Based on ongoing client conversations and engagements, this article sets out our perspective on treasury transformation in three parts:

- The challenges faced by treasurers operating within de-centralized or fragmented set-ups.

- Three “quick wins” that allow treasurers to enhance visibility and control while minimizing disruption to critical processes and infrastructure.

- A roadmap to New Treasury, with a goal of lifting treasury into a strategic partner to the C-suite in solving for structural trends and strategic priorities.

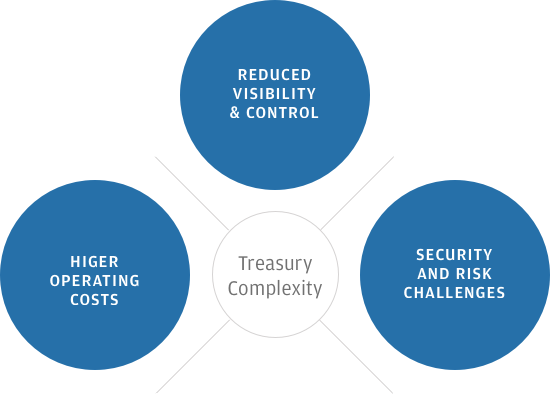

Treasury complexity: drivers and implications

Our engagement with treasurers has surfaced treasury complexity and the resulting lack of visibility and control as persistent pain points.

While specific drivers will vary across and within industry segments and individual corporates, such treasury set-ups are often driven by the company’s history, de-centralized operating models, M&A activity, and local regulatory requirements.

Irrespective of the underlying drivers, an overly complex treasury set-up gives rise to a number of issues:

Treasury Complexity

- Reduced Visibility & Control

- Security and Risk Challenges

- Higher Operating Costs

- Reduced visibility and control into the company’s cash position across the globe. The 2019 PWC Global Treasury Benchmarking Survey of treasurers concluded that “more than a quarter of global cash is not visible to corporate treasury on a daily basis”.1

- Higher operating costs. The more banks a corporate has, the more likely it is that fees and spreads will be not aligned on an enterprise-wide level. In addition, each bank may have its own channels and submission methods and formats, creating additional costs related to maintenance, testing, and reconciliation.

- Security and risk challenges. The more accounts and the more connectivity methods a corporate has, the more entry points there are. As cybersecurity risks mount, corporates are paying more attention to areas of potential vulnerability. 85% of corporates surveyed by PWC have said that their organizations were affected by payment fraud attempts, with 1 in 4 reporting weekly or more frequent attempts.2

While treasurers we speak to are well aware of these issues, they are simultaneously operating in an environment of competing priorities and limited investment budgets.

"We see a strong case to capture “quick wins” that can deliver benefits within a short-time frame and with minimal disruption to critical processes and infrastructure."

Treasury “quick-wins” to achieve visibility & control

Quick Win #1: Achieve real-time cash visibility through APIs

Visibility on cash balances is the primary building block of an effective treasury. In a typical “de-centralized” set-up (i.e., accounts at subsidiary levels across multiple banks), central treasury relies on SWIFT MT940 messages to establish end-of-day balances. Those in turn are integrated into treasury management systems to establish the end-of-day balances on a stand-alone and consolidated basis.

The drawbacks of such an approach are becoming more apparent, which include but are not limited to: manual processes, complex reconciliation and forecasting, and costs that rise in-line with the complexity of group structures. Moreover, the “batch processing” approach does not provide treasurers with real-time data, which could be especially relevant to high velocity businesses such as e-commerce, marketplaces and direct-to-consumer models.

In this context, application program interfaces (“APIs”) can provide real-time multi-bank connectivity that could transform intra-day visibility. Using dedicated APIs, treasury can ‘call on’ any connected account to establish the balance and transaction-level data – both on an intraday and end-of-day basis., Crucially, APIs are compatible with SWIFT rails and message types that are familiar to treasurers, allowing for ease of implementation within existing infrastructure.

At J.P. Morgan, we see the evolution of “Multi-Banking 2.0” as a key solution for corporates operating in high-velocity, cross-border payment environments, and have established a developer portal and partnered with clients to deliver tailored API-powered account visibility and connectivity solutions.

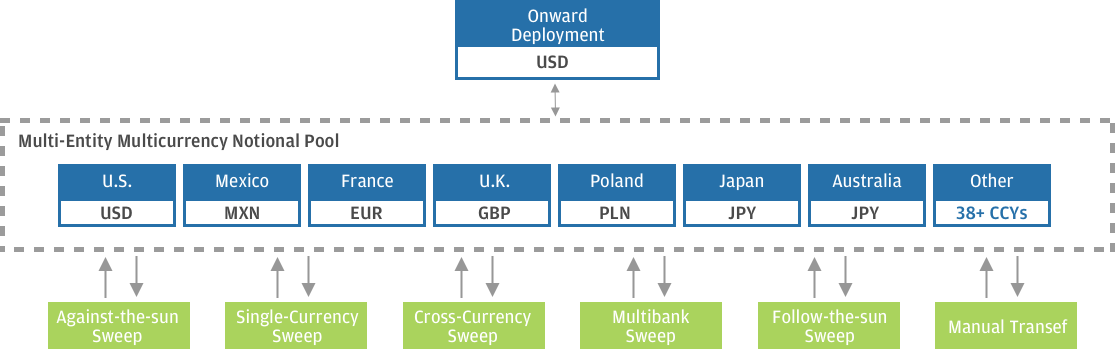

Quick Win #2: Set-up tailored liquidity overlays

Having achieved greater visibility, a treasurer’s next focus should turn to optimizing the management and value of cash positions across multiple subsidiaries and currencies.

In typical de-centralized set-ups (i.e., absence of “on-behalf-of” structures), subsidiaries transact payables and receivables at an entity account level, with accounts building up balances and others going into overdraft on a daily basis. On an operational level, this approach drives up operating costs (e.g., overdraft expenses) and may increase the need for FX conversions to meet the subsidiary’s multi-currency needs. Strategically, fragmented cash positions diminish the ability of treasury to centralize funding requirements across the group, match liquidity where it is needed, or optimize returns on excess cash.

Treasurers can generate considerable value by creating overlay structures through notional pooling. In a simple example of a multi-entity multi-currency notional pool, each participating entity retains autonomy of its own funds in the structure. As shown in the diagram, balances in operating accounts (including third-party banks) are swept on an automated basis at close of business into corresponding accounts that sit within the notional pool, consolidating the liquidity position across the group into a single structure.

The notional pool provider would then calculate interest on the “net position” of the pools across the various currencies into a base currency chosen by the client. Where the appetite exists, the treasurer can also opt to deploy “surplus cash” into investment alternatives or pay down debt.

NEED TEXT VERSION

Tailored appropriately, a liquidity overlay offers a number of benefits:

- Centralized liquidity for visibility and control into groups cash position.

- Minimized interest expense by off-setting debit and credit positions.

- Release of working capital (enhancing ability to self-fund operations or pay down debt).

- Enhanced returns on excess cash.

- Preserved autonomy, control and record keeping at an entity level.

- Minimized disruption to existing processes and infrastructure.

Quick Win #3: Streamline multi-currency management

Our conversations with treasurers continue to highlight multi-currency management as an area of sharpening focus. From a strategic perspective, exposure to FX fluctuations has increased as corporates have developed cross-border supply chains and extended their footprints towards growth markets – requiring effective multi-currency management models.

From a treasurer’s perspective, FX is also relevant to the day-in day-out operations. This includes payments to suppliers, receivables from customers, meeting global payroll and other aspects where corporate subsidiaries transact with each other across borders and currencies.

The traditional approach for many corporates has been to implement a hybrid model to multi-currency management, where balances above a certain threshold are managed more centrally (i.e., regional treasury centers) and those below are managed at subsidiary level. The result is a patchwork of operational accounts with local banking providers across “core” and “non-core” currencies.

However, as operational complexity grows, such set-ups may contribute to lower visibility, fragmented liquidity, and higher operating costs.

In addition to the direct costs, it is also arguable that fragmenting multi-currency management may incur material opportunity costs. These could arise as subsidiaries negotiate transactional FX spreads across multiple providers, without tapping into scale benefits that could be realized at a corporate or group level. Moreover, companies operating in such an environment often rely on wires as their means to transfer funds across currencies and entities, driving up transaction costs and potentially denting their operational margins.

In order to address these issues, J.P. Morgan has developed a number of multi-currency tools and solutions that aim to simplify treasury tasks while meeting clients sophisticated needs. For example, Global Mass Pay® enables clients to send or collect funds in 58 currencies through automated clearing houses (“ACH”). This solution provides a cost effective alternative to wires, ensures principal protection and sets the stage for account rationalization by eliminating the need for local disbursement accounts.

In addition, we have developed a number of solutions that can deliver value to our corporate clients across their transactional FX needs. J.P. Morgan Access® delivers multi-currency capabilities including FX Center, which provides clients with the opportunity to utilize consistent FX spreads across multiple subsidiaries, allowing them the benefits of scale and an industry-leading FX and payments platform.

The roadmap to a “future-ready” treasury

Treasury transformation is a multi-year journey with no “one size fit all” approach. In our experience advising a number of clients, the steps outlined above can set the stage for a broader transformation journey.

Treasurers can lay the foundation for a “future-ready” treasury that can help them navigate uncertainty while simultaneously looking to capture emerging opportunities.

The path for such a journey includes:

- Map the journey to New Treasury: to be achieved through optimization and automation initiatives (e.g., account rationalization, setting up in-house banks, “on behalf of” payment structures) and utilizing new treasury tools such as virtual accounts and advanced forecasting where applicable.

- Tap into the “direct-to-consumer” revolution: by forging closer partnerships with internal stakeholders (e.g., customer acquisition, strategy and IT) and external partnerships (e.g., banks, fintechs), positioning treasury as a strategic pillar in the end-to-end customer journey.

- Set out and implement a robust cybersecurity strategy: with cyber-attacks and payment fraud incidents on the rise – the treasurer’s role in safeguarding financial assets and payment infrastructure will continue to gain greater urgency. With 45% of CFOs naming cybersecurity as a priority, the case for a comprehensive and thoughtful cybersecurity strategy has rarely been stronger.3

Future articles in the New Treasury series will set out our views on these themes and implications for treasurers’ strategic priorities and agendas.

To learn more, please contact your J.P. Morgan Treasury Services representative.

This article was prepared exclusively for the benefit and internal use of the JPMorgan client to whom it is directly addressed (including such client’s subsidiaries, the “Company”) in order to assist the Company in evaluating a possible service and does not carry any right of disclosure to any other party. This article is incomplete without reference to the other briefings provided by JPMorgan. Neither this article nor any of its contents may be disclosed or used for any other purpose without the prior written consent of JPMorgan.

J.P. Morgan, JPMorgan, JPMorgan Chase and Chase are marketing names for certain businesses of JPMorgan Chase & Co. and its subsidiaries worldwide (collectively, “JPMC”). Products or services may be marketed and/or provided by commercial banks such as JPMorgan Chase Bank, N.A., securities or other non-banking affiliates or other JPMC entities. JPMC contact persons may be employees or officers of any of the foregoing entities and the terms “J.P. Morgan”, “JPMorgan”, “JPMorgan Chase” and “Chase” if and as used herein include as applicable all such employees or officers and/or entities irrespective of marketing name(s) used.

Not all products and services are available in all geographic areas. Eligibility for particular products and services is subject to final determination by JPMC and or its affiliates/subsidiaries. This content does not constitute a commitment by any JPMC entity to extend or arrange credit or to provide any other products or services and J.P. Morgan reserves the right to withdraw at any time. All services are subject to applicable laws, regulations, and applicable approvals and notifications.

Notwithstanding anything to the contrary, the statements in this article are not intended to be legally binding. Any products, services, terms or other matters described herein (other than in respect of confidentiality) are subject to the terms of separate legally binding documentation and/or are subject to change without notice. In preparing this article, J.P. Morgan has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources. Neither J.P. Morgan nor any of its directors, officers, employees or agents shall incur any responsibility or liability whatsoever to any other party in respect of the contents of this presentation or any matters referred to in, or discussed as a result of, this article. Nothing in this article is a solicitation by JPMC of any product or service which would be unlawful under applicable laws or regulations. Investments or strategies discussed herein may not be suitable for all investors. This article is not intended to provide, and should not be relied on for, accounting, legal or tax advice or investment recommendations. Please consult your own tax, legal, accounting or investment advisor concerning such matters.

JPMorgan Chase Bank, N.A. Member FDIC.