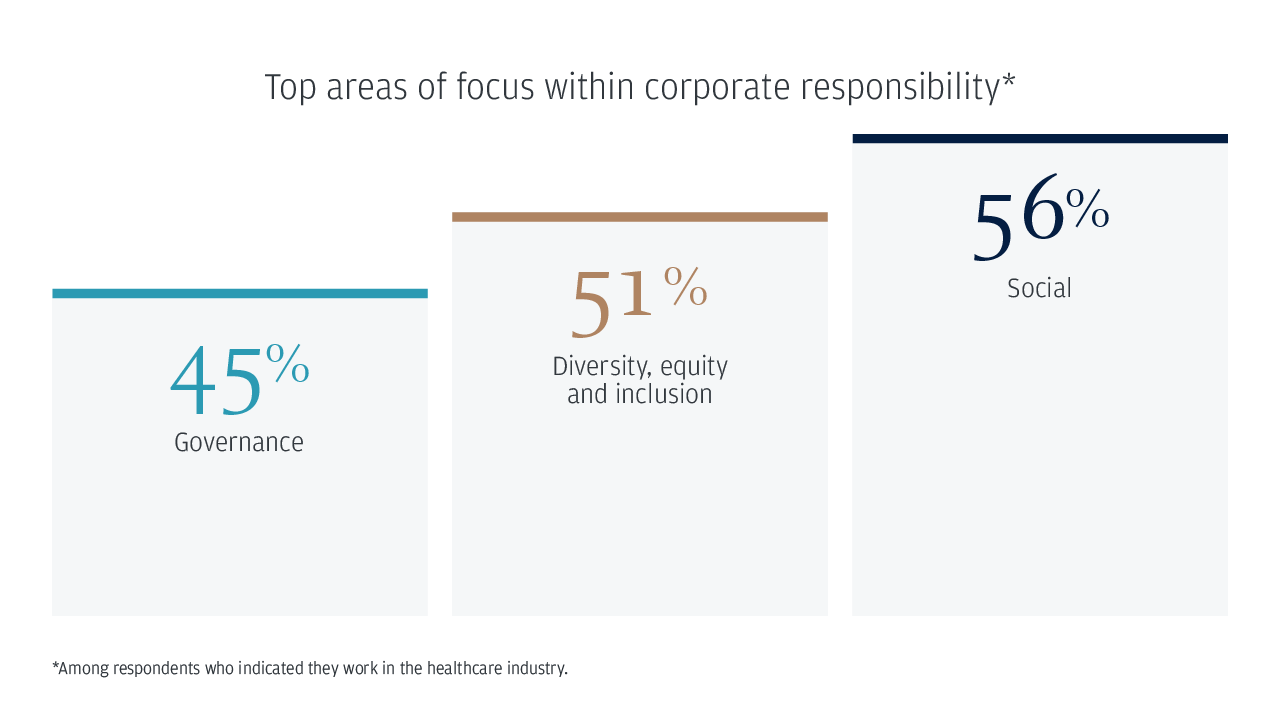

Social responsibility

Top areas of focus within corporate responsibility*

Governance: 45%

Diversity, equity and inclusion: 51%

Social: 56%

*Among respondents who indicated they work in the healthcare industry.

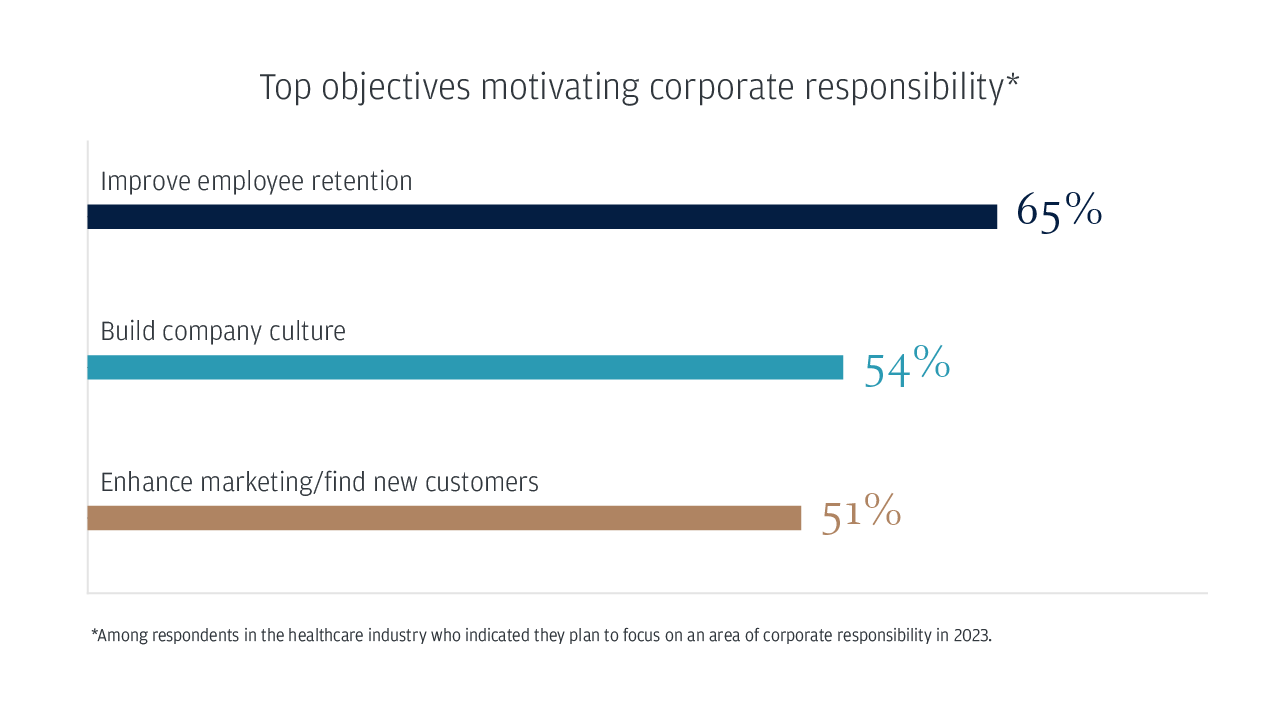

Top objectives motivating corporate responsibility*

Improve employee retention: 65%

Build company culture: 54%

Enhance marketing/find new customers: 51%

*Among respondents in the healthcare industry who indicated they plan to focus on an area of corporate responsibility in 2023.

Business transitions and growth plans

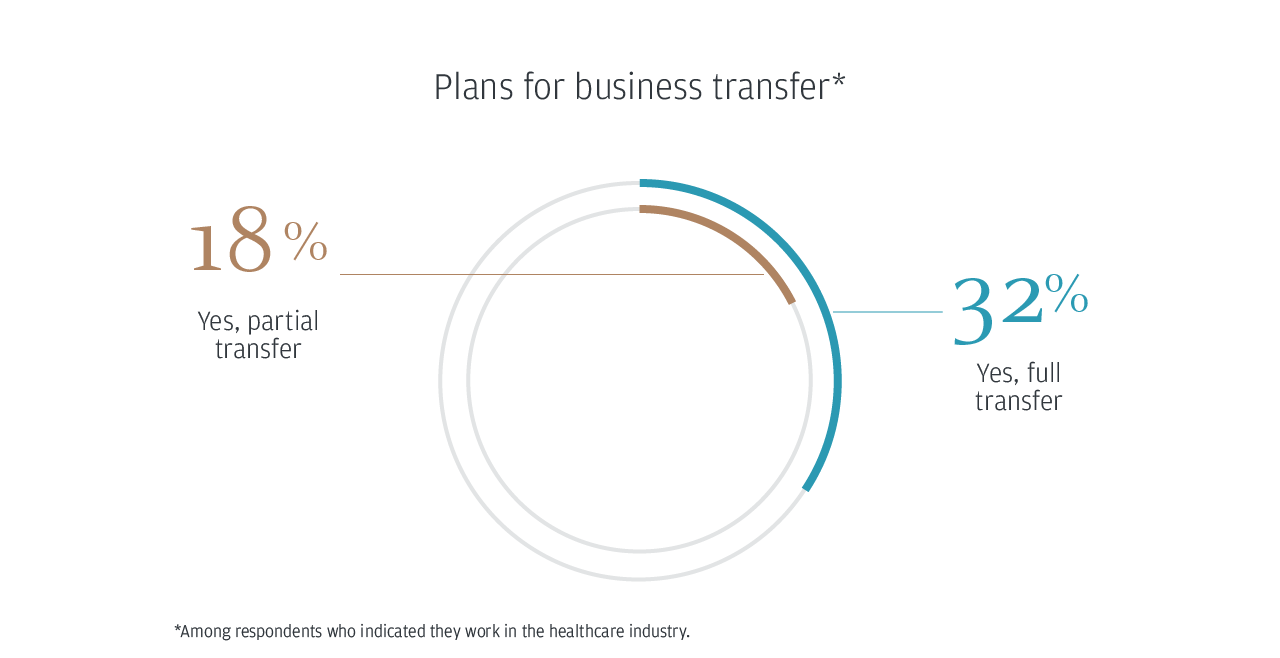

Plans for business transfer*

Yes, full transfer: 32%

Yes, partial transfer: 18%

*Among respondents who indicated they work in the healthcare industry.

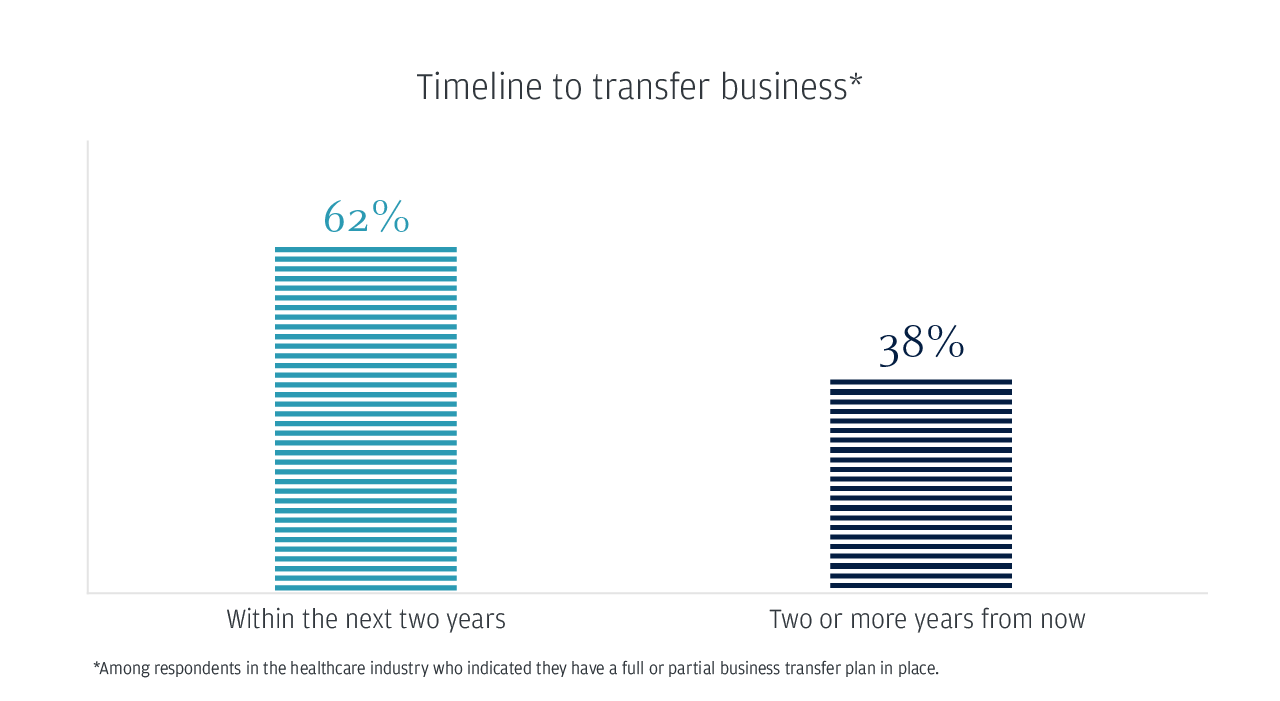

Timeline to transfer business*

Within the next two years: 62%

Two or more years from now: 38%

*Among respondents in the healthcare industry who indicated they have a full or partial business transfer plan in place.

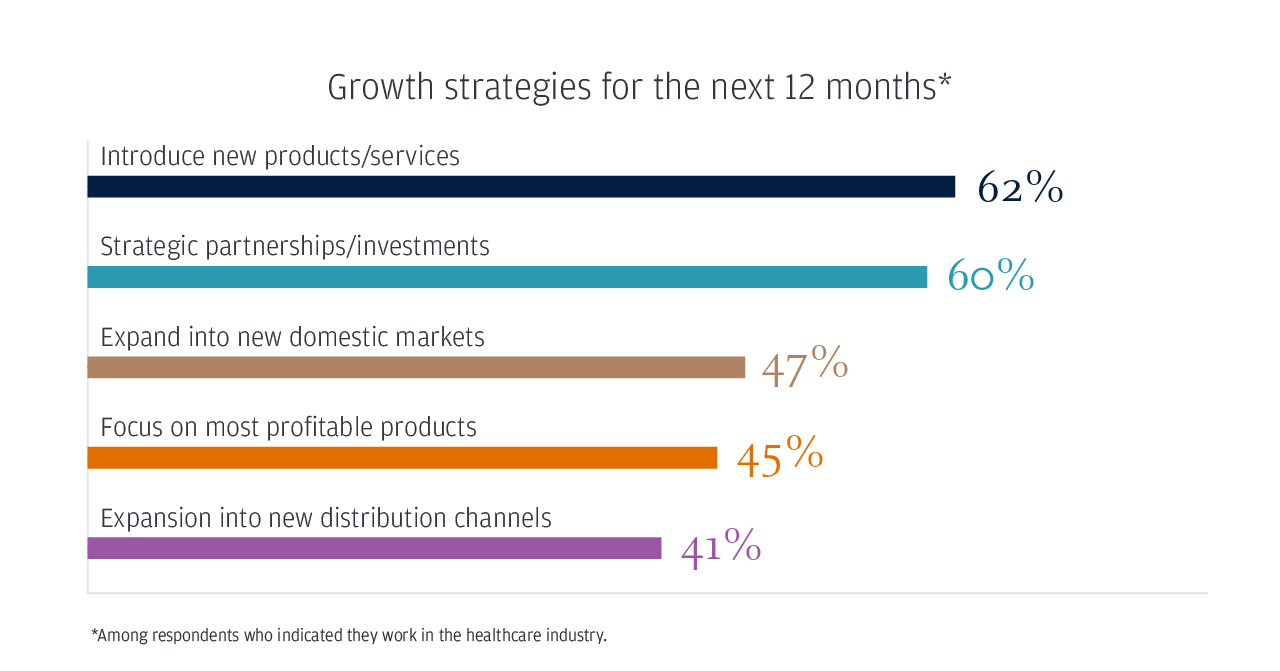

Growth strategies for the next 12 months*

Introduce new products/services: 62%

Strategic partnerships/investments: 60%

Expand into new domestic markets: 47%

Focus on most profitable products: 45%

Expansion into new distribution channels: 41%

*Among respondents who indicated they work in the healthcare industry.

About the survey

Started in 2011, the annual and midyear Business Leaders Outlook survey series provides snapshots of the challenges and opportunities facing executives of midsize companies in the United States.

This year, 791 respondents completed the online survey between Nov. 29 to Dec. 13, 2022. Additionally, 405 respondents with general annual revenue between $20 million and $500 million were recruited via online survey panels. These additional respondents were recruited to achieve readable base sizes for the healthcare industry. Results are within statistical parameters for validity; the error rate is plus or minus 8.2% at the 95% confidence interval.

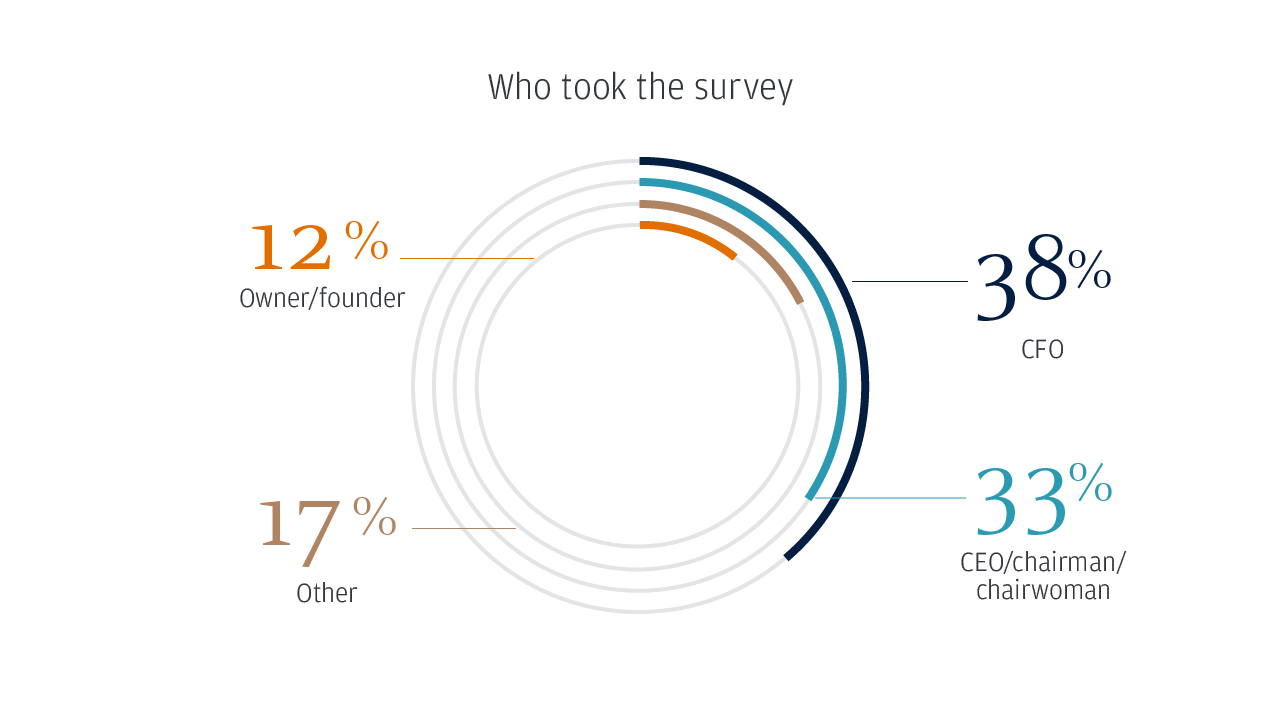

Who took the survey

CFO: 38%

CEO/chairman/chairwoman: 33%

Other: 17%

Owner/founder: 12%

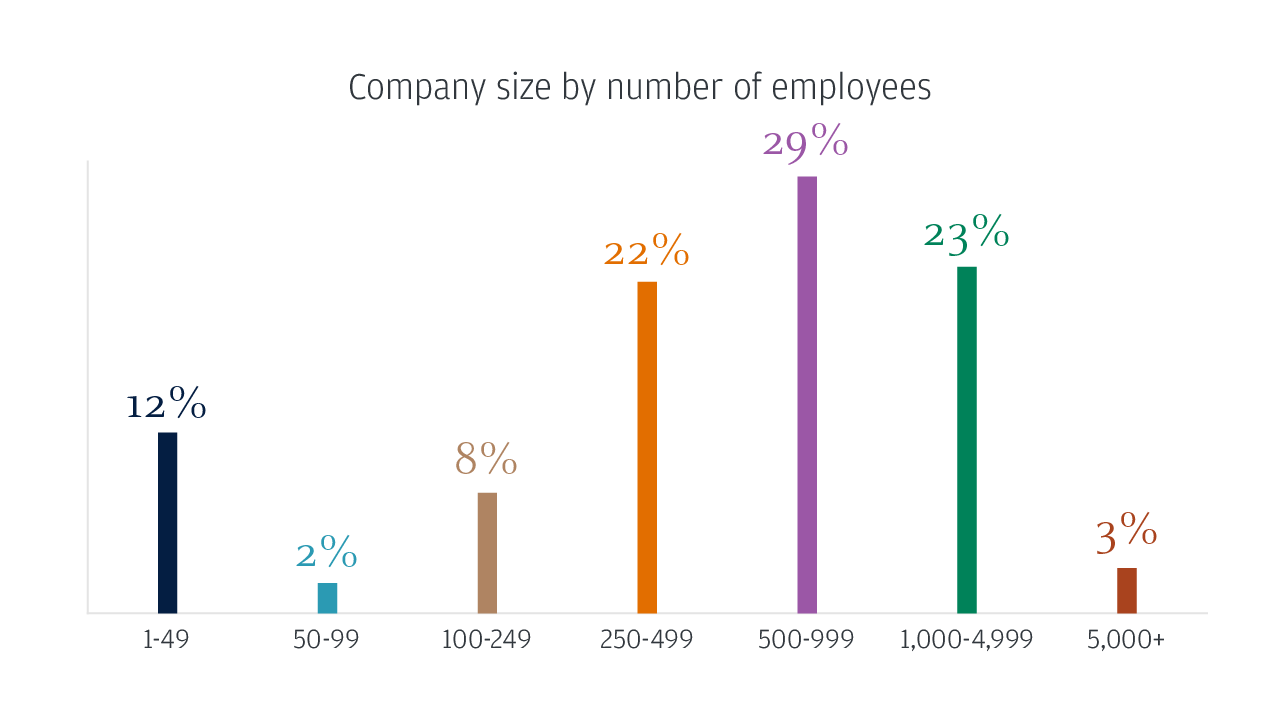

Company size by number of employees

1-49: 12%

50-99: 2%

100-249: 8%

250-499: 22%

500-999: 29%

1,000-4,999: 23%

5,000+: 3%

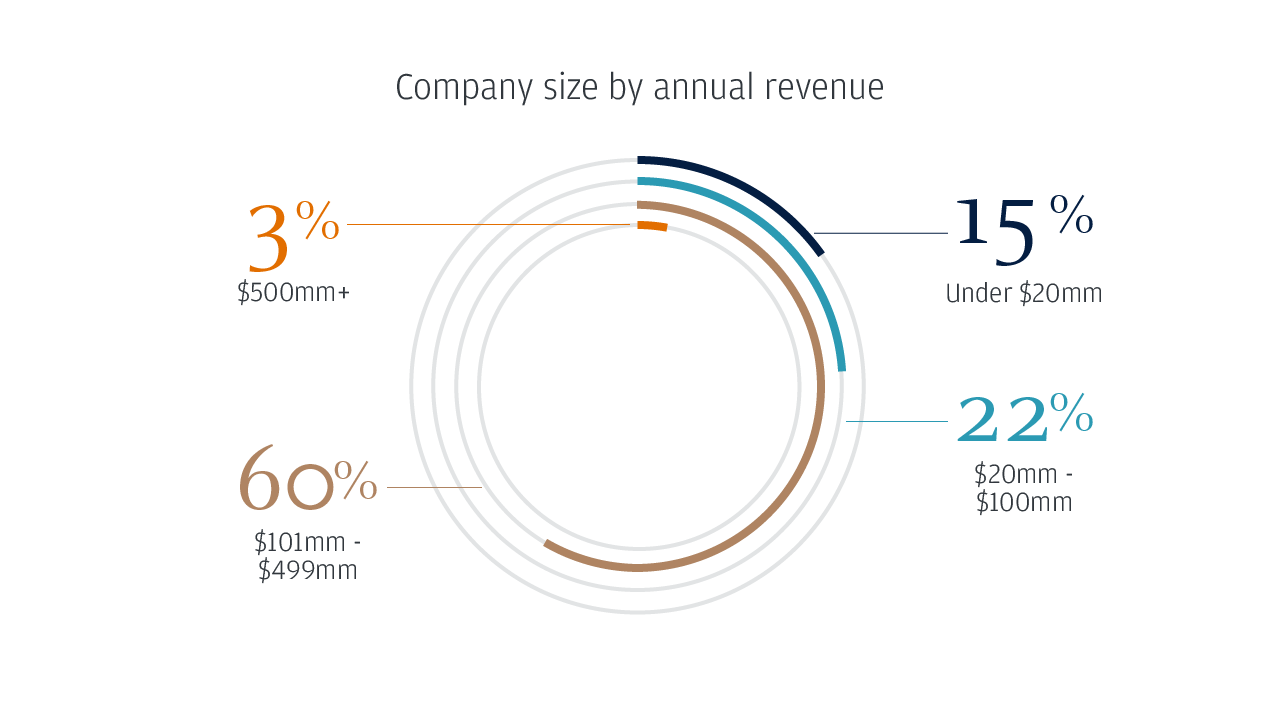

Company size by annual revenue

Under $20mm: 15%

$20mm - $100mm: 22%

$101mm - $499mm: 60%

$500mm+: 3%

Note: Some numbers may not equal 100% due to rounding.

Contributors

Kerry Jessani

Head of Healthcare, Higher Education & Not-for-Profit at J.P. Morgan Commercial Banking, Middle Market Banking & Specialized Industries

Lauren Ruane

Co-Head of Healthcare, Middle Market Banking & Specialized Industries Commercial Banking, J.P. Morgan

JPMorgan Chase Bank, N.A. Member FDIC. Visit jpmorgan.com/cb-disclaimer for disclosures and disclaimers related to this content.

Midyear survey

Hide

Midyear survey

Hide