The U.S. Census Bureau estimates that total e-commerce sales for 2020 grew about 32 percent from 2019, sending a clear message that consumer shopping habits have shifted digital.1 To meet demand—which has been accelerated even more by the COVID-19 pandemic—consumer brands are adopting new digital operating models like direct-to-consumer (D2C), direct-to-store and online marketplaces.

Now, corporate treasury and payments teams need to prepare their businesses to succeed amidst this digital transformation. Every consumer brands business is unique, but a strong treasury and payments process on the backend will help ensure that the company can achieve strategic goals. And treasurers can’t go at it alone; they will need to collaborate across teams.

From business, operations and IT to procurement, here are four key conversations corporate treasury teams should be having.

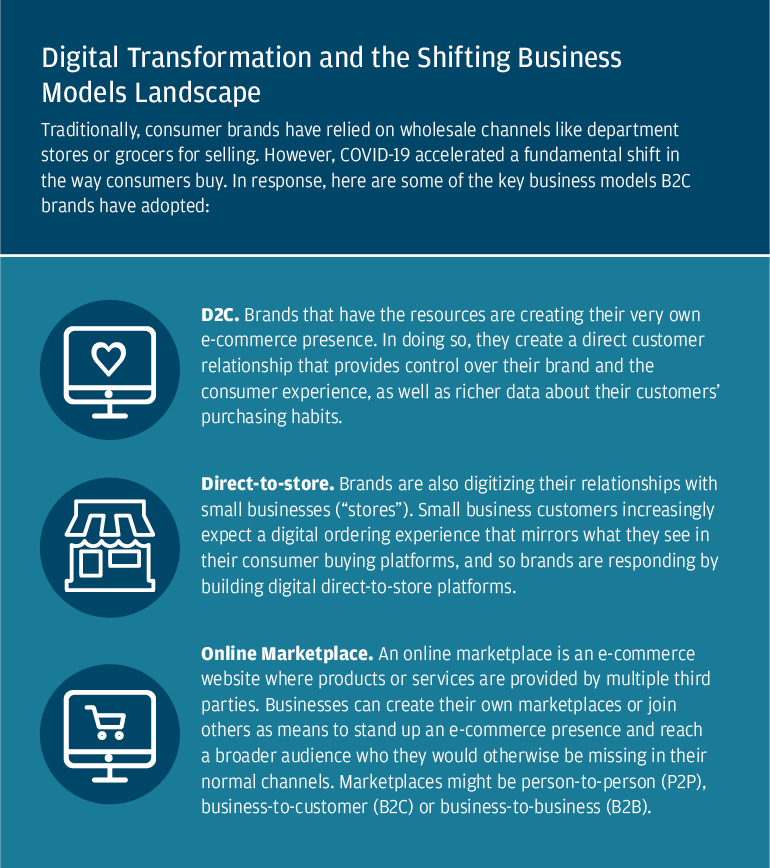

Digital transformation and the shifting business models landscape

Traditionally, consumer brands have relied on wholesale channels like department stores or grocers for selling. However, COVID-19 accelerated a fundamental shift in the way consumers buy. In response, here are some of the key business models B2C brands have adopted:

- D2C. Brands that have the resources are creating their very own e-commerce presence. In doing so, they create a direct customer relationship that provides control over their brand and the consumer experience, as well as richer data about their customers’ purchasing habits.

- Direct-to-store. Brands are also digitizing their relationships with small businesses (“stores”). Small business customers increasingly expect a digital ordering experience that mirrors what they see in their consumer buying platforms, and so brands are responding by building digital direct-to-store platforms.

- Online Marketplace. An online marketplace is an e-commerce website where products or services are provided by multiple third parties. Businesses can create their own marketplaces or join others as means to stand up an e-commerce presence and reach a broader audience who they would otherwise be missing in their normal channels. Marketplaces might be person-to-person (P2P), business-to-customer (B2C) or business-to-business (B2B).

How to align your treasury and payments tools with the business strategy

Just 60 percent of consumer-goods brands feel moderately prepared to capture e-commerce growth opportunities, according to a McKinsey report.2 Therefore, it’s important to understand the key drivers behind the business model shifts—including business objectives, customer engagement strategy and valuation.

This initial groundwork should help layout a clear strategy and qualify the opportunity. And with corporate treasury playing an increasingly strategic role within the business, you will be better prepared to identify the necessary treasury and payments capabilities to execute on that vision.

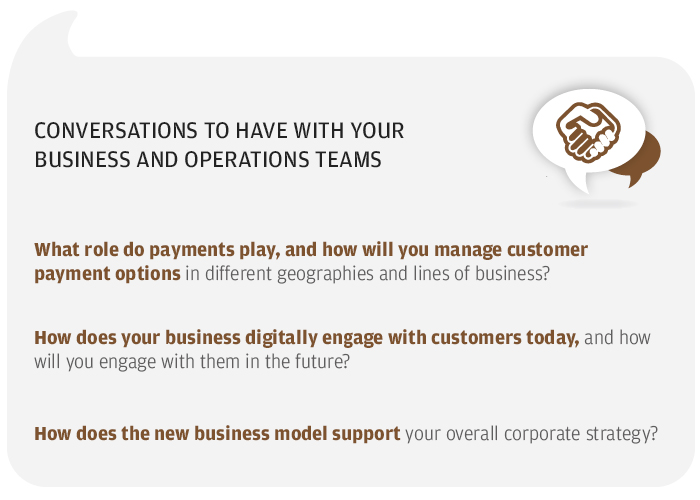

Conversations to have with your business and operations teams

- How does the new business model support your overall corporate strategy?

- How does your business digitally engage with customers today, and how will you engage with them in the future?

- What role do payments play, and how will you manage customer payment options in different geographies and lines of business?

How to build your treasury and payments tech infrastructure

Examine the impact new business models will have on your cash flows, finance functions and the systems supporting those processes. Traditionally, businesses have multiple systems and platforms used for different sales channels and inventory systems. Now, D2C and online marketplaces present yet another set of channels to reach a broader audience who demand a seamless, immediate and secure shopping experience. Reducing fragmentation across systems is important to eliminate potential friction.

You may also need to enable new payment methods to meet those expectations—for instance, e-wallets, bank transfers or direct debits. Not to mention transaction volumes and chargebacks will likely increase. Preparation will require oft-precious IT resources; here are the questions you should be asking your IT teams.

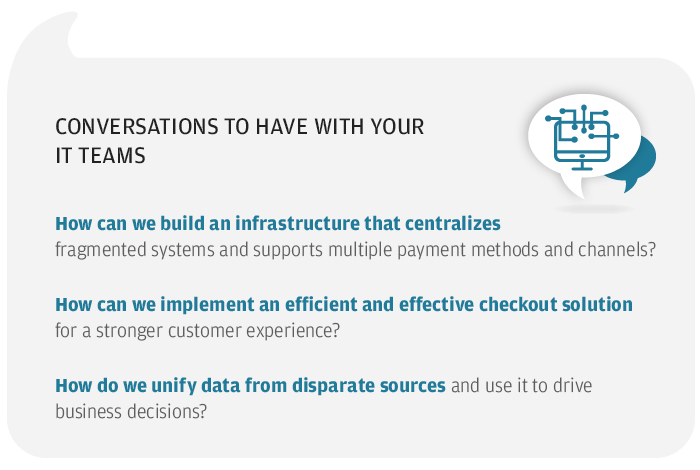

Conversations to have with your IT teams

- How can we build an infrastructure that centralizes fragmented systems and supports multiple payment methods and channels?

- How can we implement an efficient and effective checkout solution for a stronger customer experience?

- How do we unify data from disparate sources and use it to drive business decisions?

How to standardize payments for procurement

Omnichannel defines much of the current consumer shopping experience. And within this dynamic space, corporate treasury teams should consider how a strong supply chain can support. Start by understanding how you can minimize out-of-stocks by rethinking how market and supplier data are used across supply chain processes to identify and meet fluctuating consumer demand. By maximizing visibility, these insights help your business understand what your suppliers need and when they need it.

Also consider how to drive value through supply chain optimization. Businesses that balance working capital optimization, sourcing costs and supplier relationships are positioned to outperform others. Leveraging a holistic strategy can help enhance working capital for the buyer and seller—meanwhile creating potential opportunities to monetize payment flows. Get the conversations started with your sourcing and procurement teams with these questions.

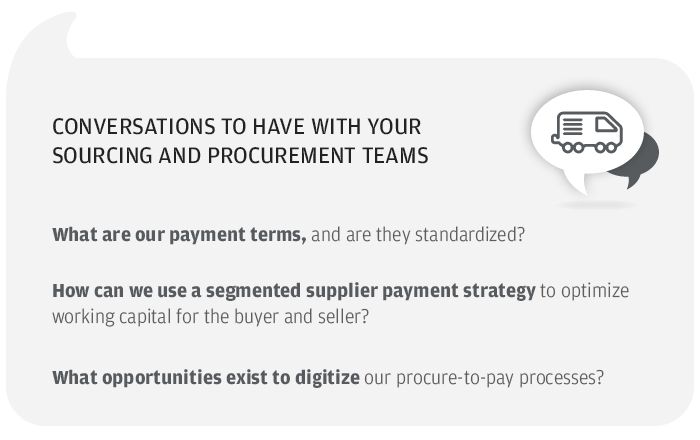

Conversations to have with your sourcing and procurement teams

- What are our payment terms, and are they standardized?

- How can we use a segmented supplier payment strategy to optimize working capital for the buyer and seller?

- What opportunities exist to digitize our procure-to-pay processes?

How to improve resiliency across treasury, payments and the business

More channels to sell through; more fluctuation to account for. Due to COVID-19, brands have started keeping higher levels of cash within the business to help cope with uncertainty. However, as the world continues its path to “normal,” corporate treasury and resiliency teams should consider the role of active, passive and seasonal (e.g., Black Friday, Cyber Monday) liquidity management as the business engages with consumers in more ways.

Technology solutions can help address those needs. For instance, cash concentrations and investments can be automated. Likewise, peak demands for goods can become predictable events when you integrate machine learning into your systems. As your teams explore how best to manage liquidity, start with this key question.

Conversations to have amongst your own corporate treasury teams

- What data do I need in order to improve cash flow forecasting?

Preparing to grow your business in new ways

Digital transformation is not going anywhere. Pandemic or not, more than two-thirds of consumers plan to continue shopping online.2 Therefore, consumer brands need to develop their strategy and build the infrastructure for a digital-first business. Corporate treasury can help as the driver for fundamental business change by ushering their core teams to a new model of e-commerce and sales growth.

As you engage in these conversations, you don’t have to do it alone. With more ways of doing business, you will need to address the inherent complexities across reconciliation, reporting and risk. J.P. Morgan is committed to helping you on your journey and crafting tailored solutions to meet your needs along the way.

Connect with your J.P. Morgan representative to get started today.

References

"Quarterly Retail E-commerce Sales 4th Quarter 2020," U.S. Census Bureau, February 19, 2021. https://www.census.gov/retail/mrts/www/data/pdf/ec_current.pdf

“DTC e-commerce: How consumer brands can get it right,” McKinsey, November 30, 2020. https://www.mckinsey.com/business-functions/marketing-and-sales/our-insights/dtc-e-commerce-how-consumer-brands-can-get-it-right

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of J.P. Morgan, its affiliates, or its employees. The information set forth herein has been obtained or derived from sources believed to be reliable. Neither the author nor J.P. Morgan makes any representations or warranties as to the information’s accuracy or completeness. The information contained herein has been provided solely for informational purposes and does not constitute an offer, solicitation, advice or recommendation, to make any investment decisions or purchase any financial instruments, and may not be construed as such.

JPMorgan Chase Bank, N.A. Member FDIC.

JPMorgan Chase Bank, N.A., organized under the laws of U.S.A. with limited liability.