Automate administrative functions, simplify cardholder tasks and streamline account reconciliation.

Treasury

Contact us

Commercial Card Programs

Our commercial credit card solutions can help your company organize, manage and automate payments with versatile controls and robust reporting.

Why choose J.P. Morgan?

Our suite of commercial cards can be tailored to suit your company's needs and evolve with you through all stages of your growth.

One Card

Reduce costs and streamline your payments for business travel, entertainment and other expenses.

- Singular spend controls: One set of controls for spend limit, cardholder fraud alerts and merchant categories.

- Robust data and reporting: One data management tool for card account activity, reconciliation, reporting or exporting, and one spend reporting structure.

- Maximized rebates: Consolidate spend to increase rebate earning potential.

Corporate Card

Implement an integrated, configurable travel and expense (T&E) solution.

- Increased T&E efficiency: Leverage J.P. Morgan expertise and analytics to assess past performance and operate an optimal expense management program.

- Fraud protection: Alerts quickly inform cardholders of unusual transactions.

- Hassle-free payments: Cardholders can upload to a mobile wallet and pay vendors worldwide.

Purchasing Card

Manage B2B procurement spending more strategically with a p-card solution.

- Increase rebate potential: Earn on your procurement payables.

- Protect purchases: End-to-end controls reduce chances for fraud or misuse.

- Optimized payments: Extend days payable outstanding (DPO) while paying suppliers sooner.

Virtual Card

Integrate digital card payments into your accounts payable.

- Single-use card functions: Send unique card numbers to specific suppliers for a preset amount valid for a specific time frame.

- Capture more rebate-earning spend: Reduce the use of checks, ACH and wire and earn rebates on card payments.

- Improve security and control: Virtual cards experience nearly zero percent fraud3, supported by robust spend controls.

Compare our solution benefits

Our card controls can be customized to fit the contours of your organization's spending needs. Explore which product can help you achieve your goals.

One Card

Manage multiple types of spend, simplify administration, control purchasing, monetize expenses and improve cardholder experience.

Corporate Card

Give cardholders a hassle-free way to pay with a configurable T&E expense solution that can increase efficiency, establish controls and protect against fraud.

Purchasing Card

Manage your B2B procurement spending more strategically, increase your rebate revenue potential, enhance fraud protection and optimize supplier payments.

Virtual Card

Digitize supplier payments, increase security and extend days payable outstanding without impacting cash flow, and transform traditional areas of expense into potential revenue generators.

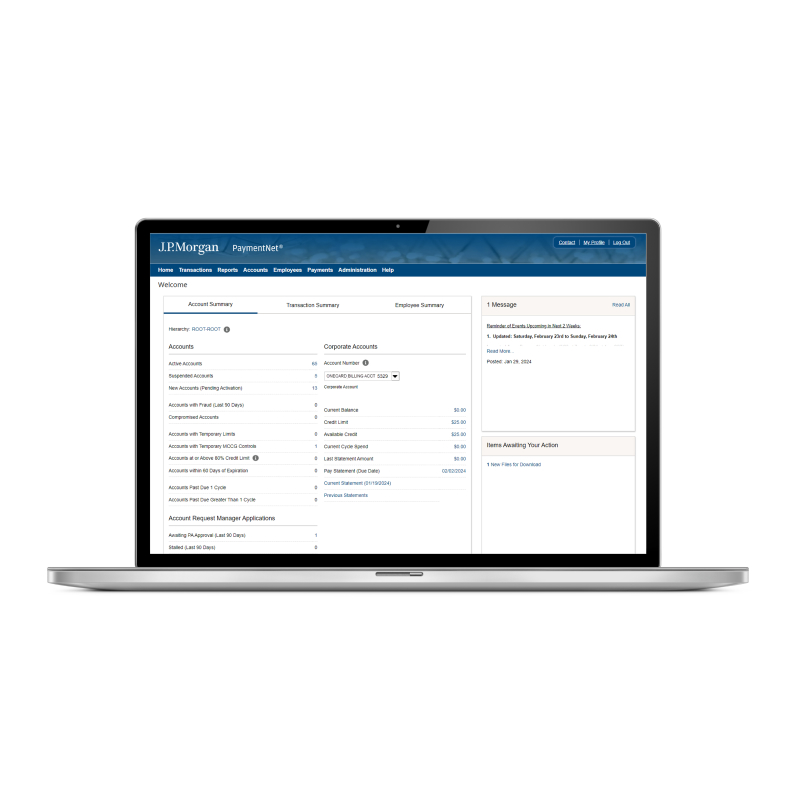

Customizable card-management platform

Set controls and promote policy adherence across different divisions, locations and departments.

Access standardized and custom reporting to gain transparency into your spend, and insights into what’s important to your company.

Hear from our clients

Treasury

Excel in the growing digitized payments environment

Ashton Woods leveraged a leading commercial card solution to facilitate online transactions, support operations and growth, and reap benefits from the card’s cutting-edge rebate program.

Support where and when you need it

We’ll help you take advantage of our platform to save time, reduce administrative costs and gain greater control over your spend.

Call or email anytime to manage card operation issues.

Driving commercial card program success

When you begin a card program with us, we’ll dive deep into program design, push hard on control measures and sweat the details to help you achieve your goals. Even if you have an existing program, our industry experts can offer a fresh look at your goals and help you achieve stronger results.

Design

Our consultative, tailored approach can help you determine the best setup for your organization’s specific needs.

Build

Our team does the heavy lifting—so you don’t have to. We’ll dig into program configuration details, including systems integration and reporting.

Launch

Before the program goes live, benefit from training, communications templates and best practices to share across your company.

Treasury

Pay suppliers with a credit card

January 17, 2025

Credit card payments can help improve your cash flow and enhance security. Learn how to implement card payments and gain supplier acceptance.

Read moreCommercial card FAQs

When implemented and managed effectively, commercial cards can drive significant value for companies in several ways, including streamlined payment processing, enhanced tracking and reporting, cost savings and efficiency, and improved oversite.

Companies can reduce costs, earn rebates and improve bottom-line results. They can integrate more payment options into their processes, cut down on manual work and protect against fraud and misuse.

The responsibility for payment is determined by the terms of each program’s agreement. Unlike personal or business credit cards, corporate cards often use corporate liability—meaning the company is responsible for paying for all the charges made to the cards, rather than the employee or business owner.

Related solutions

Related solutions

Global Treasury Solutions

Future-ready treasury solutions- craft your vision with confidence and execute at scale.

Cross-Currency Solutions (FX)

Take advantage of solutions that allow you to send in 120 currencies and receive in 40 across 200+ countries and territories.

Liquidity Solutions

Access and manage your cash 24/7 with advanced liquidity solutions that offer greater visibility, control and optimization.

Account Solutions

Get a roadmap to a future-ready treasury with the right account strategy.

Receivables Solutions

Automate and improve your working capital.

Payment Solutions

Automate payments, enhance security, offer strategic payment options and boost customer and vendor satisfaction.

Related insights

2:54 - Treasury

Virtual cards: The future of B2B payments

Mar 30, 2026

Learn how virtual cards can help businesses streamline B2B payments with enhanced control, visibility and automation.

Watch video

Payments

What is PCI compliance?

Mar 25, 2025

Protect your business and customer relationships through strong payment security. Learn how PCI DSS requirements safeguard card data and help prevent fraud while building trust.

Read more

Payments

What are card-issuing APIs?

Mar 20, 2025

Card issuing application programming interfaces (APIs) can help enhance the efficiency, security and overall management of corporate credit card programs.

Read more