The replacement of fuel vehicles with electric vehicles (EVs) has become a case of not ‘if,’ but ‘when.’

As of the first quarter of 2021, more than 10 percent of cars sold in Europe are electrically chargeable.1 In Norway alone, that figure is 82 percent for the same time period.2 Globally, governments and policymakers are committing to net-zero targets. International carmakers, such as General Motors, Volvo, Volkswagen and Jaguar Land Rover, are transitioning to become all-electric in the next 15 years.

With battery technology developing at a rapid pace and costs coming down, 2023 is now tipped as the year when mass market EVs will reach cost and margin parity with internal combustion vehicles.3

What does this all mean for energy majors?

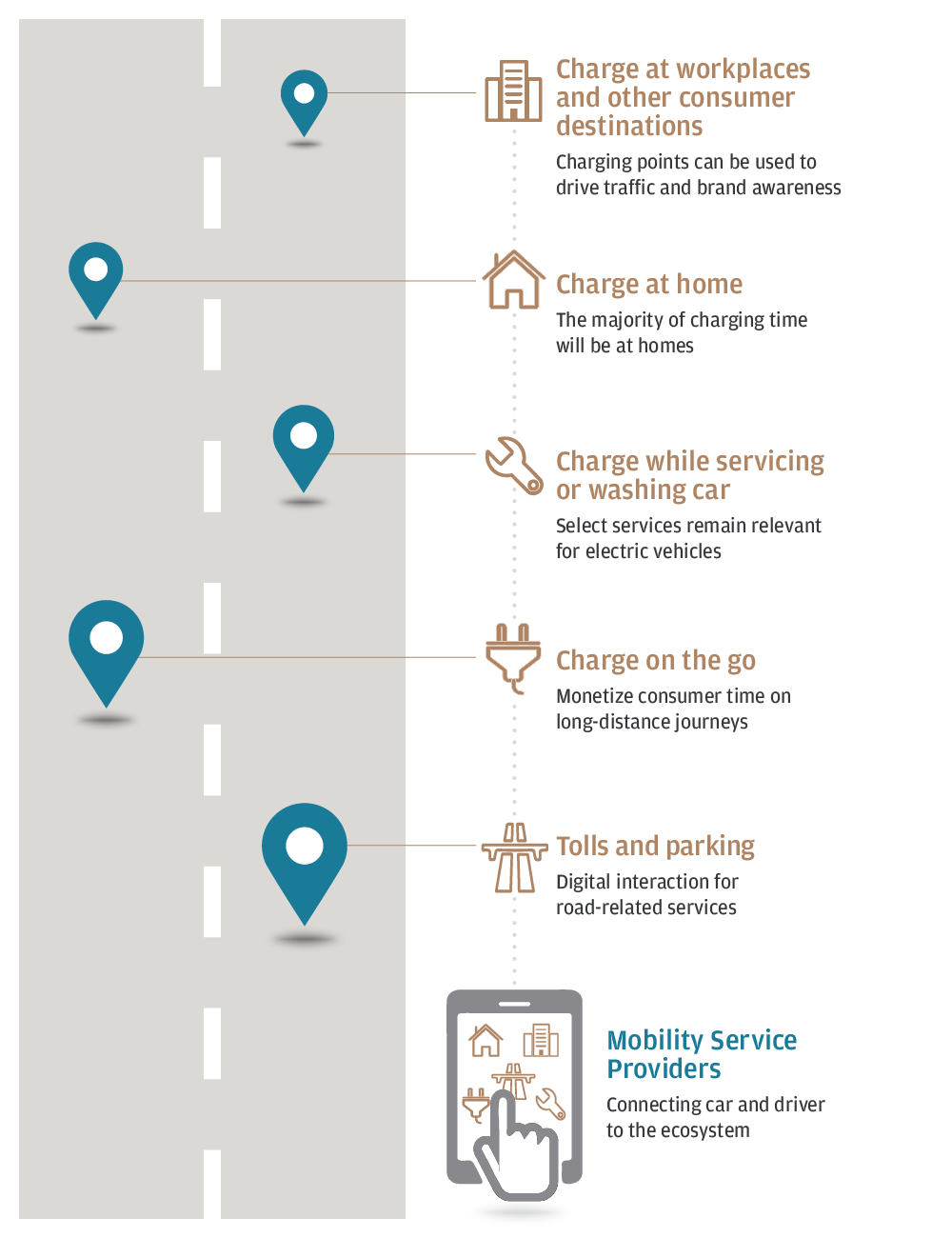

The arrival of the EV tipping point will disrupt the legacy fueling value chain in fundamental ways. In an EV-led world, drivers no longer need a service station when they can charge at home or work. This will result in reduced petroleum sales, but more importantly, in the loss of the intimate relationship with end consumers.

To adapt to this changing environment, treasuries must prepare now

The first movers will gain flexibility in an uncertain marketplace—and a head start on new market entrants.

Here are four strategies to help ensure your business can keep up.