Our top market takeaways for June 4, 2021.

Markets in a minute

At the headline index level, this week felt like the “Lazy River” after a prolonged ride on “Splash Mountain.” For the past seven trading days, the S&P 500 hasn’t moved more than +/- 0.40% from its prior day close. That’s given us the longest “boring” streak for the headline index since November 2019, before anyone had even heard of COVID-19. Heading into Friday, the S&P 500 was down -27 basis points on the week (still within 1% of all-time highs, though).

The big-picture narrative didn’t evolve all that much, but there were some interesting details:

- Energy is by far the S&P 500’s best-performing sector on the week and year-to-date (+6.1% since last Friday’s close through Thursday’s; +47.7% on a total return basis since the start of 2021). The sector rose along with oil prices as OPEC+ continued to show production discipline, and demand picked up in real time (last weekend marked the TSA’s busiest period since the start of the pandemic).

- The Markit Services PMI index hit an all-time high because more people are getting vaccinated and want to get their pent-up ya-ya’s out by traveling, eating at restaurants, and so on. Also, Friday’s payrolls report came in below the average estimate, but the addition of 559k jobs (more than half of which came from Leisure & Hospitality) and 0.3% drop in the unemployment rate points towards continued progress. The recovery continues to carry on, and we don’t think the data will influence significant changes to the Fed’s policy stance in either direction.

- Meme stocks are having another moment. Shares of AMC Entertainment climbed nearly +140% over the course of two days. They then fell -18% on Thursday after the company said it would sell over 11 million shares and told investors something along the lines of do you, but our stock price has little to do with our actual business right now.

- President Biden and Congressional Republicans are still trying to find a middle ground on a bipartisan infrastructure deal. It’s still all talk right now, but the president’s latest proposal is to keep the statutory corporate tax rate at 21% and impose a minimum corporate tax rate of 15%. This still means that over 120 S&P 500 companies’ overall tax bills would go up, but it’s a concession nonetheless. If negotiations fall through, Democrats can still pursue spending and tax changes via the budget reconciliation process without the need for GOP support.

Quieter weeks like these offer an opportunity to zoom back out and consider our big investment pictures. Are you holding too much cash? Reticent about putting money to work when the market is at all-time highs? Is your portfolio appropriately diversified?

Spotlight

Investment hygiene checkup

We (are supposed to) go to the dentist twice a year so that we can be scolded or praised for our dental habits. Mechanics recommend getting your car to the garage for maintenance every 30,000 miles. A lot of us are in the habit of a good spring and winter cleaning to refresh our homes as the seasons change. So, this week, we’re here to remind you to check up on your financial hygiene by thinking through whether your financial picture is adhering to three of our tried-and-true investing principles.

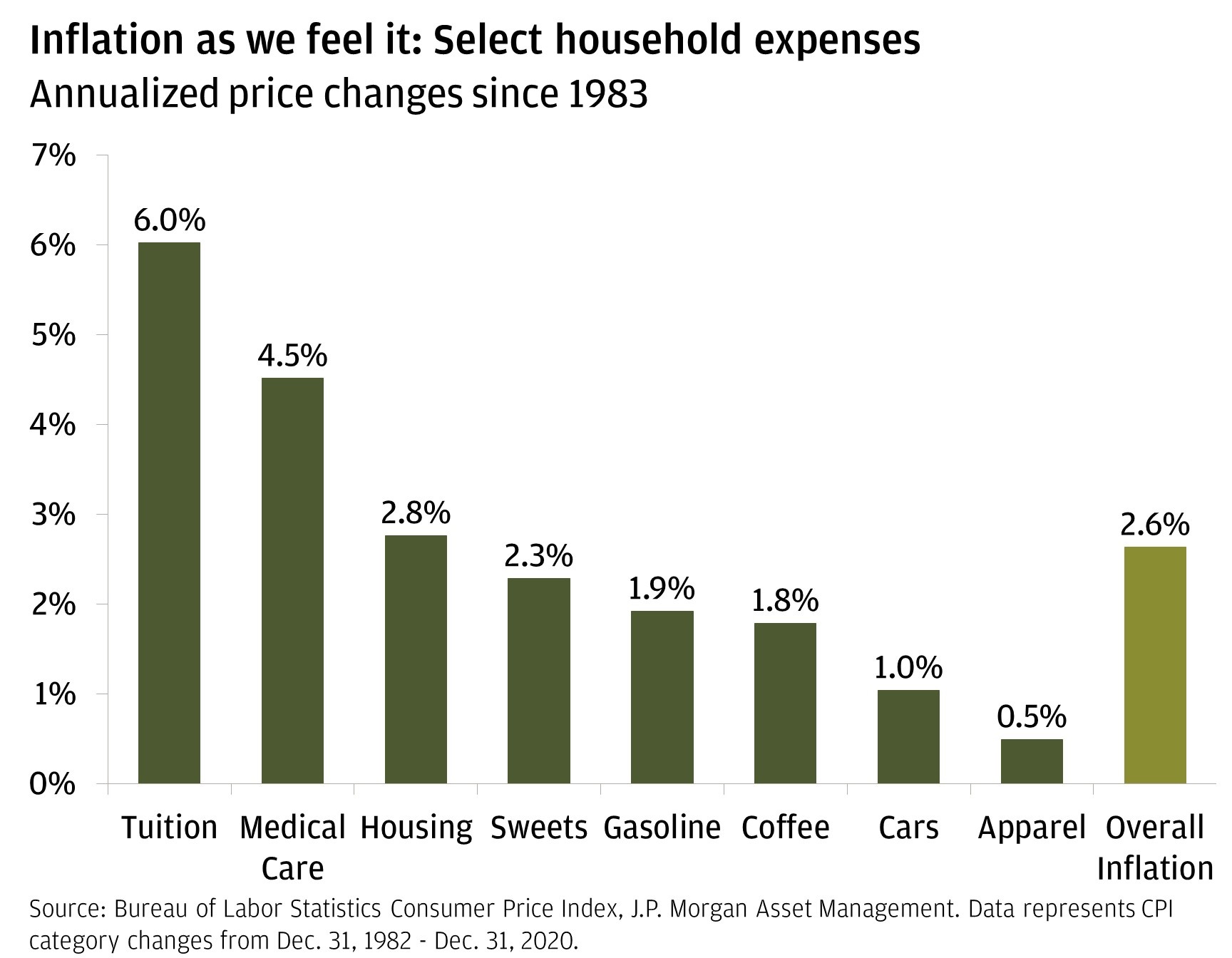

1. The year is 2021, and cheeseburgers don’t cost a quarter anymore. There are a lot of different reasons why we might feel comfortable holding on to cash. But for most of us, the entire point of saving is to use our money for something we will need or want to pay for in the future. That necessitates an approach to managing those savings that gives us the best shot at growing our money at a rate that beats, or at least keeps up with, the pace at which prices rise (A.K.A., inflation).

We’ve been talking about inflation a lot, usually in the context of why we don’t view it as a near-term threat to the Fed’s easy policy stance or the persistence of the market rally. Even our sanguine outlook for price increases acknowledges that they’re still happening, though at different rates in the various areas in which we might spend our money. Consider the chart below:

Sure, a cookie or a cup of coffee may feel like a small expenditure relative to a new car or four years of college education, but all of these items add up. Cash-like instruments earn next to nothing in the present era (short-dated Treasury bills, for example, are yielding under 0.05%), let alone enough to keep up with the Fed’s long-term average 2% overall inflation target. So, are you holding too much cash? If you find that you are, work with your advisor to figure out how you can put it to work according to your goals, ability and willingness to take risk, and your time horizon.

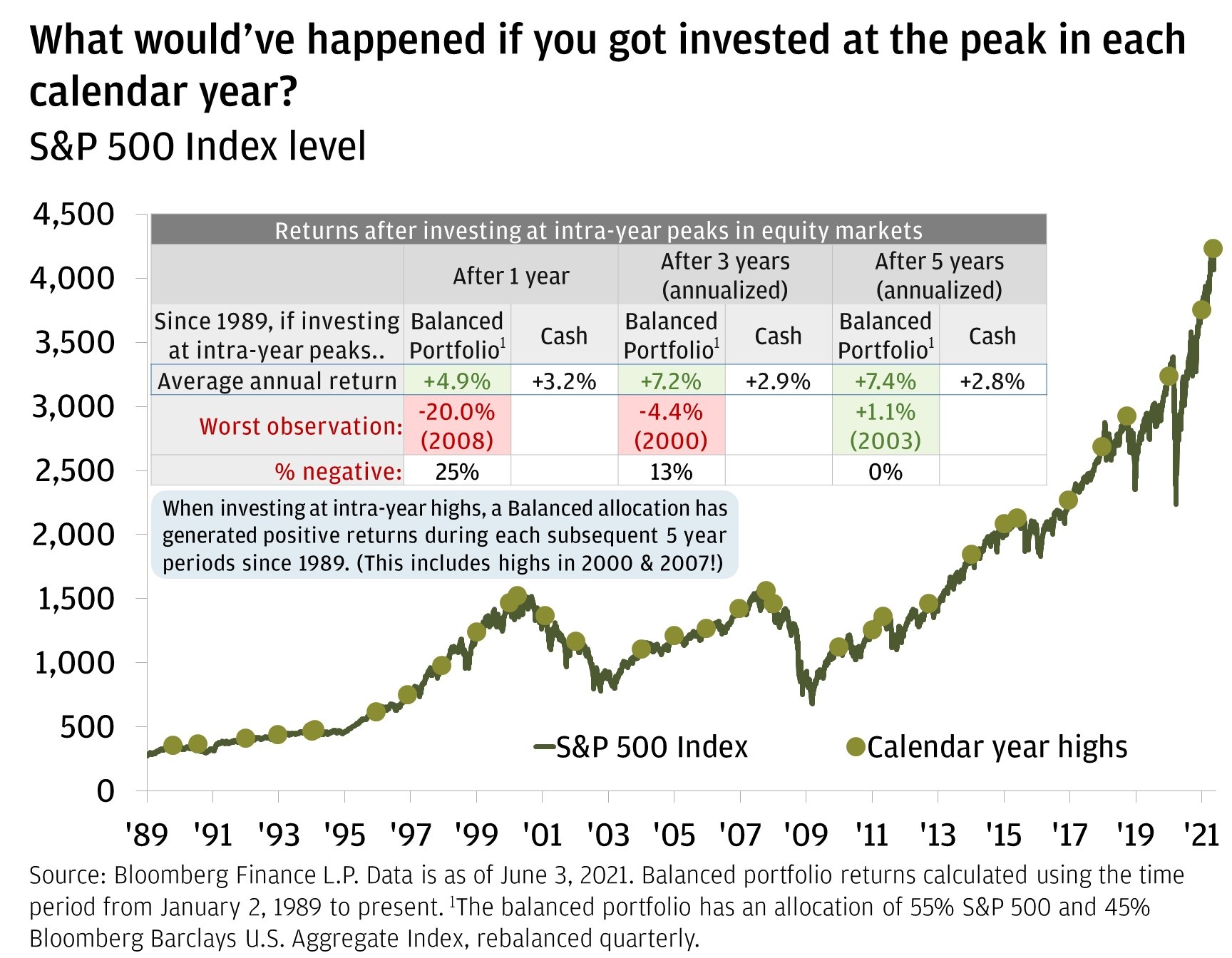

2. Let the good times roll. The S&P 500 has posted 26 new all-time record closes so far this year, compared to a full-year average of 19 since 1990. Even on the days that we haven’t closed at highs, there hasn’t been a single one in 2021 when the market wasn’t within 5% of its most recent all-time record. That’s not to say we won’t see more significant drawdowns at some point this year: 40 years of history show that, on average, the S&P 500 experiences an intra-year decline of -14% but has still mustered positive calendar-year returns 75% of the time. Regardless, for investors considering putting money to work in the U.S. stock market today, you’re doing so near or at highs. The old adage says to “buy low and sell high,” so should you hold off on investing until the market pulls back?

We think not. Time is one of the most powerful allies an investor can have. Let’s assume that when an investor puts money to work, they do so in a diversified manner that reflects their long-term strategic asset allocation. Here, call it 55% stocks and 45% bonds. If you’re investing for the long term (more than five years), the data tells us to feel confident that we can realize positive annualized returns—even if markets are at or near a high.

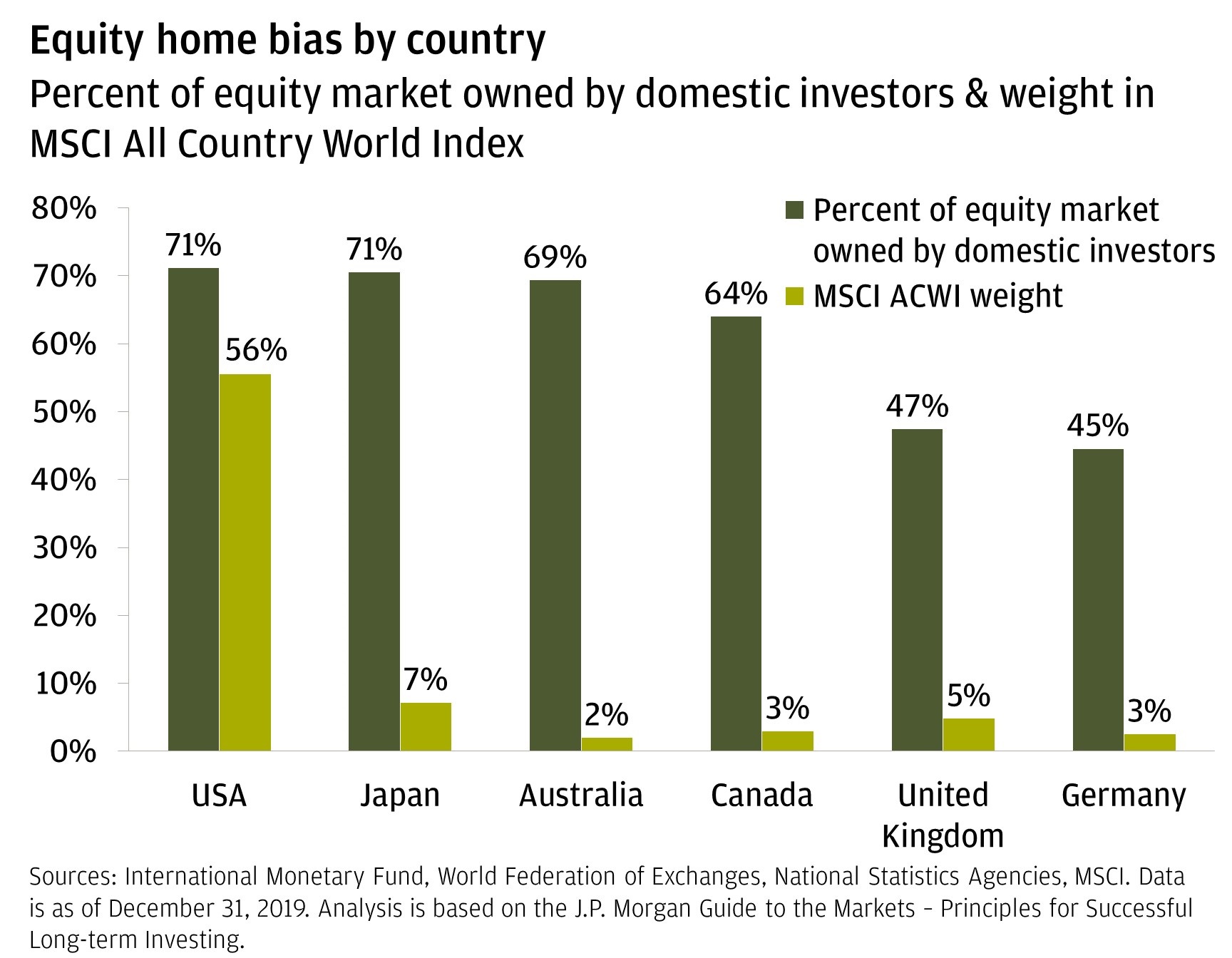

3. You don’t shop in only one aisle of the supermarket, do you? We tend to gravitate toward ideas and things that feel familiar to us (never have I ever bought a different brand of laundry detergent than the one that was always beside my parents’ washing machine), and investors around the world are inclined to act similarly when it comes to constructing their investment portfolios. For example, the U.S. equity market is more than half of the global stock market, yet nearly three-fourths of the entire U.S. equity market is owned by Americans. Brits own nearly 50% of U.K. stocks, but they only account for 5% of the global market. Are you exhibiting home-country bias?

Diversification is crucial, and it’s just as much about having exposure to a mix of geographies as it is about asset classes, sectors and styles. American investors’ preference for U.S. stocks may have been validated by their outperformance over the course of the post-Global Financial Crisis decade, but our outlook today advocates for a more balanced approach to allocating across different regions. For example, we think the tides could be changing favorably for European markets.

When it comes down to it, the various aspects of your personal financial situation should form the basis of your investment approach. The things we want to do with money—our goals—are at the root of the reasons why we invest in the first place. Principles like the ones referenced above offer guidelines as to how we can invest most effectively.

All market and economic data as of June 2021 and sourced from Bloomberg and FactSet unless otherwise stated.

We believe the information contained in this material to be reliable but do not warrant its accuracy or completeness. Opinions, estimates and investment strategies and views expressed in this document constitute our judgment based on current market conditions and are subject to change without notice.

RISK CONSIDERATIONS

- Past performance is not indicative of future results. You may not invest directly in an index.

- The prices and rates of return are indicative, as they may vary over time based on market conditions.

- Additional risk considerations exist for all strategies.

- The information provided herein is not intended as a recommendation of or an offer or solicitation to purchase or sell any investment product or service.

- Opinions expressed herein may differ from the opinions expressed by other areas of J.P. Morgan. This material should not be regarded as investment research or a J.P. Morgan investment research report.

IMPORTANT INFORMATION

This material is for informational purposes only, and may inform you of certain products and services offered by J.P. Morgan’s wealth management businesses, part of JPMorgan Chase & Co. (“JPM”). Please read all Important Information.

- The MSCI China Index captures large- and mid-cap representation across China H shares, B shares, Red chips, P chips and foreign listings (e.g., ADRs). With 459 constituents, the index covers about 85% of this China equity universe. Currently, the index also includes Large Cap A shares represented at 5% of their free float adjusted market capitalization.

- The Standard and Poor’s 500 Index is a capitalization-weighted index of 500 stocks. The index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The index was developed with a base level of 10 for the 1941–43 base period.

- The STOXX Europe 600 Index tracks 600 publicly traded companies based in one of 18 EU countries. The index includes small-cap, medium-cap and large-cap companies. The countries represented in the index are Austria, Belgium, Denmark, Finland, France, Germany, Greece, Holland, Iceland, Ireland, Italy, Luxembourg, Norway, Portugal, Spain, Sweden, Switzerland and the United Kingdom.

This material is for informational purposes only, and may inform you of certain products and services offered by J.P. Morgan’s wealth management businesses, part of JPMorgan Chase & Co. (“JPM”). Please read all Important Information.

GENERAL RISKS & CONSIDERATIONS

Any views, strategies or products discussed in this material may not be appropriate for all individuals and are subject to risks. Investors may get back less than they invested, and past performance is not a reliable indicator of future results. Asset allocation does not guarantee a profit or protect against loss. Nothing in this material should be relied upon in isolation for the purpose of making an investment decision. You are urged to consider carefully whether the services, products, asset classes (e.g., equities, fixed income, alternative investments, commodities, etc.) or strategies discussed are suitable to your needs. You must also consider the objectives, risks, charges, and expenses associated with an investment service, product or strategy prior to making an investment decision. For this and more complete information, including discussion of your goals/situation, contact your J.P. Morgan team.

NON-RELIANCE

Certain information contained in this material is believed to be reliable; however, JPM does not represent or warrant its accuracy, reliability or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. No representation or warranty should be made with regard to any computations, graphs, tables, diagrams or commentary in this material, which are provided for illustration/reference purposes only. The views, opinions, estimates and strategies expressed in this material constitute our judgment based on current market conditions and are subject to change without notice. JPM assumes no duty to update any information in this material in the event that such information changes. Views, opinions, estimates and strategies expressed herein may differ from those expressed by other areas of JPM, views expressed for other purposes or in other contexts, and this material should not be regarded as a research report. Any projected results and risks are based solely on hypothetical examples cited, and actual results and risks will vary depending on specific circumstances. Forward-looking statements should not be considered as guarantees or predictions of future events.

Nothing in this document shall be construed as giving rise to any duty of care owed to, or advisory relationship with, you or any third party. Nothing in this document shall be regarded as an offer, solicitation, recommendation or advice (whether financial, accounting, legal, tax or other) given by J.P. Morgan and/or its officers or employees, irrespective of whether or not such communication was given at your request. J.P. Morgan and its affiliates and employees do not provide tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any financial transactions.

IMPORTANT INFORMATION ABOUT YOUR INVESTMENTS AND POTENTIAL CONFLICTS OF INTEREST

Conflicts of interest will arise whenever JPMorgan Chase Bank, N.A. or any of its affiliates (together, “J.P. Morgan”) have an actual or perceived economic or other incentive in its management of our clients’ portfolios to act in a way that benefits J.P. Morgan. Conflicts will result, for example (to the extent the following activities are permitted in your account): (1) when J.P. Morgan invests in an investment product, such as a mutual fund, structured product, separately managed account or hedge fund issued or managed by JPMorgan Chase Bank, N.A. or an affiliate, such as J.P. Morgan Investment Management Inc.; (2) when a J.P. Morgan entity obtains services, including trade execution and trade clearing, from an affiliate; (3) when J.P. Morgan receives payment as a result of purchasing an investment product for a client’s account; or (4) when J.P. Morgan receives payment for providing services (including shareholder servicing, recordkeeping or custody) with respect to investment products purchased for a client’s portfolio. Other conflicts will result because of relationships that J.P. Morgan has with other clients or when J.P. Morgan acts for its own account.

Investment strategies are selected from both J.P. Morgan and third-party asset managers and are subject to a review process by our manager research teams. From this pool of strategies, our portfolio construction teams select those strategies we believe fit our asset allocation goals and forward-looking views in order to meet the portfolio’s investment objective.

As a general matter, we prefer J.P. Morgan managed strategies. We expect the proportion of J.P. Morgan managed strategies will be high (in fact, up to 100 percent) in strategies such as cash and high-quality fixed income, subject to applicable law and any account-specific considerations.

While our internally managed strategies generally align well with our forward-looking views, and we are familiar with the investment processes as well as the risk and compliance philosophy of the firm, it is important to note thatJ.P. Morgan receives more overall fees when internally managed strategies are included. We offer the option of choosing to exclude J.P. Morgan managed strategies (other than cash and liquidity products) in certain portfolios.

The Six Circles Funds are U.S.-registered mutual funds managed by J.P. Morgan and sub-advised by third parties. Although considered internally managed strategies, JPMC does not retain a fee for fund management or other fund services.

LEGAL ENTITY, BRAND & REGULATORY INFORMATION

In the United States, bank deposit accounts and related services, such as checking, savings and bank lending, are offered by JPMorgan Chase Bank, N.A. Member FDIC.

JPMorgan Chase Bank, N.A. and its affiliates (collectively “JPMCB”) offer investment products, which may include bank-managed investment accounts and custody, as part of its trust and fiduciary services. Other investment products and services, such as brokerage and advisory accounts, are offered through J.P. Morgan Securities LLC (“JPMS”), a member of FINRA and SIPC. Annuities are made available through Chase Insurance Agency, Inc. (CIA), a licensed insurance agency, doing business as Chase Insurance Agency Services, Inc. in Florida. JPMCB, JPMS and CIA are affiliated companies under the common control of JPMorgan Chase & Co. Products not available in all states.

In Luxembourg, this material is issued by J.P. Morgan Bank Luxembourg S.A (JPMBL), with registered office at European Bank and Business Centre, 6 route de Treves, L-2633, Senningerberg, Luxembourg. R.C.S Luxembourg B10.958. Authorized and regulated by Commission de Surveillance du Secteur Financier (CSSF) and jointly supervised by the European Central Bank (ECB) and the CSSF. J.P. Morgan Bank Luxembourg S.A. is authorized as a credit institution in accordance with the Law of 5th April 1993. In the United Kingdom, this material is issued by J.P. Morgan Bank Luxembourg S.A., London Branch. Prior to Brexit (Brexit meaning that the United Kingdom leaves the European Union under Article 50 of the Treaty on European Union, or, if later, loses its ability to passport financial services between the UK and the remainder of the EEA), J.P. Morgan Bank Luxembourg S.A., London Branch is subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority. Details about the extent of our regulation by the Financial Conduct Authority and the Prudential Regulation Authority are available from us on request. In the event of Brexit, in the UK, J.P. Morgan Bank Luxembourg S.A., London Branch is authorized by the Prudential Regulation Authority, subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. Details about the extent of our regulation by the Prudential Regulation Authority are available from us on request. In Spain, this material is distributed by J.P. Morgan Bank Luxembourg S.A., Sucursal en España, with registered office at Paseo de la Castellana, 31, 28046 Madrid, Spain. J.P. Morgan Bank Luxembourg S.A., Sucursal en España is registered under number 1516 within the administrative registry of the Bank of Spain and supervised by the Spanish Securities Market Commission (CNMV). In Germany, this material is distributed by J.P. Morgan Bank Luxembourg S.A., Frankfurt Branch, registered office at Taunustor 1 (TaunusTurm), 60310 Frankfurt, Germany, jointly supervised by the Commission de Surveillance du Secteur Financier (CSSF) and the European Central Bank (ECB), and in certain areas also supervised by the Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin). In Italy, this material is distributed byJ.P. Morgan Bank Luxembourg S.A., Milan Branch, registered office at Via Cantena Adalberto 4, Milan 20121, Italy and regulated by Bank of Italy and the Commissione Nazionale per le Società e la Borsa (CONSOB). In addition, this material may be distributed by JPMorgan Chase Bank, N.A. (“JPMCB”), Paris branch, which is regulated by the French banking authorities Autorité de Contrôle Prudentiel et de Résolution and Autorité des Marchés Financiers or by J.P. Morgan (Suisse) SA, which is regulated in Switzerland by the Swiss Financial Market Supervisory Authority (FINMA).

In Hong Kong, this material is distributed by JPMCB, Hong Kong branch. JPMCB, Hong Kong branch is regulated by the Hong Kong Monetary Authority and the Securities and Futures Commission of Hong Kong. In Hong Kong, we will cease to use your personal data for our marketing purposes without charge if you so request. In Singapore, this material is distributed by JPMCB, Singapore branch. JPMCB, Singapore branch is regulated by the Monetary Authority of Singapore. Dealing and advisory services and discretionary investment management services are provided to you by JPMCB, Hong Kong/Singapore branch (as notified to you). Banking and custody services are provided to you by JPMCB Singapore Branch. The contents of this document have not been reviewed by any regulatory authority in Hong Kong, Singapore or any other jurisdictions. You are advised to exercise caution in relation to this document. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice. For materials which constitute product advertisement under the Securities and Futures Act and the Financial Advisers Act, this advertisement has not been reviewed by the Monetary Authority of Singapore. JPMorgan Chase Bank, N.A., a national banking association chartered under the laws of the United States, and as a body corporate, its shareholder’s liability is limited.

JPMorgan Chase Bank, N.A. (JPMCBNA) (ABN 43 074 112 011/AFS Licence No: 238367) is regulated by the Australian Securities and Investment Commission and the Australian Prudential Regulation Authority. Material provided by JPMCBNA in Australia is to “wholesale clients” only. For the purposes of this paragraph the term “wholesale client” has the meaning given in section 761G of the Corporations Act 2001 (Cth). Please inform us if you are not a Wholesale Client now or if you cease to be a Wholesale Client at any time in the future.

JPMS is a registered foreign company (overseas) (ARBN 109293610) incorporated in Delaware, U.S.A. Under Australian financial services licensing requirements, carrying on a financial services business in Australia requires a financial service provider, such as J.P. Morgan Securities LLC (JPMS), to hold an Australian Financial Services Licence (AFSL), unless an exemption applies. JPMS is exempt from the requirement to hold an AFSL under the Corporations Act 2001 (Cth) (Act) in respect of financial services it provides to you, and is regulated by the SEC, FINRA and CFTC under U.S. laws, which differ from Australian laws. Material provided by JPMS in Australia is to “wholesale clients” only. The information provided in this material is not intended to be, and must not be, distributed or passed on, directly or indirectly, to any other class of persons in Australia. For the purposes of this paragraph the term “wholesale client” has the meaning given in section 761G of the Act. Please inform us immediately if you are not a Wholesale Client now or if you cease to be a Wholesale Client at any time in the future.

This material has not been prepared specifically for Australian investors. It:

- May contain references to dollar amounts which are not Australian dollars;

- May contain financial information which is not prepared in accordance with Australian law or practices;

- May not address risks associated with investment in foreign currency denominated investments; and

- Does not address Australian tax issues.

With respect to countries in Latin America, the distribution of this material may be restricted in certain jurisdictions. We may offer and/or sell to you securities or other financial instruments which may not be registered under, and are not the subject of a public offering under, the securities or other financial regulatory laws of your home country. Such securities or instruments are offered and/or sold to you on a private basis only. Any communication by us to you regarding such securities or instruments, including without limitation the delivery of a prospectus, term sheet or other offering document, is not intended by us as an offer to sell or a solicitation of an offer to buy any securities or instruments in any jurisdiction in which such an offer or a solicitation is unlawful. Furthermore, such securities or instruments may be subject to certain regulatory and/or contractual restrictions on subsequent transfer by you, and you are solely responsible for ascertaining and complying with such restrictions. To the extent this content makes reference to a fund, the Fund may not be publicly offered in any Latin American country, without previous registration of such fund’s securities in compliance with the laws of the corresponding jurisdiction. Public offering of any security, including the shares of the Fund, without previous registration at Brazilian Securities and Exchange Commission–CVM is completely prohibited. Some products or services contained in the materials might not be currently provided by the Brazilian and Mexican platforms.

References to “J.P. Morgan” are to JPM, its subsidiaries and affiliates worldwide.“J.P. Morgan Private Bank” is the brand name for the private banking business conducted by JPM. This material is intended for your personal use and should not be circulated to or used by any other person, or duplicated for non-personal use, without our permission. If you have any questions or no longer wish to receive these communications, please contact your J.P. Morgan team.

Check the background of our firm and investment professionals on FINRA's BrokerCheck

To learn more about J. P. Morgan Wealth Management’s investment business, including our accounts, products and services, as well as our relationship with you, please review our J.P. Morgan Securities LLC Form CRS and Guide to Investment Services and Brokerage Products.

This website is for informational purposes only, and not an offer, recommendation or solicitation of any product, strategy service or transaction. Any views, strategies or products discussed on this site may not be appropriate or suitable for all individuals and are subject to risks. Prior to making any investment or financial decisions, an investor should seek individualized advice from a personal financial, legal, tax and other professional advisors that take into account all of the particular facts and circumstances of an investor's own situation.

This website may provide information about the brokerage and investment advisory services provided by J.P. Morgan Securities LLC ("JPMS"). When JPMS acts as a broker-dealer, a client's relationship with us and our duties to the client will be different in some important ways than a client's relationship with us and our duties to the client when we are acting as an investment advisor. A client should carefully read the agreements and disclosures received (including our Form ADV disclosure brochure, if and when applicable) in connection with our provision of services for important information about the capacity in which we will be acting.

INVESTMENT AND INSURANCE PRODUCTS ARE:

• NOT FDIC INSURED • NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY • NOT A DEPOSIT OR OTHER OBLIGATION OF, OR GUARANTEED BY, JPMORGAN CHASE BANK, N.A. OR ANY OF ITS AFFILIATES • SUBJECT TO INVESTMENT RISKS, INCLUDING POSSIBLE LOSS OF THE PRINCIPAL AMOUNT INVESTED

J.P. Morgan Wealth Management is a business of JPMorgan Chase & Co., which offers investment products and services through J.P. Morgan Securities LLC (JPMS), a registered broker-dealer and investment adviser, member FINRA and SIPC Insurance products are made available through Chase Insurance Agency, Inc. (CIA), a licensed insurance agency, doing business as Chase Insurance Agency Services, Inc. in Florida. Certain custody and other services are provided by JPMorgan Chase Bank, N.A. (JPMCB). JPMS, CIA and JPMCB are affiliated companies under the common control of JPMorgan Chase & Co. Products not available in all states.

Please read additional Important Information in conjunction with these pages.

You're now leaving J.P. Morgan

J.P. Morgan’s website and/or mobile terms, privacy and security policies don’t apply to the site or app you're about to visit. Please review its terms, privacy and security policies to see how they apply to you. J.P. Morgan isn’t responsible for (and doesn’t provide) any products, services or content at this third-party site or app, except for products and services that explicitly carry the J.P. Morgan name.