3 min read

Boston’s multifamily market remains one of the nation’s most durable apartment markets entering mid-2026. Despite elevated interest rates, a slower office recovery and continued affordability pressures, the region consistently attracts long-term capital due to its diversified economy, globally recognized universities, constrained housing supply and highly educated workforce.

The market recorded net absorption of roughly 3,800 units against a wave of 6,500 new deliveries in 2025, according to Moody’s, supporting healthy occupancy levels even amid supply pressure. Vacancy across the Greater Boston metro stabilized at 6.4% in the first quarter of 2026, and is expected to rise slightly to 6.5% by the end of the year. That’s below the national average, 6.8%.

Boston’s multifamily fundamentals benefit from several structural advantages:

- High barriers to entry and restrictive zoning

- Strong renter demand driven by higher-for-longer mortgage rates and limited single-family housing affordability

- A large student and young professional population

- Consistent demand from the healthcare, technology, education and life sciences sectors

Mid-market apartments outperform luxury assets

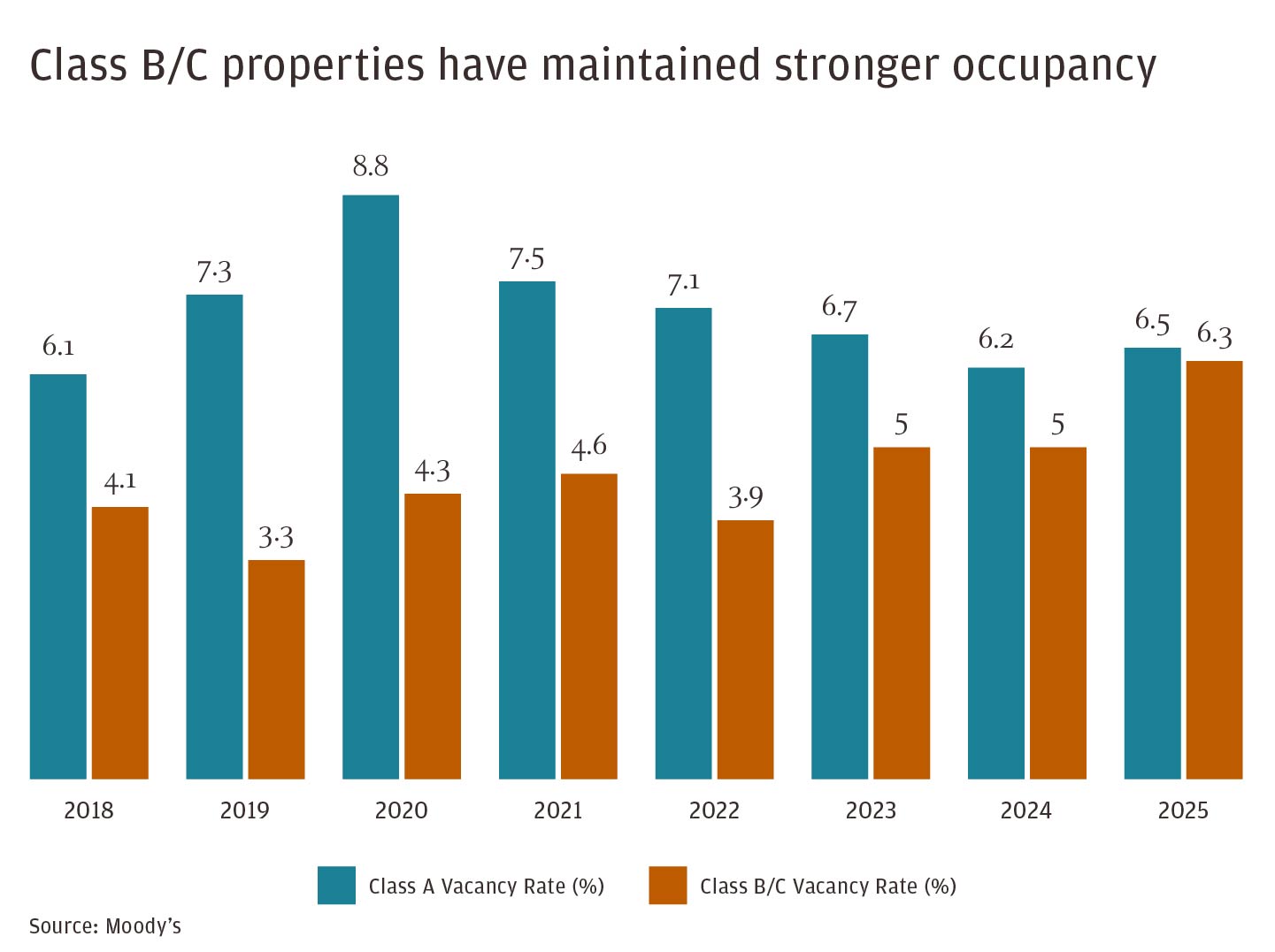

One of the clearest trends over the past decade has been the relative strength of Class B/C workforce housing compared with luxury Class A product.

The gap narrowed in 2025 as Class B/C units accounted for a larger than usual share of new construction. The vacancy rate for Class B/C units stabilized at 6.3% in the first quarter of 2026 as average asking rent rose 0.5% over the prior quarter. The Class A vacancy rate rose to 6.6%, with 1.3% growth in asking rent. Still, existing mid-tier properties have generally maintained stronger occupancy and rent performance over the past decade.

Bar chart titled “Class B/C properties have maintained stronger occupancy” comparing vacancy rates for Class A properties and Class B/C properties from 2018 to 2025. Class A vacancy rates (teal bars) are consistently higher than Class B/C vacancy rates (orange bars) across all years shown.

Data points for Class A vacancy rates: 6.1% in 2018, 7.3% in 2019, peaking at 8.8% in 2020, then declining to 7.5% in 2021, 7.1% in 2022, 6.7% in 2023, 6.2% in 2024, and 6.5% in 2025.

Data points for Class B/C vacancy rates: 4.1% in 2018, 3.3% in 2019, 4.3% in 2020, 4.6% in 2021, 3.9% in 2022, 5.0% in 2023, 5.0% in 2024, and 6.3% in 2025.

Overall, the chart shows that Class B/C properties maintained lower vacancy rates (indicating stronger occupancy) than Class A properties throughout the period, although the gap narrows by 2025. Source: Moody’s.

Rent growth has moderated from the post-pandemic surge across both asset classes, with annual gains forecast to remain in the low single digits in the coming years, according to Moody’s. Boston rents remain high by national standards, but operators are increasingly prioritizing occupancy and retention over aggressive hikes.

Development grows more selective

Boston has been in a cycle of elevated construction. The market added 6,538 new units in 2025, and inventory grew 9.6% over the past five years, according to Moody’s. But the pipeline is shrinking: 2026 deliveries are expected to drop to roughly 3,700 units before declining further over the next three years.

Reduced construction is expected to support a return to positive effective rent growth, forecasted at 1.3% in 2026, up from -1.9% in 2025, according to Moody’s.

Developers are becoming increasingly selective due to:

- Elevated interest rates

- Higher construction and labor costs

- Slower lease-up assumptions

- Reduced availability of construction debt

Developers are also shifting from luxury projects toward more attainable housing, reflecting changing investor priorities and renter demand for affordability. Slightly more than half of new units delivered in 2025 fell within the Class B or C category, according to Moody’s. Over the prior four years, Boston added nearly three new Class A units for each new Class B or C unit.

The region’s long-term housing shortage supports multifamily fundamentals even as near-term supply temporarily pressures rents in select submarkets.

Investment sales on the rise

Boston multifamily investment sales activity improved throughout 2025 as investors adjusted to higher rates and pricing expectations began to reset.

Cap rates expanded modestly during the rate cycle but remain relatively compressed. In the first quarter of 2026, Boston’s size-weighted estimated average multifamily cap rate was 5.6%, according to Moody’s.

Private investors have remained highly active, particularly in smaller and mid-sized transactions, while institutional investors continue targeting well-located core and core-plus assets with long-term hold strategies.

Transit-oriented development accelerates

The ongoing implementation of Massachusetts’ MBTA Communities framework is expected to support additional multifamily development near public transit corridors over the coming years.

Transit-oriented housing remains highly attractive to both renters and employers, especially as hybrid work patterns evolve. Submarkets with strong commuter access and walkability continue to outperform from both a leasing and investment perspective.

The slowdown in life sciences development has also created acquisition and redevelopment opportunities for multifamily investors near transit hubs previously dominated by biotech competition.

Outlook for the remainder of 2026

Boston’s multifamily market is expected to remain stable through year-end, though operating conditions will likely stay more balanced than during the aggressive rent-growth years immediately following the pandemic.

Key trends expected to shape the market include:

- Continued strong demand for workforce and mid-market housing

- Moderating but positive rent growth

- Fewer new construction starts

- Increasing investor focus on operational efficiency and resident retention

- Strong long-term renter demand driven by homeownership affordability challenges

While near-term supply growth may continue pressuring rents in select urban submarkets, Boston’s structural housing shortage, highly educated labor force and diversified economy position the region as one of the nation’s strongest long-term multifamily investment markets.

Whether you’re ready for financing or looking to streamline your operations, connect with our Boston lending, payments and liquidity team.

JPMorgan Chase Bank, N.A. Member FDIC. Visit jpmorgan.com/commercial-banking/legal-disclaimer for disclosures and disclaimers related to this content.