E-commerce has experienced staggering growth in recent years. While traditional brick-and-mortar businesses still account for nearly 90 percent of global retail sales in 2018, online sales have soared, growing 20 percent annually since 2017 and expected to double by 2021, according to a report by Cantor Fitzgerald1. Companies of all sizes are under increased pressure to build their online presence quickly to keep up with competition, increase sales or maintain market share.

E-commerce presents treasury with an opportunity to play a larger role in supporting the organization’s growth, but the changing landscape means practitioners need a fresh approach to treasury management. In this article, we examine the key challenges that treasurers may face as they embark on the e-commerce journey, and how they can position for success.

From offline to online:

5 key challenges for treasury

1. Higher velocity and volume of sales

While physical stores are typically confined to buyers in a particular geography, e-commerce has allowed businesses to expand their pool of customers, sometimes as wide as across the globe. Thanks to internet and smartphone penetration, a purchase is often a mere click away via a website or mobile app, significantly changing the dynamics of traditional commerce.

The shift towards direct-to-consumer models could pose challenges for corporate treasurers that have long been accustomed to managing cash, funding and FX from traditional flows. The fast pace and high volume of sales can disrupt regular business cycles, financial forecasts as well as standard processes in ordering, receiving, recording and reporting of purchases. For example, online Black Friday sales in the U.S. and China’s Singles Day shopping event have resulted in cases where wrong addresses or rerouting of orders can create a backlog of outstanding transactions, disputes, cancellations or refunds, and in turn create major reconciliation issues for finance teams.

2. New payment methods and currencies

It’s only a matter of time before traditional payment methods like cash, credit cards, cheques and wires give way to newer, alternate formats like e-wallets that offer convenience to users. To improve buyer experience, more online businesses are also offering customers the ability to make payments in their preferred currencies.

Treasurers will need to be prepared to manage local nuances, especially in Asia where regulations, tax laws and settlement times can differ vastly. Strict license and documentation requirements for cross-border payments in certain markets can also create added complexity. In addition, the acceptance of payments in a wider range of currencies could expose businesses to new FX risks.

3. Need for real time

The 24/7 nature of e-commerce means sales records are no longer updated just once at end of the business day but in real time, as and when transactions occur. Customer information will also need to be synced across all systems as the purchase is being made, which can be complex if a company has multiple banking partners with separate payment platforms and reporting formats.

For treasurers, this means a need to replace manual, excel-based workflows with centralized, automated and straight-through alternatives that facilitate quicker processing and tracking of transactions. A well-integrated system with a single customer database that connects treasury and accounting systems with those of marketing, product management, logistics and customer relations can result in smoother workflows, eliminating the need to manually track information.

4. Active to passive liquidity management

With real-time payments enabling settlements to take place around the clock, treasurers can no longer rely on manual processes to manage their liquidity and FX.

Dynamic liquidity and investments solutions that facilitate automatic cash concentration across subsidiaries and regions and invest surplus cash can help optimize internal liquidity and yields even during after-hours. Companies receiving cross-border payments across multiple currencies can also tap into innovative FX solutions to ensure currency exposures are managed in real time.

5. Superior customer experience

With the customer experience moving to online channels, companies are increasingly looking to differentiate themselves through enhanced user experience. A seamless payment process that provides customers the ability to pay in their preferred currencies and payment methods will create a better buyer experience and help to reduce the number of customers abandoning their e-shopping carts.

Firms are also tapping into an omni-channel approach – where customers can engage via a range of communication channels including in-person, phone, web chat, email and social media. This not only requires an integrated approach around communications, but also a unified system that connects marketing and sales processes with the backend payment infrastructure to avoid the finance and logistics teams manually tracking large volumes of transactions in order to reconcile data.

Supporting your global e-commerce needs

A successful e-commerce strategy requires the integration of three key elements – system, process and people – which would enable treasurers to balance an organization’s speed to market, financial efficiency, long-term sustainability and growth.

3 Key Pillars for a Successful E-commerce Strategy

-

System

- Full integration between ERP webstore logistics and back end systems

- Up-to-date ERP data on :

- Prices

- Discounts

- Customers

- Products

- Real-time data & analytics

- No downtime

- Multiple language support

-

Process

- 24x7 automated processing/reconciliation

- Scalability

- Standardization & centralization

- Strong control environment

- Leverage artificial intelligence, machine learning & robotics

-

People

- Appoint an e-commmerce manager

- Clear communication on e-commmerce strategy & objectives

- Adopt a customer-centric culture

- Cybersecurity awareness & training

Leveraging a robust, global payment platform with the ability to provide competitive FX rates, execute payments and collections online can be a key factor for success. When it comes to collections, a good starting point is to focus on the most crucial markets. As a business expands its e-commerce offerings to overseas markets, treasurers should look at reducing expenses associated with cross-border transactions and establishing local bank accounts that can offer a broad range of payment types at reduced costs.

J.P. Morgan offers a range of e-commerce solutions that brings together the strength and security of an established bank with a comprehensive, global payments network to meet the evolving requirements of the e-commerce industry. From simplifying payments via e-wallets, to instant FX pricing in customer’s preferred currencies, and enhanced reconciliation via virtual accounts, clients can leverage J.P. Morgan’s extensive pay-in and pay-out network to unlock e-commerce opportunities and reduce barriers in local markets.

By developing alliances with local fintechs, J.P. Morgan aims to offer a complete set of capabilities to help clients manage their large volume of payments and support clients’ present and future needs as they grow their e-commerce business.

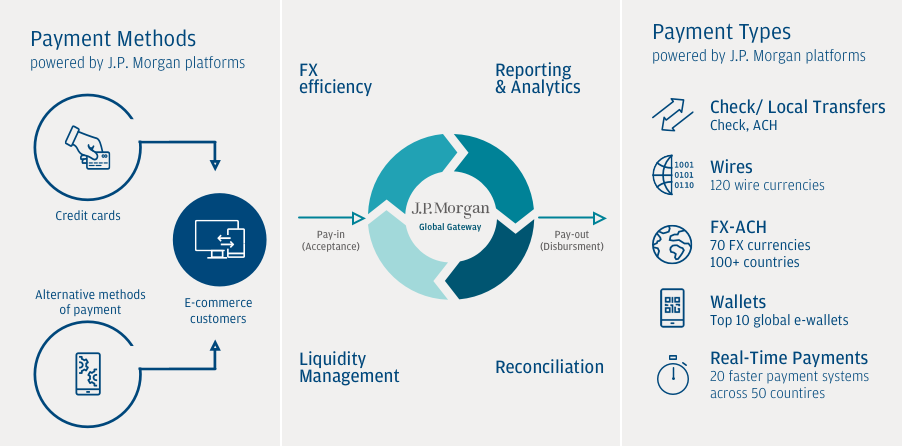

Payment Methods powered by J.P. Morgan platforms

- Credit cards

- E-commerce customers

- Alternative methods of payments

Pay-In (Acceptance) - J.P. Morgan Global Gateway - Pay-out (Disbursement)

- FX efficiency

- Liquidity Management

- Reporting & Analytics

- Reconciliation

Payment Types powered by J.P. Morgan platforms

- Check/Local Transfers - Check, ACH

- Wires - 120 wire currencies

- FX-ACH - 70 FX currencies 100+ countries

- Wallets - Top 10 global e-wallets

- Real-Time Payments - 20 faster payments systems across 50 countries

Real-Time Payments: Driving disruptive innovation

The world of always-on, contextual commerce includes an emerging need for faster payments. Customers, workers, merchants and suppliers want a quicker way to do business that fits into their 24/7/365 lifestyle. A convergence of these global trends is feeding expectations and are driving a shift towards Real-time Payments.

Treasury in 2025: What it Could Look Like

We examine how the cash management industry is transforming and what the treasury of tomorrow might look like.

5 Trends Driving the Payments Revolution

Explore the factors driving the payments revolution and find out how treasurers can thrive.

To learn more, please contact your J.P. Morgan Treasury Services representative.

This material was prepared exclusively for the benefit and internal use of the JPMorgan client to whom it is directly addressed (including such client’s subsidiaries, the “Company”) in order to assist the Company in evaluating a possible transaction(s) and does not carry any right of disclosure to any other party. This material is for discussion purposes only and is incomplete without reference to the other briefings provided by JPMorgan. Neither this material nor any of its contents may be disclosed or used for any other purpose without the prior written consent of JPMorgan.

J.P. Morgan, JPMorgan, JPMorgan Chase and Chase are marketing names for certain businesses of JPMorgan Chase & Co. and its subsidiaries worldwide (collectively, “JPMC”). Products or services may be marketed and/or provided by commercial banks such as JPMorgan Chase Bank, N.A., securities or other non-banking affiliates or other JPMC entities. JPMC contact persons may be employees or officers of any of the foregoing entities and the terms “J.P. Morgan”, “JPMorgan”, “JPMorgan Chase” and “Chase” if and as used herein include as applicable all such employees or officers and/or entities irrespective of marketing name(s) used. Nothing in this material is a solicitation by JPMC of any product or service which would be unlawful under applicable laws or regulations.

Investments or strategies discussed herein may not be suitable for all investors. Neither JPMorgan nor any of its directors, officers, employees or agents shall incur in any responsibility or liability whatsoever to the Company or any other party with respect to the contents of any matters referred herein, or discussed as a result of, this material. This material is not intended to provide, and should not be relied on for, accounting, legal or tax advice or investment recommendations. Please consult your own tax, legal, accounting or investment advisor concerning such matters.

Not all products and services are available in all geographic areas. Eligibility for particular products and services is subject to final determination by JPMC and or its affiliates/subsidiaries. This material does not constitute a commitment by any JPMC entity to extend or arrange credit or to provide any other products or services and JPMorgan reserves the right to withdraw at any time. All services are subject to applicable laws, regulations, and applicable approvals and notifications. The Company should examine the specific restrictions and limitations under the laws of its own jurisdiction that may be applicable to the Company due to its nature or to the products and services referred herein.

Notwithstanding anything to the contrary, the statements in this material are not intended to be legally binding. Any products, services, terms or other matters described herein (other than in respect of confidentiality) are subject to the terms of separate legally binding documentation and/or are subject to change without notice.

JPMorgan Chase Bank, N.A. Member FDIC. JPMorgan Chase Bank, N.A., organized under the laws of U.S.A. with limited liability.