While helping employees save for retirement is important, it’s often outranked by other operational priorities that CFOs must handle. But in a competitive job market, demonstrating that you care about your workers’ financial futures can help you attract and retain talent.

Though you can’t be their personal financial advisor, you can help put your employees on the path to reach a financially secure retirement. Many workers, in fact, are depending on you to help them through the process.

As you assess your 401(k) offerings, use these strategies to help employees get the most out of your retirement plan.

1. Try an automated approach

Many employees can be overwhelmed by the sheer number of investment choices in a 401(k) plan. They may not know how much to invest or which funds to select. One solution: Do it for them.

The majority of plan sponsors now automatically enroll employees in 401(k) plans. By enrolling everyone except those who specifically opt out, you can help overcome employee inertia—one of the biggest hurdles in retirement planning.

You also can help your employees by putting them in target date funds, a diversified mix of investments that automatically adjust over time based on the target retirement date. These funds are managed by a team of experts and can be a good choice for people who don’t have the time or expertise to actively manage their accounts.

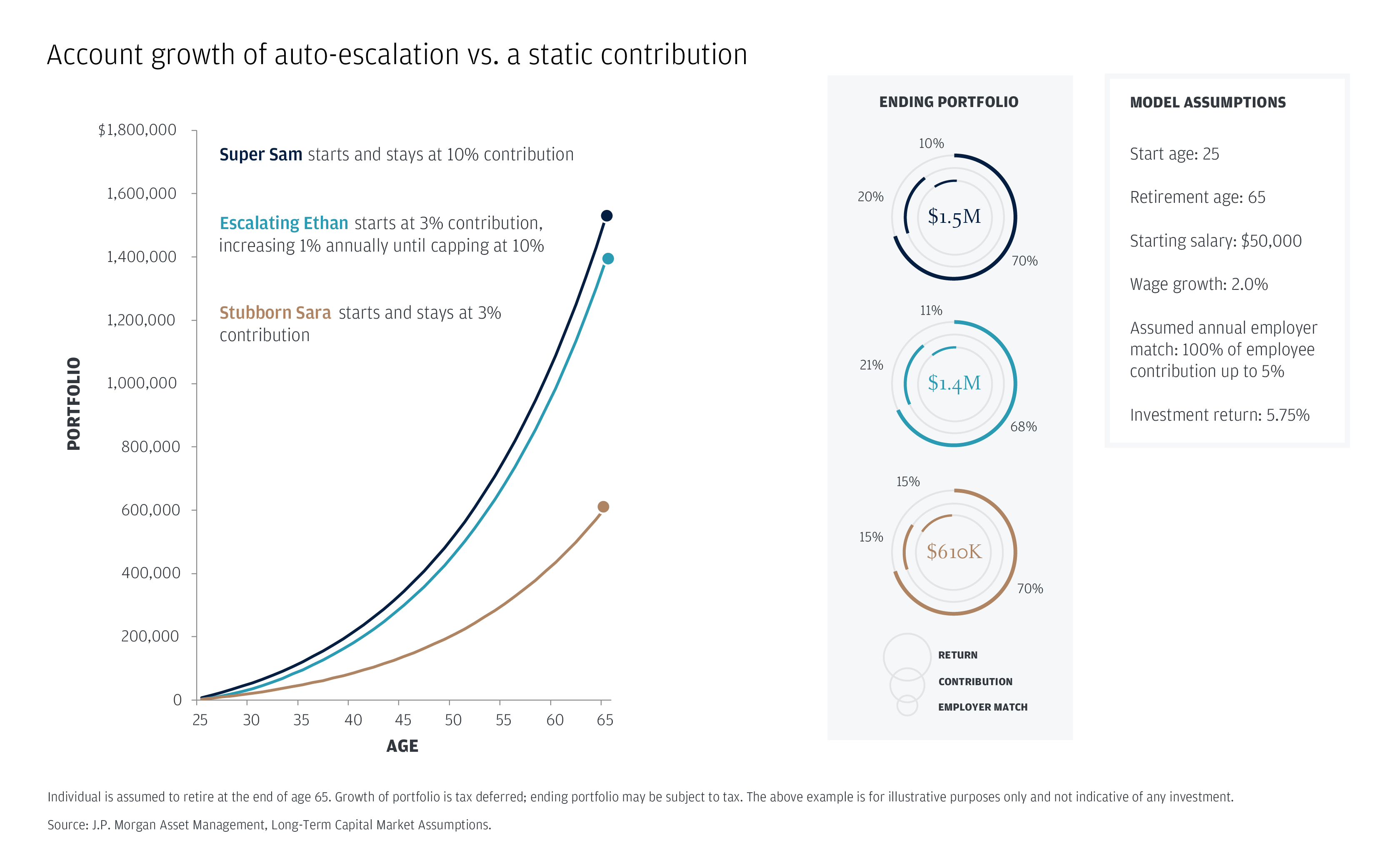

And finally, you should consider automatically increasing employee contributions each year. Many companies use this feature and start their employees at a 3% contribution rate; they then add 1% every year to a pre-set limit. (Ideally, that limit would be between 10%-15%). This allows people to put more money in their 401(k) as their salaries increase over time.

Account growth of auto-escalation vs. a static contribution

Charts showing growth in account value, starting at age 25 and ending at 65

Super Sam starts and stays at 10% contribution

Escalating Ethan starts at 3% contribution, increasing 1% annually until capping at 10%

Stubborn Sara starts and stays at 3% contribution

Ending portfolio

Super Sam: $1.5 million (70% return; 20% contribution; 10% employer match)

Escalating Ethan: $1.4 million (68% return; 21% contribution; 11% employer match)

Stubborn Sara: $610,000 (70% return; 15% contribution; 15% employer match)

Model assumptions

Start age: 25

Retirement age: 65

Starting salary: $50,000

Wage growth: 2.0%

Assumed annual employer match: 100% of employee contribution up to 5%

Investment return: 5.75%

Note: Individual is assumed to retire at the end of age 65. Growth of portfolio is tax deferred; ending portfolio may be subject to tax. The above example is for illustrative purposes only and not indicative of any investment.

Source: J.P. Morgan Asset Management, Long-Term Capital Market Assumptions.

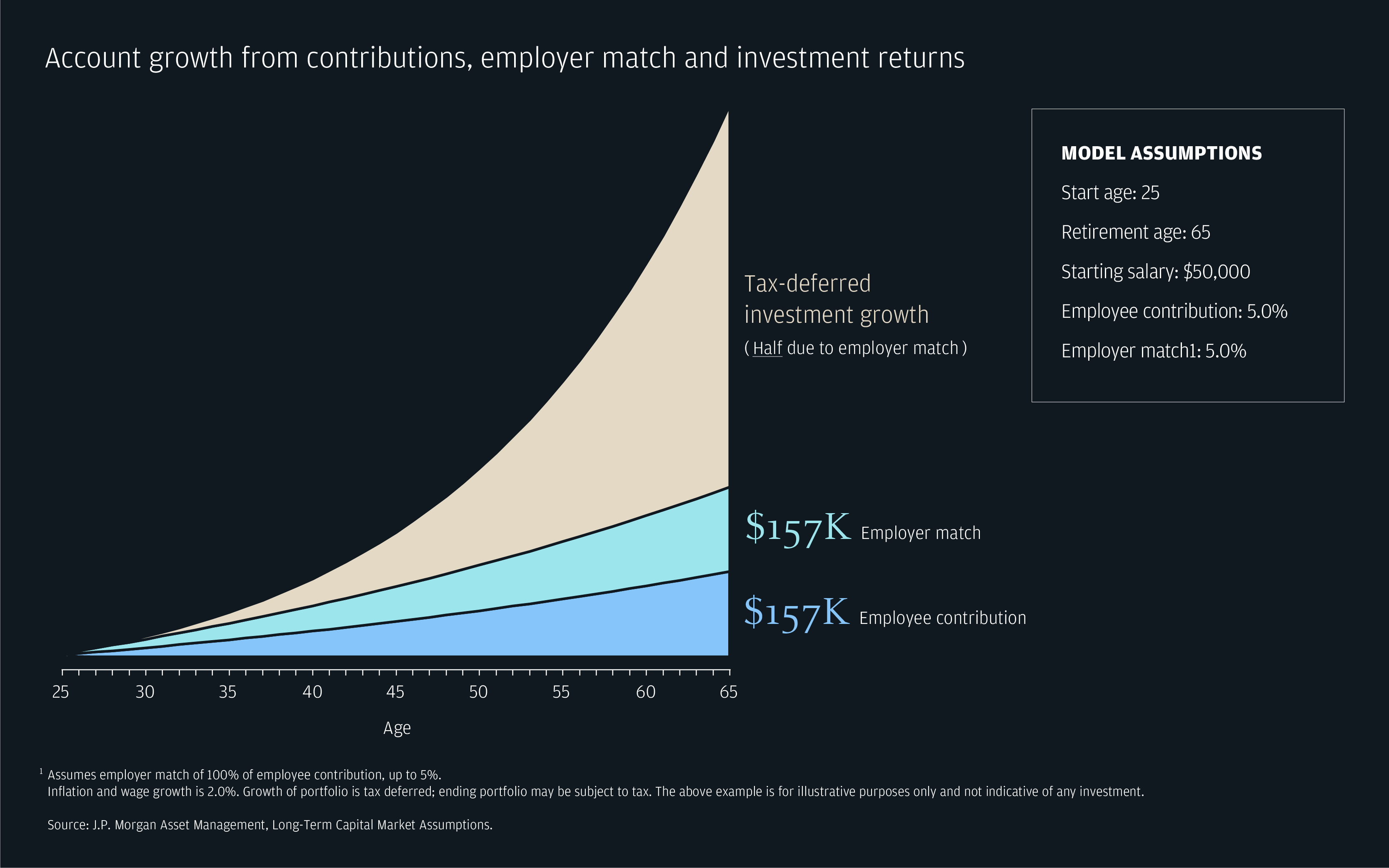

2. Stretch the match

Most companies with a 401(k) plan provide matching contributions. This money is on top of the contributions that employees make on their own. Matches can take several forms, but typically fall into one of these categories:

Partial match: The company uses a formula to match a portion of employee contributions. For example, a plan may match 50 cents on the dollar up to 6% of an employee’s salary.

Full match: These dollar-for-dollar matches are more generous, but they also come with limits. A company, for instance, may make equal matches up to 4% of an employee’s salary.

Stretch match: These require employees to contribute a higher amount to get the full employer match. These matches are typically “graded,” so instead of providing a 100% match up to 4%, the company may match 100% of the first 2% contributed and 50% up to 6% of an employee’s salary. This will produce an employer match of 4%, but an employee needs to contribute 6% to receive it. These plans help instill a strong savings behavior—the more employees contribute, the more matching funds they get.

Some companies opt for a discretionary match, which allows employers to adjust the amount they contribute each year. Regardless of your plan’s rules, if you offer a match make sure your employees are aware of the benefit. They may not realize they’re leaving free money on the table to put toward their retirement.

Account growth from contributions, employer match and investment returns

Chart showing how employer matches can accelerate your 401(k) balance

$157K: Employee contribution

$157K: Employer match

Tax-deferred investment growth: Half due to employer match

Get the free money

Take full advantage of your employer match if available, and consider contributing even more to build your portfolio.

Model assumptions

Start age: 25

Retirement age: 65

Starting salary: $50,000

Employee contribution: 5.0%

Employer match1: 5.0%

Note: 1Assumes employer match of 100% of employee contribution, up to 5%.

Inflation and wage growth is 2.0%. Growth of portfolio is tax deferred; ending portfolio may be subject to tax. The above example is for illustrative purposes only and not indicative of any investment.

Source: J.P. Morgan Asset Management, Long-Term Capital Market Assumptions.

Matching contributions can help a company as well. They can improve employee satisfaction and retention rates, which are key in a tight labor market. They also allow you to claim certain tax benefits. Contact your tax provider or visit the IRS website for more information.

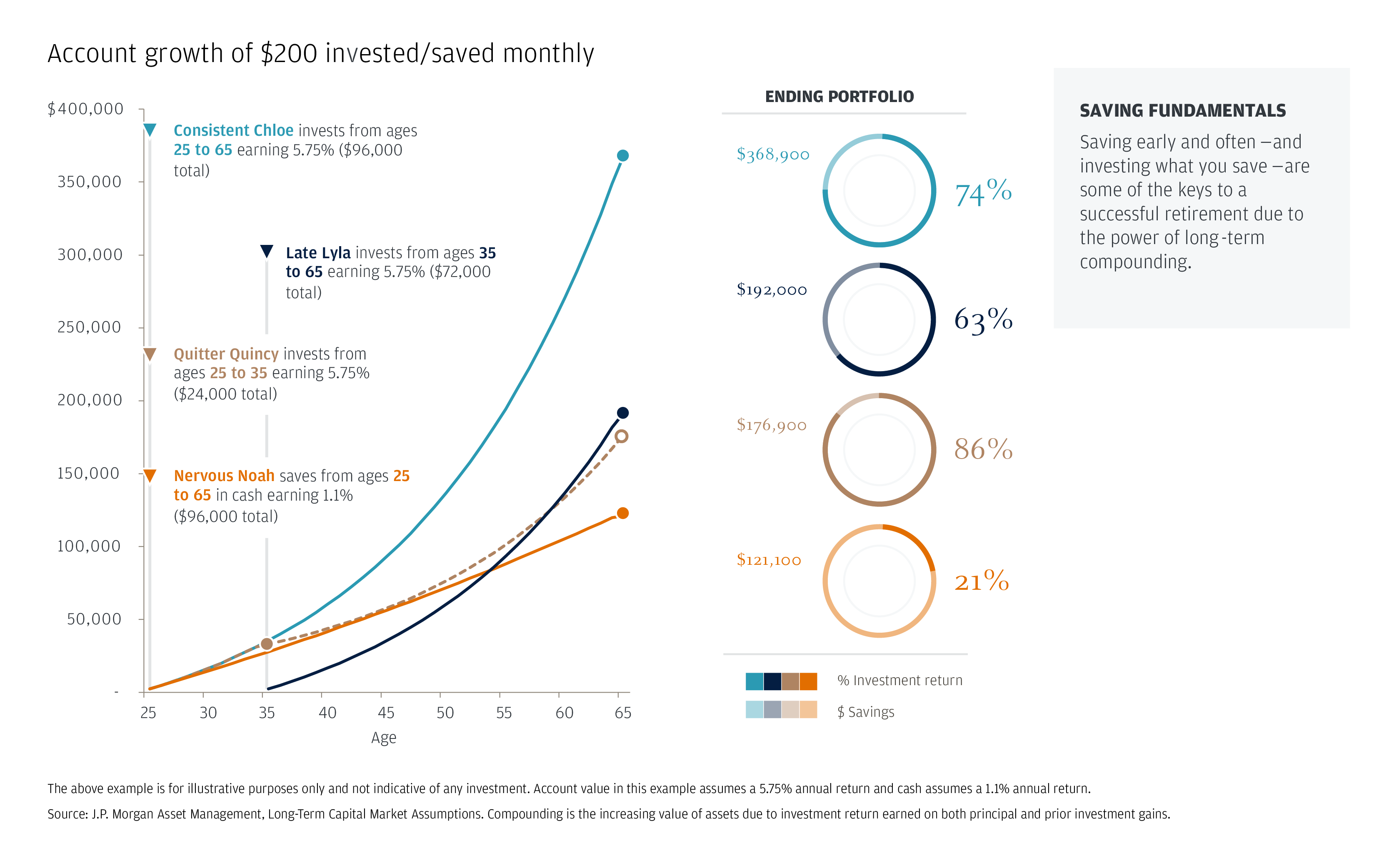

3. Reinforce the benefits of starting early

It may seem like a small thing, but investing early—and consistently over time—can make a huge difference in an employee’s 401(k) balance. Consider the examples in the chart below of four hypothetical people who invest/save $200 a month. (The examples assume an annual return of 5.75% on investments and 1.1% on cash savings.)

- At age 25, Chloe starts investing in a diversified mutual fund in her 401(k) account. She keeps contributing until she turns 65.

Money put in: $96,000

Balance at end: $368,900 - Quincy starts at the same age and invests in the same mutual fund, but he stops contributing after 10 years. Still, his early start lets him reap the benefits of long-time compounding.

Money put in: $24,000

Balance at end: $176,900 - Lyla waits until age 35 to start and keeps investing until she turns 65. Despite investing nearly three times as much money as Quincy, she ends up with only slight more money in her account.

Money put in: $72,000

Balance at end: $192,000 - Noah saves the same amount as Chloe. But he keeps his money in cash rather than investing it in a diversified fund. His conservative approach leaves him with the smallest balance.

Money put in: $96,000

Balance at end: $121,000

Help your employees save for retirement | J.P. Morgan

Account growth of $200 invested/saved monthly

Charts showing growth in account value, depending on when someone starts and stops investing

Consistent Chloe invests from ages 25 to 65 earning 5.75% ($96,000 total)

Late Lyla invests from ages 35 to 65 earning 5.75% ($72,000 total)

Quitter Quincy invests from ages 25 to 35 earning 5.75% ($24,000 total)

Nervous Noah saves from ages 25 to 65 in cash earning 1.1% ($96,000 total)

Ending portfolio

Consistent Chloe: $368,900 (74% investment return; 26% savings)

Late Lyla: $192,000 (63% investment return; 37% savings)

Quitter Quincy: $176,900 (86% investment return; 14% savings)

Nervous Noah: $121,100 (21% investment return; 79% savings)

Saving fundamentals

Saving early and often—and investing what you save—are some of the keys to a successful retirement due to the power of long-term compounding.

Note: The above example is for illustrative purposes only and not indicative of any investment. Account value in this example assumes a 5.75% annual return and cash assumes a 1.1% annual return.

Source: J.P. Morgan Asset Management, Long-Term Capital Market Assumptions. Compounding is the increasing value of assets due to investment return earned on both principal and prior investment gains.

4. Educate, educate, educate

The more you can show your employees how to save for retirement, the better off they’ll be. Here are a few tips to get you—and them—started.

- Make everything easy to understand. Retirement plans can be confusing. So do as much as you can to simplify your 401(k) information. Think about using short videos, FAQs and information sessions to share plan highlights.

- It’s better to show, not tell. Charts and infographics (like the ones above) are every 401(k) manager’s friend. Use them to show employees how their investments could grow over time, which may motivate people to invest in their futures.

- Lean into technology. Between websites and apps, there is a wealth of investing advice out there. Give your employees the resources to make informed decisions about their finances. (J.P. Morgan’s Participant Resource Center is a good place to start.)

7 tips for all investors

These strategies can help investors through challenging markets. Consider sharing the tips with your employees; they’ll appreciate the advice. Learn more >

We’re here to help

JPMorgan Chase’s Commercial Banking experts are here to help you navigate the retirement planning landscape so you can focus on your business. Our comprehensive, full-service retirement plan solution, J.P. Morgan Retirement LinkSM, can help you build quality retirement plans for your employees at lower costs. Schedule a meeting with a Retirement Link specialist to learn more.

JPMorgan Chase Bank, N.A. Member FDIC. Visit jpmorgan.com/cb-disclaimer for disclosures and disclaimers related to this content.