As organizations navigate through the pandemic, the role of Shared Services Centers (SSCs) – long valued for its ability to save costs – has become increasingly important. SSCs are enabling businesses to focus on reducing finance costs and optimizing working capital in today’s uncertain environment. With the pandemic exposing gaps within existing SSC support models, organizations are faced with the pressing need of accelerating its digitization plans to strengthen finance operations and ensure business continuity.

Based on a survey conducted by J.P. Morgan on global clients who have SSCs, approximately 90 percent of global corporates have centralized at least one finance function into their SSC. The survey also highlighted that 65 percent of clients are focused on finance transformation initiatives and indicated the growing importance of the SSC in their business models.1

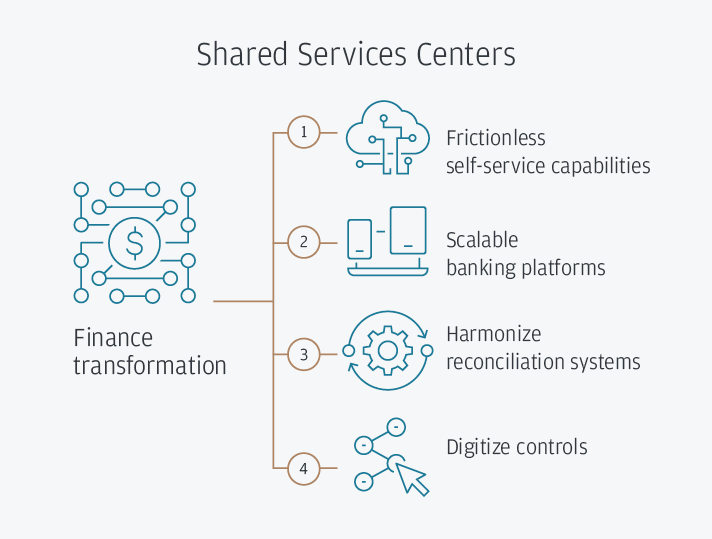

Here are four best practices for digitizing SSCs to reinforce greater efficiencies, control and value in the current environment.

Frictionless self-service capabilities

Scalable banking platforms

Harmonize reconciliation systems

Digitize controls

Here are four best practices for digitizing SSCs to reinforce greater efficiencies, control and value in the current environment.

1. Adopt frictionless self-service capabilities

Amid a crisis, corporates tend to face an influx of payment inquiries as their cash-strapped suppliers seek early payments to manage tight liquidity positions. These additional requests often translate to a significant increase in workload for Accounts Payables (AP) teams already coping with large volumes of planned and urgent payments. Connecting your enterprise resource planning (ERP) systems and supplier portals to your bank through APIs provides your suppliers with a simple, real-time resolution to access payment information. The API connection enables your supplier portal to automatically extract payment confirmations from your bank statements, empowering suppliers with a self-service tool to track payment status directly on their end and freeing up capacity for AP teams to focus on optimization initiatives like analyzing and rationalizing urgent payments that directly impact working capital.

2. Deploy scalable banking platforms

Asia Pacific’s diverse regulatory landscape can sometimes lead to challenges faced by SSCs in the execution of cross-border and statutory payments.

This is especially true in markets that require additional manual documentation to facilitate transactions, resulting in errors involving incorrect or missing fields or details. A strategic banking platform that can digitize the end-to-end execution and issue resolution can help SSC teams immensely.

The use of virtual platforms has grown substantially since the onset of the pandemic, as companies seek rapid solutions to overhaul manual submissions with digital processes. J.P. Morgan’s Virtual Branch has been rolled out in markets like China, India, Indonesia, the Philippines and Vietnam in varying degrees in each country to help clients digitize processes when making cross-border payments, currency conversions or statutory tax payments.

3. Harmonize reconciliation systems

As the order-to-cash process has a direct impact on the working capital needs of an organization, finance practitioners are looking to increase the level of automation in this process. Particularly challenging is the manual nature of reconciliation, also known as the cash application process that requires staff to manually reconcile multiple payments received against their outstanding customer invoices.

Leveraging the right banking infrastructure can help SSC teams reduce manual intervention and speed up processing times by improving automatic invoice matching rates.

J.P. Morgan

Payments

Leveraging the right banking infrastructure can help SSC teams reduce manual intervention and speed up processing times by improving automatic invoice matching rates. For example, J.P. Morgan’s Integrated Receivables platform aggregates fragmented data points across multiple sources and ERP outputs to automatically reconcile receipts with the corresponding invoices. With SSCs now playing a more prominent role in cost optimization, integrating ERP systems into banking platforms can help automate the cash application processes, enabling account receivables (AR) resources to be allocated to activities that provide more value-add, such as resolving disputes, partnering with sales teams to reduce accounts receivables past due in an effort to improve working capital.

4. Digitize controls

Amid movement restrictions during the pandemic, delivering physical documents and securing wet-ink signatures from authorized signatories within the same day for a range of regular banking processes have also become highly challenging. In some cases, bank rationalization initiatives have been deferred, due to heavy reliance on the wet-ink process. Electronic signatures or e-signatures enable clients to digitize the age-old processes of manual bank account opening and other agreements such as physical cash concentrations that require signatories. The simple tool is not only digitally encrypted, but also provides a robust audit trail of all the people who have touched the document, delivering additional layers of information a normal wet-ink signature is unable to accomplish. J.P. Morgan has experienced a significant increase in the adoption of e-signature platforms by its clients across the 26 operating markets around the world. The solution can be just as transformational as it is secure, enabling businesses to continue their rationalization initiatives while complying with due diligence measures. The pandemic may have exposed sensitive gaps within the finance and treasury functions and prompted companies to become agile and adopt workaround measures to reinforce its business continuity plans and emerge from the crisis stronger. Digitizing these key areas of your Shared Services Center can be a fitting response to current challenges.

Please reach out to your J.P. Morgan representative on the availability of SSCs in your market.

References

This material was prepared exclusively for the benefit and internal use of the JPMorgan client to whom it is directly addressed (including such client’s subsidiaries, the “Company”) in order to assist the Company in evaluating a possible transaction(s) and does not carry any right of disclosure to any other party. In preparing this material, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Company or which was otherwise reviewed by us. This material is for discussion purposes only and is incomplete without reference to the other briefings provided by JPMorgan. Neither this material nor any of its contents may be disclosed or used for any other purpose without the prior written consent of JPMorgan.

J.P. Morgan, JPMorgan, JPMorgan Chase and Chase are marketing names for certain businesses of JPMorgan Chase & Co. and its subsidiaries worldwide (collectively, “JPMC”). Products or services may be marketed and/or provided by commercial banks such as JPMorgan Chase Bank, N.A., securities or other non-banking affiliates or other JPMC entities. JPMC contact persons may be employees or officers of any of the foregoing entities and the terms “J.P. Morgan”, “JPMorgan”, “JPMorgan Chase” and “Chase” if and as used herein include as applicable all such employees or officers and/or entities irrespective of marketing name(s) used. Nothing in this material is a solicitation by JPMC of any product or service which would be unlawful under applicable laws or regulations.

Investments or strategies discussed herein may not be suitable for all investors. Neither JPMorgan nor any of its directors, officers, employees or agents shall incur in any responsibility or liability whatsoever to the Company or any other party with respect to the contents of any matters referred herein, or discussed as a result of, this material. This material is not intended to provide, and should not be relied on for, accounting, legal or tax advice or investment recommendations. Please consult your own tax, legal, accounting or investment advisor concerning such matters.

Not all products and services are available in all geographic areas. Eligibility for particular products and services is subject to final determination by JPMC and or its affiliates/subsidiaries. This material does not constitute a commitment by any JPMC entity to extend or arrange credit or to provide any other products or services and JPMorgan reserves the right to withdraw at any time. All services are subject to applicable laws, regulations, and applicable approvals and notifications. The Company should examine the specific restrictions and limitations under the laws of its own jurisdiction that may be applicable to the Company due to its nature or to the products and services referred herein.

Notwithstanding anything to the contrary, the statements in this material are not intended to be legally binding. Any products, services, terms or other matters described herein (other than in respect of confidentiality) are subject to the terms of separate legally binding documentation and/or are subject to change without notice.

Changes to Interbank Offered Rates (IBORs) and other benchmark rates: Certain interest rate benchmarks are, or may in the future become, subject to ongoing international, national and other regulatory guidance, reform and proposals for reform. For more information, please consult: https://www.jpmorgan.com/global/disclosures/interbank_offered_rates.

JPMorgan Chase Bank, N.A. Member FDIC.

JPMorgan Chase Bank, N.A., organized under the laws of U.S.A. with limited liability.