Direct-to-Consumer (“D2C”) brands have undergone a rapid ascent—maturing from niche “digital-born” challengers to genuine disrupters of the consumer and retail space. As of Q4 2019, over 400 of these brands were estimated to be active globally, and collectively they have taken significant market shares across consumer product staples such as footwear (15%), mattresses (20%) and razors (12%).1

On the supply side, D2C models have been enabled by lowering barriers to entry across the value chain:

- First, advancement in cloud-based capabilities and “outsourcing platforms” have enabled the emergence of “Supply Chain as a Service” across the production lifecycle, reducing upfront capital expenditures and fixed unit costs.

- Second, the rise of social media as a credible marketing channel has enabled cost-effective and targeted advertising of target consumers, allowing upstart D2C brands to leap frog into public consciousness through viral marketing campaigns.

- Third, advanced analytics (including those offered by marketplaces) have enabled D2C brands to adopt dynamic “just-in-time” inventory models, lowering their working capital needs across the cycle, and to leverage payments data to drive product and strategic decision-making in real time.

On the demand side, consumer expectations are also shifting. With the oldest millennials turning 40 in 2020, the consumer landscape is shifting such that bulk of spending power will reside with the first “native digital” generation—with an estimated collective spending power of $1.4 trillion in 2020 in the US alone2. Latest estimates for 2020 peg the number of D2C customers as over 87 million in the U.S., up 10.3% year-on-year.3

While nuances exist across different countries and markets, consumer surveys of millennial and Generation Z consumers have found consistent themes around the importance they place on customization, credible value propositions and cohesive “brand stories”4 which are increasingly being met by these D2C challengers.

In the face of this, established consumer and retail players have not stood still. Across multiple categories—including consumer packaged goods (“CPG”) and apparel—a number of incumbents have taken an active interest in establishing their own D2C channels. Some have pursued the M&A route of D2C brands (i.e., Unilever’s acquisition of Dollar Shave Club5), whereas others looked to acquire “bolt-on” capabilities to underpin own brand D2C channels (i.e., Nike’s acquisition of Zodiac, a data analytics firm6).

Taken together, whilst the above point to a multi-year “quiet revolution” driven by structural industry and consumer trends, the onset of the COVID-19 crisis at the start of 2020 has clearly sharpened the focus on D2C and e-commerce channels. As social distancing measures took hold, forcing a shuttering of non-essential stores, retailers with established online D2C channels have been more resilient in their ability to meet consumer demand. Going forward, we may see a greater share of companies pivot to D2C channels as a resilience strategy.

Regardless of the motivation, the challenges around engineering D2C pivots are broadly consistent.

Our conversations with clients have surfaced of the following topics and challenges:

- How to design and deliver multiple pay-in and pay-out methods of payment to reach the widest reach of clients?

- How to manage payment economics as businesses move from “one-to-few” B2B models to “one-to-many,” high volume and lower value receivables?

- How to manage liquidity, reconciliation and reporting in a “one-to-many” and high velocity payments ecosystem?

- How to enable cross-border flows while managing cross-currency risk and access to low cost payment channels?

- How to warehouse and protect consumer data across different jurisdictions?

- How to manage more complex inventory (e.g., retail SKU vs. wholesale packaging)?

- How treasury can get involved in the strategic discussions (e.g., user journey, pricing, margin growth), as payments migrate from a “utility function” to a strategic differentiator in high-velocity business models?

While we think addressing these challenges is a baseline for any treasurer operating in a D2C space, it is also clear that idiosyncratic challenges will be influenced by the company’s starting point, legacy operating model and its chosen D2C strategy.

How different D2C models shape treasury challenges

- “Pure play” D2C: These are the digital-native companies that sell directly to end-consumers through their own e-commerce channels or through third-party marketplaces. Models vary from single-brand merchandisers (e.g., mattresses) to subscription-based (e.g., shaving products)

- Treasury challenges:

- Supporting high velocity growth through scalable platforms

- Expansion into new markets (payment methods, capital controls, foreign exchange and supply chain complexities)

- Choice of infrastructure partners (e.g., acquirer, customer relationship management, distribution)

- Leveraging payments data to capture consumer insights and inform business decisions

- Treasury challenges:

- Organic expansion into D2C: Companies that traditionally operated in the B2B space or sold through intermediaries (e.g., retailers and pharmacies) that are starting to build e-commerce hubs for their own brand products

- Treasury challenges:

- Upgrade and integrate legacy systems

- Leverage payments data to capture consumer insights

- Faster and more complex working capital cycle

- Outsource vs internally build sales & logistics channels

- Managing economics and risk in low-value payments (e.g., card chargebacks, direct debit returns)

- Treasury challenges:

- M&A-led expansion into D2C: Companies that traditionally operated in the B2B space that have expanded into D2C by acquiring fast-growing “pure play” D2C brands, tapping into new brands and customer demographics

- Treasury challenges:

- Visibility/understanding of new operating model & cash flows

- Integration of acquisition into existing infrastructure (as a stop to broader

- Leveraging acquired technology/capabilities more broadly

- Ability to align company/treasury policies without impacting business momentum

- Treasury challenges:

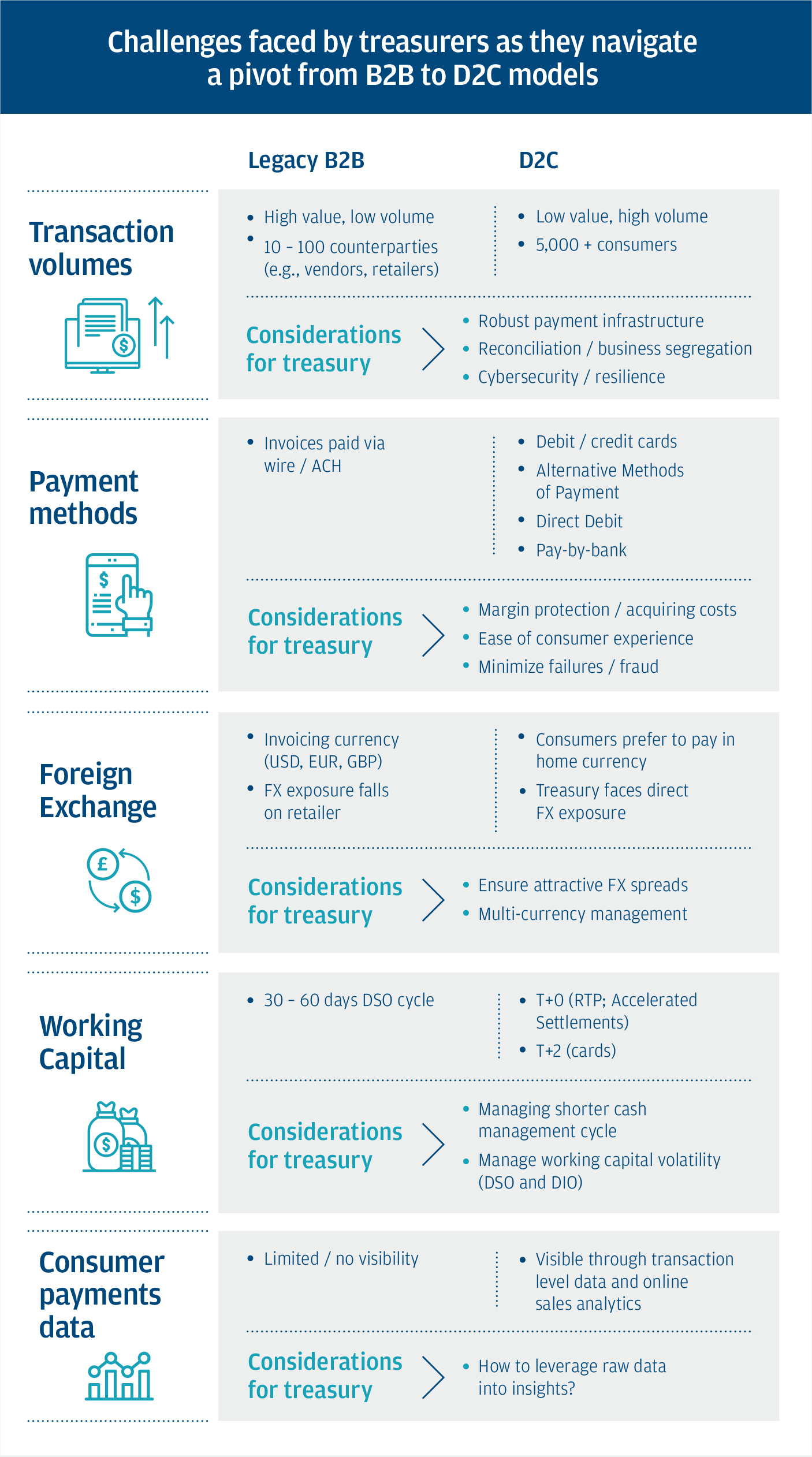

The exhibit below lays out in more detail the scale and scope of challenges faced by treasurers navigating a transition from “legacy” B2B models to D2C models (whether organically developed or via M&A)

Challenges faced by treasurers as they navigate a pivot from B2B to D2C models

Transaction volumes

Legacy B2B

- High value, low volume

- 10 – 100 counterparties (e.g., vendors, retailers)

D2C

- Low value, high volume

- 5,000 + consumers

Considerations for treasury

- Robust payment infrastructure

- Reconciliation / business segregation

- Cybersecurity / resilience

Payment methods

Legacy B2B

- Invoices paid via wire / ACH

D2C

- Debit / credit cards

- Alternative Methods of Payment

- Direct Debit

- Pay-by-bank

Considerations for treasury

- Margin protection / acquiring costs

- Ease of consumer experience

- Minimize failures / fraud

Foreign Exchange

Legacy B2B

- Invoicing currency (USD, EUR, GBP)

- FX exposure falls on retailer

D2C

- Consumers prefer to pay in home currency

- Treasury faces direct FX exposure

Considerations for treasury

- Ensure attractive FX spreads

- Multi-currency management

Working Capital

Legacy B2B

- 30 – 60 days DSO cycle

D2C

- T+0 (RTP; Accelerated Settlements)

- T+2 (cards)

Considerations for treasury

- Managing shorter cash management cycle

- Manage working capital volatility (DSO and DIO)

Consumer payments data

Legacy B2B

- Limited / no visibility

D2C

- Visible through transaction level data and online sales analytics

Considerations for treasury

- How to leverage raw data into insights?

Making the pivot to D2C: How to be a partner to your business?

More so than ever, what happens in treasury has implications for the business. This is increasingly the case as companies respond to a broader e-commerce disruption, of which D2C is a particular example.

As a treasurer, what should you be thinking about as your company embarks on this journey?

- Is the company adopting an in-house managed D2C approach or outsourcing to a third party? What are the implications of these models on cash flow exposure to third parties and control over transactional costs?

- Do you have a credible end-consumer payment strategy that is aligned to the company’s business and country strategy? How are you stress testing your assumptions with your business counterparts?

- Is your platform/legacy system ready to handle the scale of flows? If not, what is your transition/migration plan? What is the impact of this on the expected user experience?

- Which treasury and payment capabilities should you look to build in-house vs. those that you would outsource to partners?

J.P. Morgan understands that each company faces a unique set of challenges and priorities as it considers participation into the D2C space. That is why we offer a variety of products and services, including innovative treasury and payment tools, to help clients respond to the challenges they face.

In an increasingly complex cross-border environment, we also offer a combination of local capabilities and global reach that can help you tap into the world’s largest growth markets while maintaining your focus on your core business priorities.

To learn more, please contact your J.P. Morgan representative.

This material was prepared exclusively for the benefit and internal use of the JPMorgan client to whom it is directly addressed (including such client’s subsidiaries, the “Company”) in order to assist the Company in evaluating a possible transaction(s) and does not carry any right of disclosure to any other party. This material is for discussion purposes only and is incomplete without reference to the other briefings provided by JPMorgan. Neither this material nor any of its contents may be disclosed or used for any other purpose without the prior written consent of JPMorgan.

J.P. Morgan, JPMorgan, JPMorgan Chase and Chase are marketing names for certain businesses of JPMorgan Chase & Co. and its subsidiaries worldwide (collectively, “JPMC”). Products or services may be marketed and/or provided by commercial banks such as JPMorgan Chase Bank, N.A., securities or other non-banking affiliates or other JPMC entities. JPMC contact persons may be employees or officers of any of the foregoing entities and the terms “J.P. Morgan”, “JPMorgan”, “JPMorgan Chase” and “Chase” if and as used herein include as applicable all such employees or officers and/or entities irrespective of marketing name(s) used. Nothing in this material is a solicitation by JPMC of any product or service which would be unlawful under applicable laws or regulations.

Investments or strategies discussed herein may not be suitable for all investors. Neither JPMorgan nor any of its directors, officers, employees or agents shall incur in any responsibility or liability whatsoever to the Company or any other party with respect to the contents of any matters referred herein, or discussed as a result of, this material. This material is not intended to provide, and should not be relied on for, accounting, legal or tax advice or investment recommendations. Please consult your own tax, legal, accounting or investment advisor concerning such matters.

Not all products and services are available in all geographic areas. Eligibility for particular products and services is subject to final determination by JPMC and or its affiliates/subsidiaries. This material does not constitute a commitment by any JPMC entity to extend or arrange credit or to provide any other products or services and JPMorgan reserves the right to withdraw at any time. All services are subject to applicable laws, regulations, and applicable approvals and notifications. The Company should examine the specific restrictions and limitations under the laws of its own jurisdiction that may be applicable to the Company due to its nature or to the products and services referred herein.

Notwithstanding anything to the contrary, the statements in this material are not intended to be legally binding. Any products, services, terms or other matters described herein (other than in respect of confidentiality) are subject to the terms of separate legally binding documentation and/or are subject to change without notice.

JPMorgan Chase Bank, N.A. Member FDIC.

JPMorgan Chase Bank, N.A., organized under the laws of U.S.A. with limited liability.