3 min read

Orange County’s multifamily market is expected to remain resilient in 2026, despite slowing employment and population growth.

“There’s a quality-of-life factor for people who want to be near LA’s economic powerhouse, but want to live in an area that’s less crowded and more open,” said Matthew Krasinski, Senior Regional Sales Manager at Chase.

Vacancies are expected to increase slightly to 4.7% from 4.5% the prior year, according to Moody’s. Effective rents are projected to rise 0.9% year over year, holding steady at 2025’s growth rate.

Workforce housing drives market strength

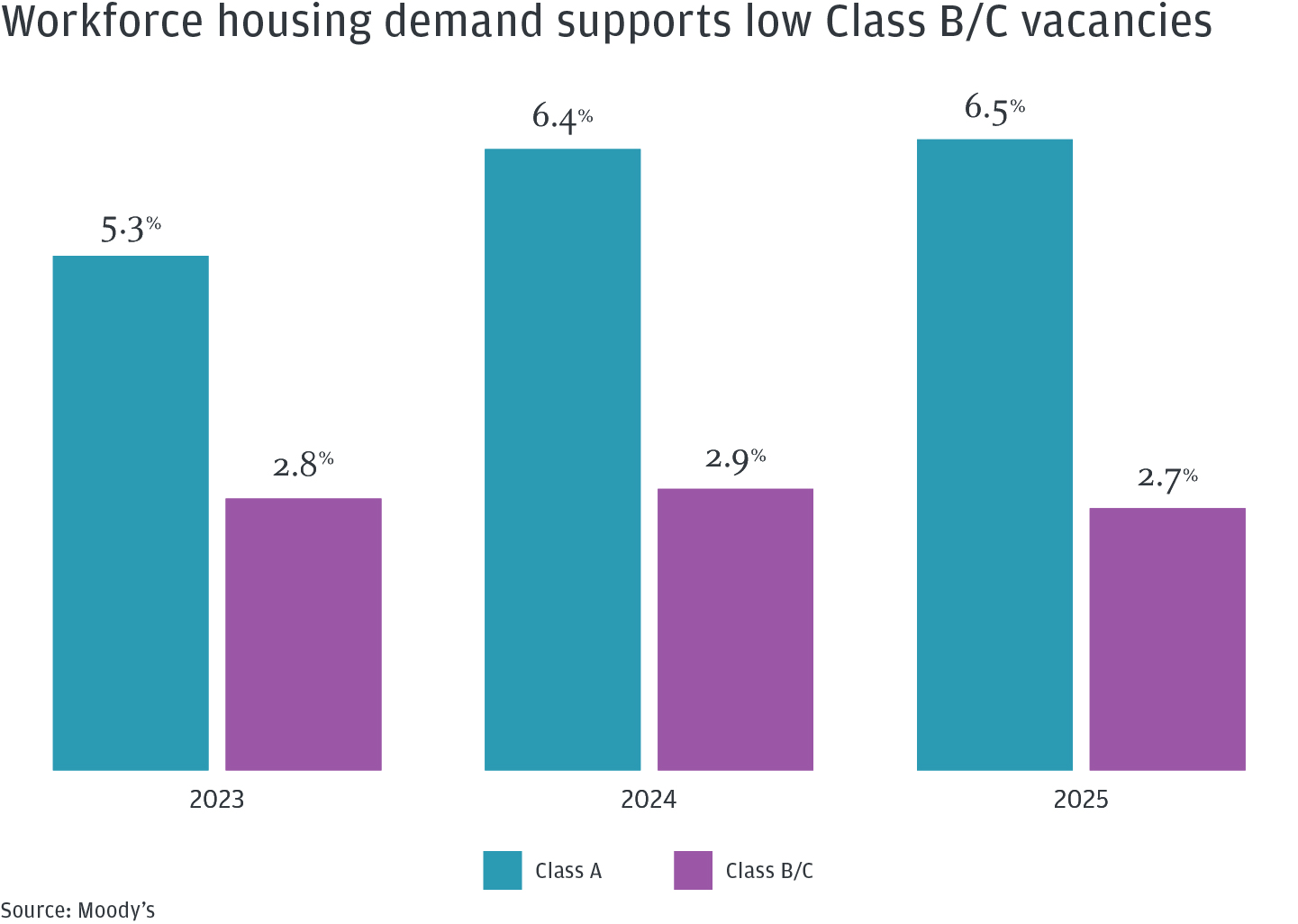

Orange County’s multifamily market shows a clear divide between asset classes: Class B and C properties had a 2.9% vacancy in the first quarter of 2026, while Class A vacancy remained elevated at 6.5%.

“The tight supply of workforce and affordable housing properties shows why renter demand tends to be very durable,” Krasinski said.

The chart shows the average annual vacancy rate for Class A and Class B/C multifamily properties in Orange County between 2023 and 2025. The vacancy rate at Class A properties is consistently higher, and the gap has grown. Class A properties’ average annual vacancy rate rose from 5.3% in 2023 to 6.5% in 2025. At Class B/C properties, the vacancy rate held relatively steady. It rose from 2.8% in 2023 to 2.9% in 2024, then fell to 2.7% in 2025.

Source: Moody's

Consider Orange County’s Tustin submarket. Nearly half of all new units built in Orange County last year were in Tustin—all delivered in the fourth quarter, according to Moody’s. As Tustin’s inventory grew 10.8% quarter over quarter, the Class A vacancy rate tripled. The vacancy rate at Class B and C properties, meanwhile, rose just 0.1% and remained down year over year.

“A shrinking construction pipeline should help ease supply pressures and support a gradual improvement in market fundamentals,” said Lu Chen, Senior Economist at Moody’s.

Even so, with population growth slowing and renovation costs rising, some multifamily owners are focusing on keeping turnover low.

“We’re seeing customers would rather work with their current renter to keep them in place,” said Lynnette Antosh, Senior Regional Sales Manager at Chase.

Interest rate uncertainty

A moderation in interest rates and an increase in cap rates are starting to create more buying opportunities.

“The difference between where cap rates are and where customers think they’ll be is getting smaller, which has spurred more activity,” Krasinski said.

The path for interest rates remains uncertain. The Federal Reserve is balancing efforts to stabilize prices and maximize employment. Amid that uncertainty, some multifamily owners are holding off on locking a long-term interest rate when seeking a new apartment loan or refinancing. Some strategies include:

- Choosing a shorter, three- to five-year loan term

- Riding out the variable-rate portion of a loan rather than refinancing

“We’re seeing customers closely watch the volatility in the rate environment, maybe more so than they have in the past,” Krasinski said.

Managing rising operational costs

Operational costs are rising. Strategic liquidity management can help. Using fast, frictionless payment systems to collect revenue faster and establishing longer payment terms with vendors can improve your cash positioning. Even short-term operational reserves can earn interest.

“When you’re working with experts who specialize in commercial real estate and have solutions tailored to owner-operators, you can deploy capital more effectively,” Antosh said.

If you already have a capital management plan, consider reviewing it with your payments and liquidity team to make sure it still fits your business.

Your payments and liquidity team can also help you take advantage of fraud protection tools and stay current on commercial real estate cybersecurity best practices.

Adding ADUs

Finding ways to create more cash flow at a property can be a challenge. One potential opportunity: accessory dwelling units (ADUs).

ADUs turn underutilized space at a property into a new apartment. They’re often built as detached units or converted garages and also known as granny flats, in-law suites and garage apartments. There are regulations to navigate, and they require an upfront investment.

“It’s an opportunistic strategy,” Antosh said. “It may not move the needle on housing supply but can be a source of added revenue, especially in areas with low vacancies like Orange County.”

Whether you’re ready for financing or looking to streamline your operations, reach out to our Orange County lending, payments and liquidity team.

JPMorgan Chase Bank, N.A. Member FDIC. Visit jpmorgan.com/commercial-banking/legal-disclaimer for disclosures and disclaimers related to this content.