Efforts to advance decarbonization across the globe remain in the early stages—providing an enormous opportunity for green-minded companies to innovate and make a difference. We expect sustainability to remain a priority for business leaders and policymakers in 2024. As we work with the companies navigating this transition, we’re excited to share some of the key renewable energy, sustainable finance and climate tech trends we anticipate for the year ahead.

This first edition of our new quarterly roundup also celebrates four of the companies that closed meaningful transactions in 2023 supporting continued energy transition. In addition, we want to be sure you’ve seen the valuable thought leadership our experts have produced to educate, inspire and advance the energy transition.

Visit our homepage to learn more about our Green Economy Banking team and how we can help support your business. We look forward to working with you.

Eric Cohen

Head of Green Economy Banking, JPMorgan Chase Commercial Banking, North America

Outlook 2024: What trends to watch

We asked leaders across the firm to share what’s top of mind for the green economy in 2024.

Climate technologies

We could see efforts toward the energy transition accelerate again in 2024—and some major new technology projects come online.

- We’re watching to see how much progress technologies such as carbon capture, hydrogen and sustainable aviation fuel will make toward commercialization or large-scale deployment, and whether private capital will be available to support the subsequent raises necessary to support growth plans.

- Green shoots in infrastructure, such as charging networks and hydrogen hubs, could enable widespread adoption of novel technologies.

- Watch for a utility-scale pilot of liquid metal batteries, one of several emerging battery storage technologies supporting the decarbonization of the electricity grid.

- Consumer-oriented businesses may face continued challenges. Sectors that rely on consumer spending, including food tech, ag tech (farming) and mobility, could see valuations slip as they go back to the capital markets.

- Capital expenditure intensity will likely increase year over year as more companies receive access to Department of Energy Loan Programs Office capital for manufacturing and demonstration projects. This could present opportunities for commercial banks to lend alongside non-dilutive financing.

- Venture debt will likely rally as founders look to bolster their balance sheets on the back of capital raises to brace for potentially longer runways, a result of capital constraints.

Project finance and tax equity

In 2024, U.S. tax equity could be the single most important financing market for the energy transition in the world. J.P. Morgan teams will be watching developments around tax credit transfers, technological eligibility and tax equity bridge loans very closely.

- Demand for traditional tax equity from renewable energy projects will likely continue to outstrip supply, creating opportunities for corporates to purchase tax credits either directly from the developers or from tax equity partnerships.

- We’re watching corporates’ participation in the tax credit transfer market. We expect more will participate and the demand for tax credits from investment-grade sponsors will be robust.

- The development of the tax credit transfer market is likely to encourage project finance banks to provide bridge loans without committed tax equity to help ease the funding gap in project development.

- Renewables growth continues to be concentrated in utility-scale solar and battery-storage projects.

- Expect some large-scale energy manufacturing projects, such as battery and solar component production, and green hydrogen projects to reach financial close and start construction.

- We will closely track the formation of green and blue ammonia demand centers in East Asia and Europe—and what it means for production in the U.S., Middle East, India and Australia.

- The convergence of decarbonization and deglobalization trends will likely accelerate the formation of joint ventures and mega projects in the U.S.—not only in renewable energy generation, but also across energy transition manufacturing, carbon capture and hydrogen technologies.

- We’re watching the lender market appetite, which has historically been robust. Given U.S. banking conditions and the volume of capital overseas lenders have already deployed, there’s potential for a tighter senior debt market.

Capital raising and markets

We continue to monitor the evolution of the broader macroeconomic and equity capital markets environment, which provides a relatively challenging backdrop for the sector with a resetting of investor expectations and market valuations.

- Despite the challenges associated with transitioning the world to carbon neutrality, we continue to see lots of opportunities in the space, with a growing volume of private capital pouring in and increasing government support.

- We’re curious how fallen SPACs and smaller public companies will trade in 2024. Time will tell whether they can find an avenue to demonstrate access to capital or if they’ll be acquired by larger strategics.

- We’re projecting a continuation of flight to quality for venture capital equity deployment in 2024, where top-tier portfolio companies could attract the lion’s share of dry powder remaining in VC funds. Reserves are increasing for top portfolio companies.

- IB activity likely will be highly centered around equity premium puzzles as Series B companies and beyond rely less on their board of directors to lead rounds of equity.

- The 2024 election cycle could impact renewable investments. Depending on campaign trail rhetoric and poll results, investors may start to fear potential changes to the Inflation Reduction Act.

ESG and operational sustainability

We’re closely monitoring how public policy may impact low-carbon investment, either directly, like the Basel III Endgame, or indirectly, like the climate disclosure rules expected from the SEC and the European Union’s Corporate Sustainability Due Diligence Directive.

- As concerns grow around greenwashing, ESG litigation and regulatory scrutiny, the quality and transparency of ESG data continues to be a focus area for lenders and their clients.

- There is enhanced focus on sustainability reporting requirements with the introduction of the EU Corporate Sustainability Reporting Directive (CSRD). It took effect in 2023 and will create more reporting requirements for U.S.-based companies with European operations.

- We’re following public sector support in creating industry standards within the voluntary carbon market (VCM) and consolidating protocol and methodology, such as U.S. Department of Energy procurement principles on carbon dioxide removal (CDR).

- Momentum will build toward both mandatory and voluntary emissions reporting, increasing data transparency and helping the firm to better engage with clients and vendors.

- We are closely following initiatives to define transition finance, which should support scaling up financing for the low-carbon energy transition, especially in hard-to-abate sectors.

We’re also increasingly finding ways to use our entire platform to help remove bottlenecks to real economy transition.

- Scaling low-carbon finance for emerging markets and developing economies is a growing focus area. In 2024, we hope to stay close to any developments in that area, particularly with regard to multilateral development bank reform and blended finance, and workforce development—helping to make sure we have enough trained workers to build and maintain the low-carbon infrastructure needed.

- We’re tracking the evolution of the VCM and growth of climate-related technologies, including momentum in all carbon removal pathways, such as DAC, BECCS, BiCRS, ERW and ocean removals. We anticipate an increase in innovative finance structure for CDR projects, both engineered and nature-based.

- We expect increased viability of sustainable aviation fuel (SAF) credits and potentially other book and claim credits for Scope 1 and 3 emissions.

- Technology solutions will continue to advance, improving data availability and resolution and the ability to measure and forecast carbon reduction strategies.

Client highlights

While 2024 holds exciting potential, the future is here for many of our clients, who are already making a difference.

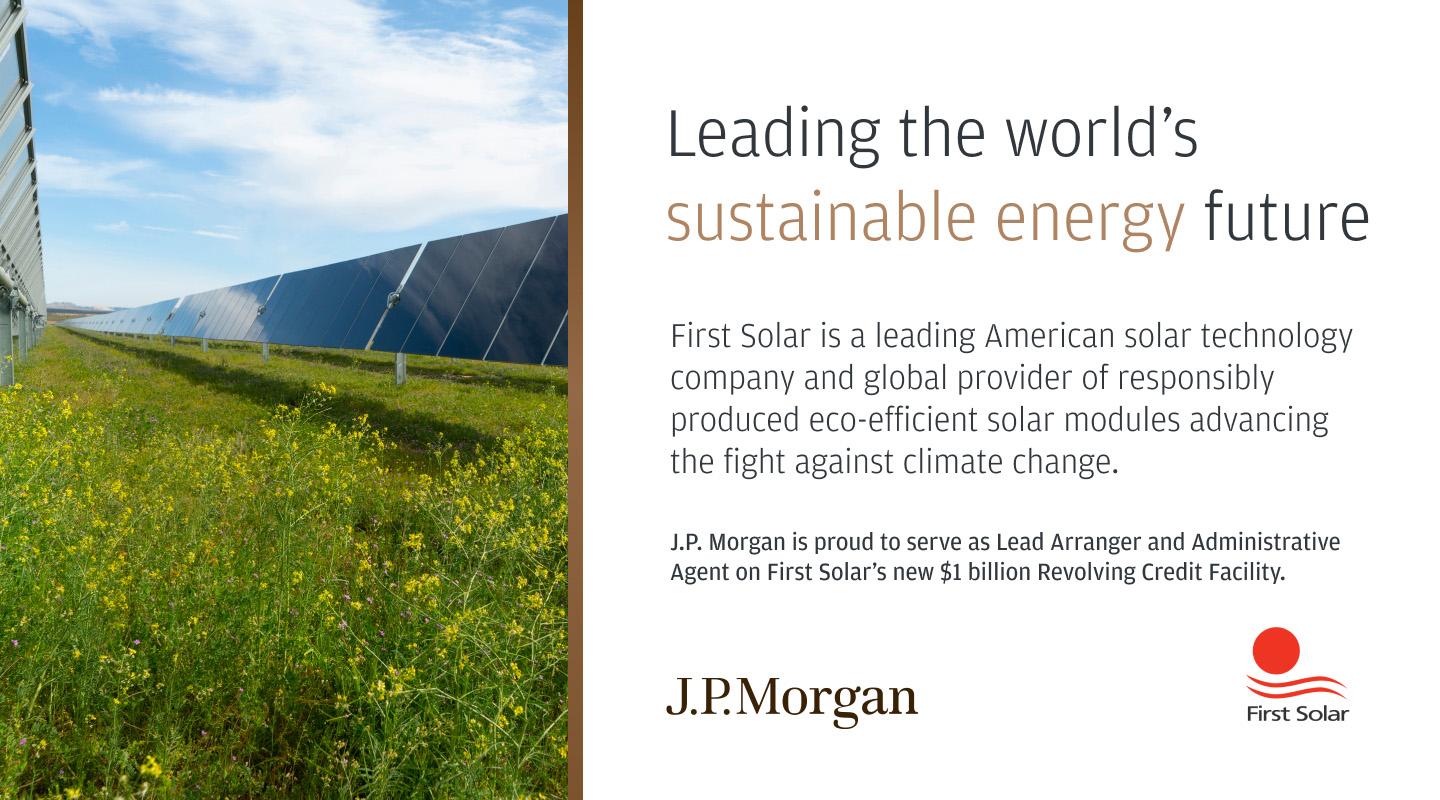

First Solar

J.P. Morgan is proud to support First Solar’s efforts to accelerate the transition to a low-carbon economy and advance long-term clean energy solutions.

Leading the world’s sustainable energy future

First Solar is a leading American solar technology company and global provider of responsibly produced eco-efficient solar modules advancing the fight against climate change.

J.P. Morgan is proud to serve as Lead Arranger and Administrative Agent on First Solar’s new $1 billion Revolving Credit Facility.

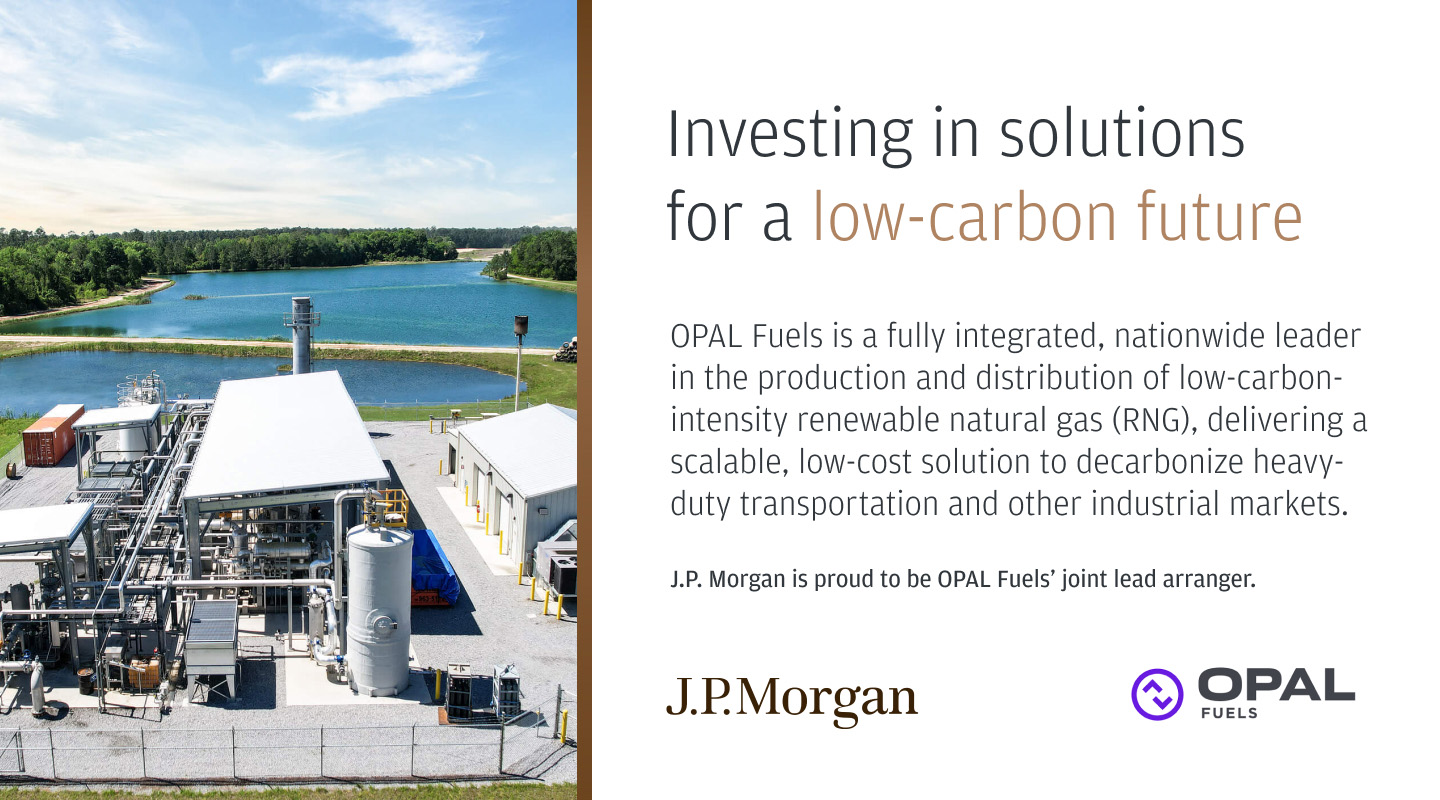

OPAL Fuels

We are proud to support OPAL Fuels’ efforts to advance the clean energy transition in support of renewable energy for transportation, utilities, EV charging, and hydrogen fuel solutions.

Investing in solutions for a low-carbon future

OPAL Fuels is a fully integrated, nationwide leader in the production and distribution of low-carbon-intensity renewable natural gas (RNG), delivering a scalable, low-cost solution to decarbonize heavy-duty transportation and other industrial markets.

J.P. Morgan is proud to be OPAL Fuels’ joint lead arranger.

WAEV

Our team supports WAEV’s mission to develop more sustainable, future-focused solutions and commitment to overcoming barriers in EV adoption.

Energizing forward motion

WAEV is an electric mobility provider dedicated to solving the mobility market’s challenges with nimble innovation and comprehensive solutions.

J.P. Morgan is proud to provide capital to advance decarbonization and grow local economies.

Clēnera

Enlight Renewable Energy Ltd (ENLT), and its U.S. subsidiary Clēnera, are leading the way in developing large, high-performing solar and battery projects across the Western United States. Our team is proud to serve companies that are advancing decarbonization across the globe through innovative business and technology solutions.

Supporting a new era of clean energy

Clēnera is a leading utility-scale solar and storage developer using breakthrough technologies to connect and shape the future of communities.

J.P. Morgan is proud to serve as a joint lead arranger on Clēnera’s 360MWdc Atrisco Solar project financing.

Insights

Scaling sustainability starts with facts, fresh ways of thinking and new frameworks. Explore our latest reports, videos, podcasts and more for valuable perspectives that affect your business.

Reports

- 2023 JPMorgan Chase Climate Report

- 2023 Carbon CompassSM Methodology

- Eye on the Market 13th Annual Energy Paper

- 2022 JPMorgan Chase Environmental Social Governance Report

Videos

Podcasts

- What’s the Deal? | How can sustainable finance make a global impact?

- What’s the Deal? | The power of clean technology: A conversation with Marc Borrett

- What’s the Deal? | U.S. Inflation Reduction Act: Mobilizing for an opportunity of a lifetime

- Research Recap | Why is China’s electric vehicle industry on the rise?

Other resources

- 7 essentials of ESG

- It’s time to solve the energy transition’s project development problem

- Reflecting on our approach to sustainability with JPMorgan Chase’s Jackie Lyons and GreenBiz’s Katie Ryan

- Green financing with Fannie Mae and Freddie Mac

- Building sustainability into our new headquarters

Learn more

Contact the Green Economy Banking team to learn more about the ways we can help your company achieve its goals.

Contributors

- Heather Zichal, Global Head of Sustainability, JPMorgan Chase

- Brian DiMarino, Deputy Director of Global Sustainability, J.P. Morgan Chase

- Rubiao Song, Head of Energy Tax Equity Investments, J.P. Morgan

- Zachary Gross, Managing Director, Climate Tech Investment Banking, J.P. Morgan

- Eric Cohen, Head of Green Economy Banking, JPMorgan Chase Commercial Banking, North America

- Thibaud De Maria, Head of Green Economy Banking, JPMorgan Commercial Banking, EMEA

- Kelly Belcher, Head of Climate Tech, JPMorgan Chase Commercial Banking, North America

- Fuat Savas, Co-Head of Infrastructure Finance and Advisory, J.P. Morgan

- André Abadie, Managing Director, Center for Carbon Transition, J.P. Morgan