Payments

PAYMENTS OUTLOOK

Five shifts powering payments

Unlock clarity and control to lead with insight and agility

PAYMENTS OUTLOOK

Unlock clarity and control to lead with insight and agility

April 23, 2026

The global economy is expected to remain resilient in 2026, although trade tensions and the risk of conflict are impacting growth, according to J.P. Morgan Global Research.1 For finance teams, this uncertain landscape is translating to a focus on optimizing liquidity and working capital and creating an always-on, connected treasury powered by programmable automation and blockchain technology. Meanwhile, the advancement of AI is creating risks and opportunities in fraud prevention, as businesses aim to deliver the seamless, personalized payment experiences customers want while protecting security.

Through proprietary research and the expertise of our global Payments leaders, we’ve looked further into these key shifts and how companies may adapt to them in coming years.

In today’s volatile global economic environment, being able to access cash quickly, across any location or currency, is more important than ever. Finance teams are therefore looking to create greater visibility and control in liquidity.

To achieve this, we’re increasingly seeing a move toward real-time liquidity. Real-time liquidity creates a centralized view of a company’s cash position at any given time, across all operating entities. Made possible by streamlining legal entities and bank accounts and integrating banking with TMS or ERP software, it creates visibility and enables quick, informed decision-making.

A centralized view of liquidity also allows for automation, reducing the need for manual processing (identified as the biggest pain point in payments infrastructure).2

Automation enables efficient and intelligent cash movement, for example, deploying cash just-in-time through automated sweeping.

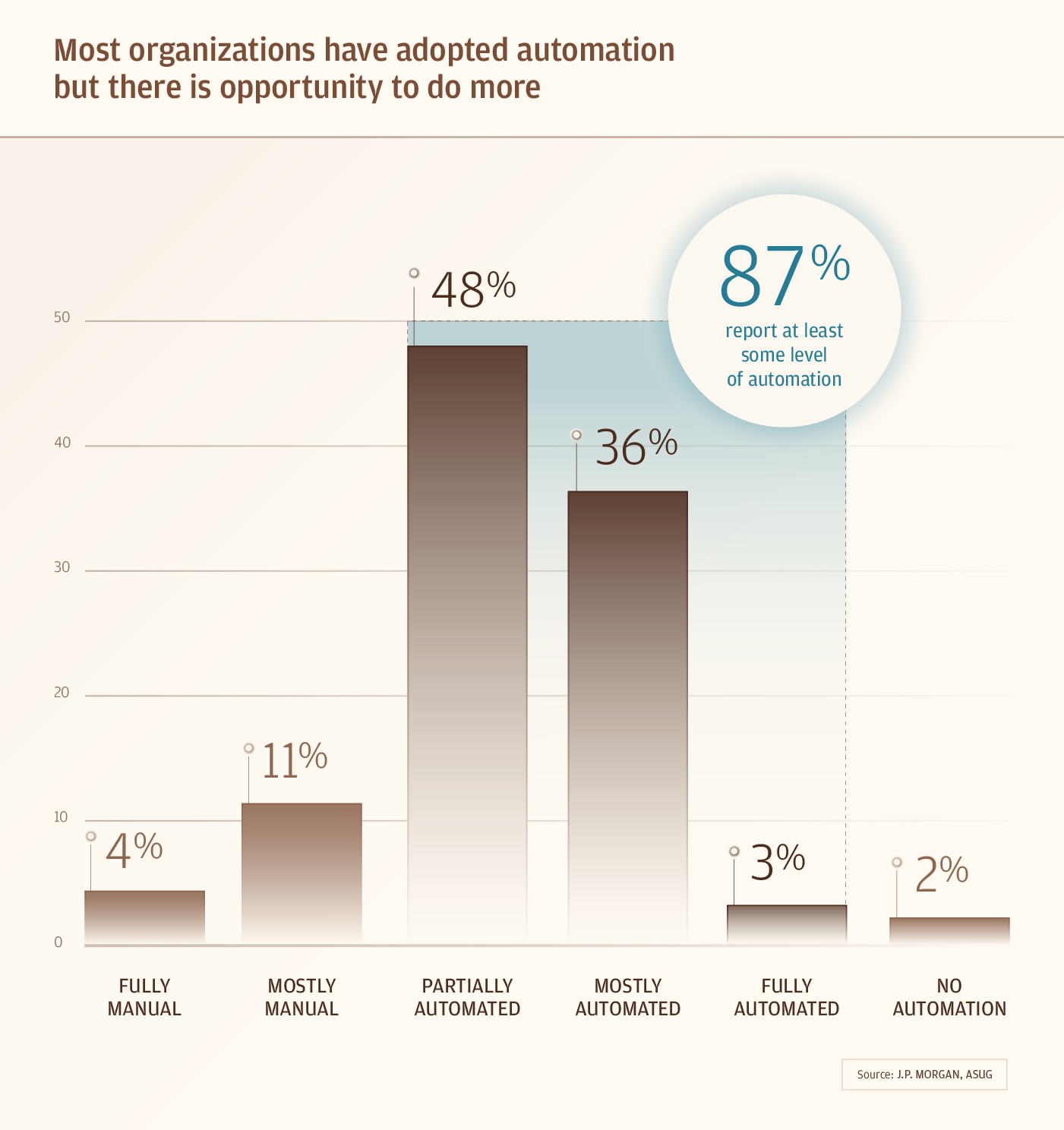

While most organizations have adopted automation, our research shows there is opportunity to do more.3

The move towards real-time liquidity is opening up the possibility of borderless liquidity. With virtual account structures for intercompany trade settlement, finance teams can manage internal cash flows and optimize foreign exchange without moving funds between accounts or locations. This improves overall liquidity, while bypassing the complexities of currency conversion.

While most organizations have adopted automation, our research shows there is opportunity to do more. 87% of organizations have some level of automation in treasury and payments infrastructure, but only 39% describe their systems as mostly or fully automated.

Source: J.P. Morgan, ASUG

“Automation is transforming receivables and payment reconciliation by drastically reducing manual intervention and enabling near real-time posting of payments to invoices.”

Michelle Conklin

Managing Director, Head of Receivables Solutions at J.P. Morgan

If turbulent conditions disrupt cashflow, being able to move funds quickly from different areas of the business can be a vital safeguard. Payment centralization is increasingly being used. Instead of relying on local offices, a regional treasury center (RTC) or an in-house bank is used to consolidate cash.

Another tool is multicurrency notional pooling, where multiple bank account balances are aggregated to provide a single cash position. This allows treasuries to use surplus cash from one account to offset the deficit in another, without the need for intercompany loans and FX hedges. Dynamic markets require a new approach to working capital. Due to changing trade dynamics, companies are reorganizing supply chains, which is forcing them to rethink their approach to trade and working capital management.

Finance teams are looking to gain real-time visibility of their accounts receivables ecosystem and embed automation into TMS to cut the admin load and make it easier to access non-debt financing. The ongoing surge in AI investment is also contributing to the need to optimize working capital.

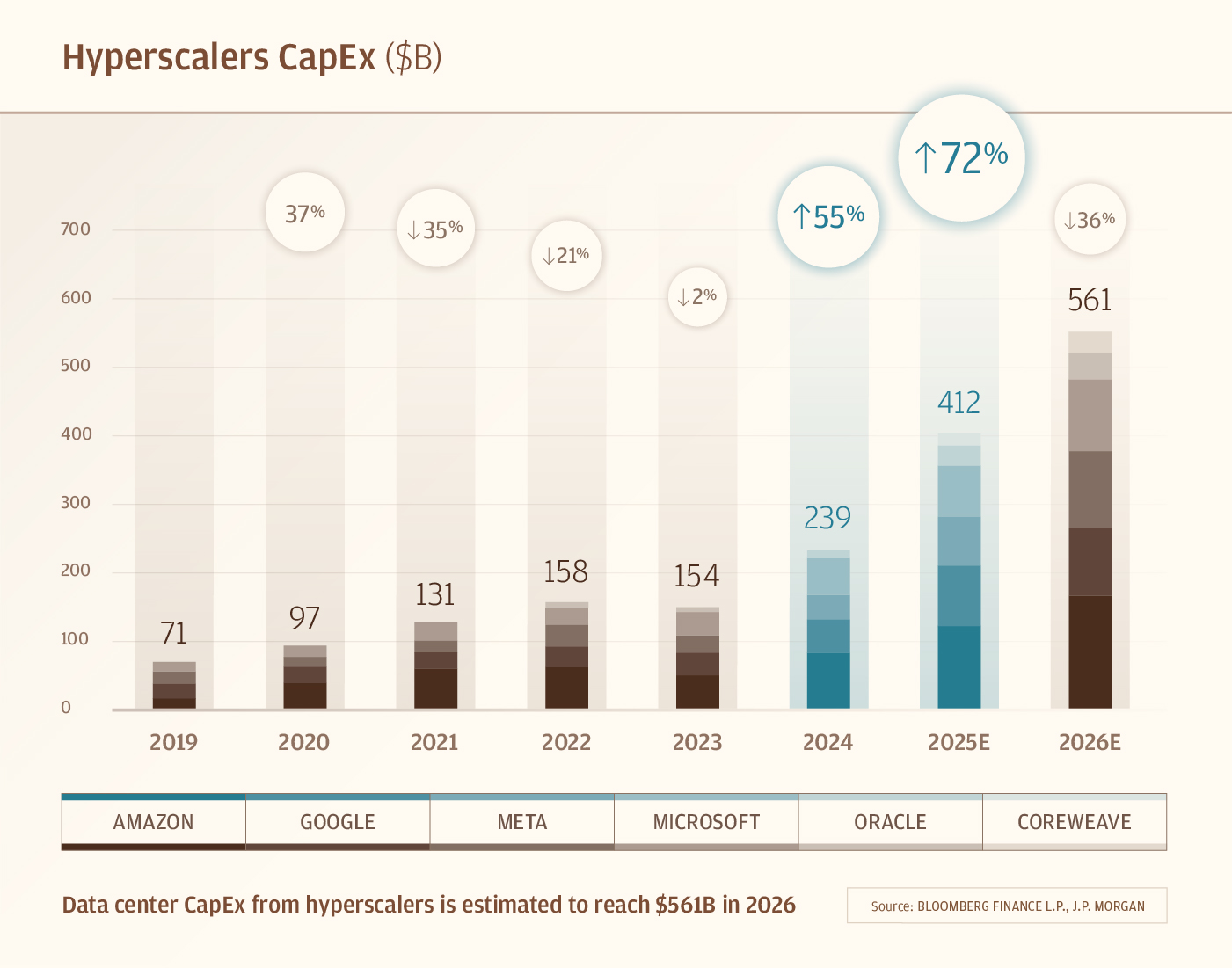

AI uptake is driving working capital demands. An intelligent approach to working capital is also critical to finance the ongoing surge in AI investment. According to J.P. Morgan estimates, about 122GW in global data center infrastructure will be installed between 2026 and 2030. In 2026, there is estimated to be approximately $561 billion in CapEx from the hyperscalers alone.4

“In response to increased tariffs, many companies are moving production back to the U.S. or neighboring countries such as Mexico. Relocating supply chains in this way requires both higher capital expenditure, as well as the negotiation of new buyer-supplier relationships. Manufacturing in countries with higher labor costs also increases overall demand for working capital.”

Keith Murphy

Managing Director, Head of North America Sales, J.P. Morgan Trade & Working Capital Finance

Chart titled “Hyperscalers CapEx ($B).” A stacked bar chart shows annual data center capital expenditures for major hyperscalers (Amazon, Google, Meta, Microsoft, Oracle, CoreWeave) from 2019 to 2026E. Total CapEx by year: 2019 $71B; 2020 $97B (up 37%); 2021 $131B (down 35%); 2022 $158B (down 21%); 2023 $154B (down 2%); 2024 $239B (up 55%); 2025E $412B (up 72%); 2026E $561B (down 36%). A caption notes: “Data center CapEx from hyperscalers is estimated to reach $561B in 2026.”

Source: Bloomberg Finance L.P., J.P. Morgan

In today’s 24/7 on-demand economy, businesses and consumers increasingly expect transactions to clear instantly (account-to-account payments are predicted to be worth $195 billion globally by 2030.5)

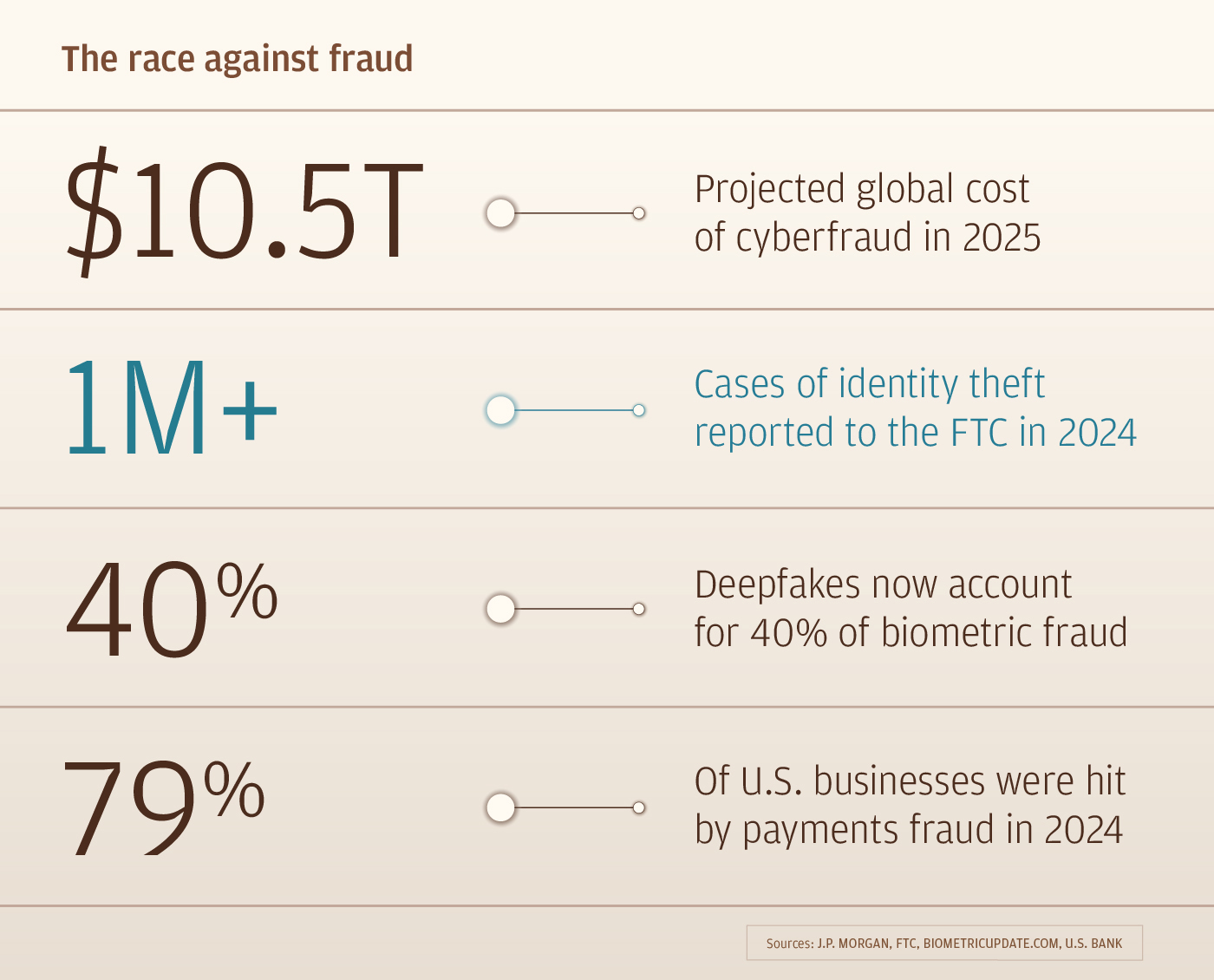

But with money changing hands faster, businesses need to be confident the person on the other side of the transaction is who they say they are, particularly when transactions are irreversible as with A2A payments. This tension is fueling a contest of relentlessness between businesses and scammers, as companies rush to invest in fraud prevention tools, while cyber criminals adopt more sophisticated technology to try and sidestep corporate defenses.

$10.5 trillion—global cost of cyberfraud in 20256

1 million+ cases of identity theft reported to the FTC in 20247

40% of biometric fraud attributed to deepfakes8

79% of U.S. businesses were hit by payments fraud in 20249

Source: J.P. Morgan, FTC, Biometricupdate.com, U.S. Bank

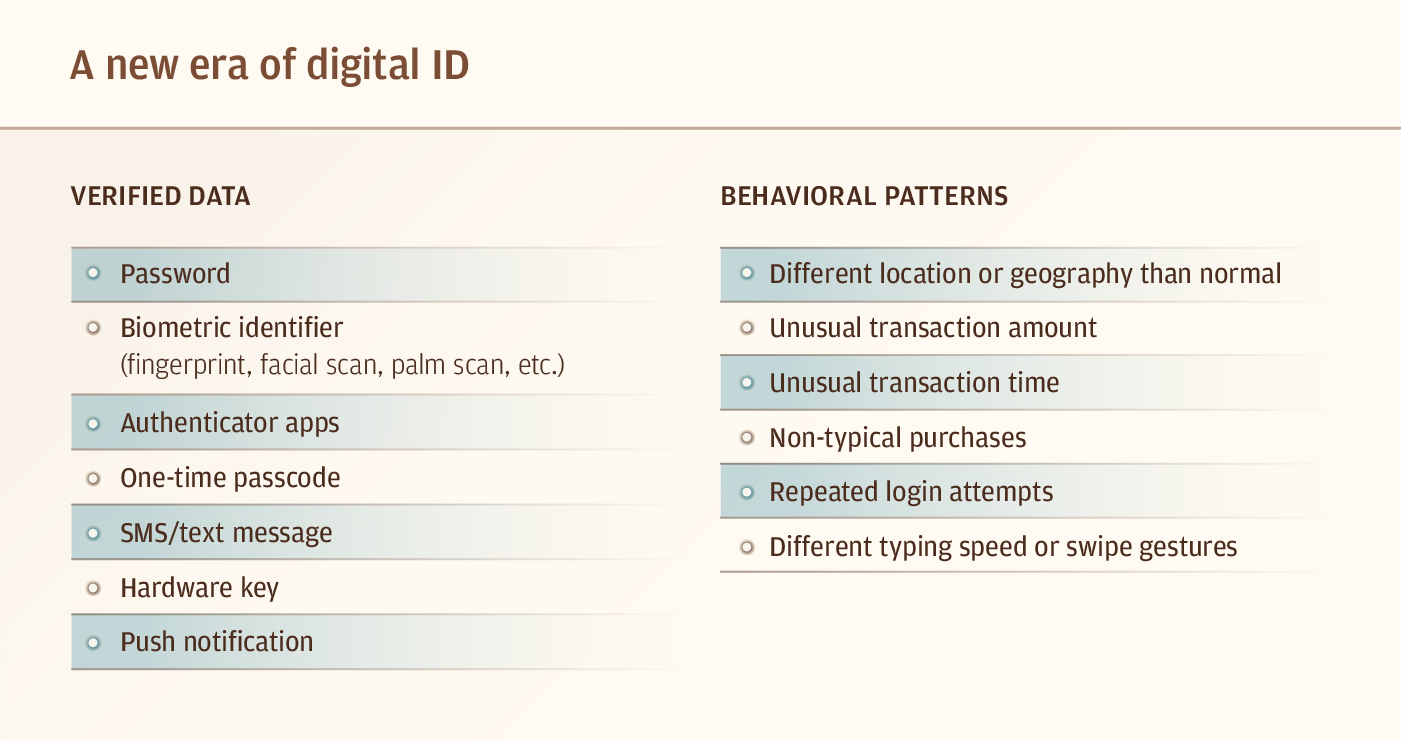

In the face of evolving threats, companies are looking to supplement existing verification controls with behavioral data.

AI can use this data to build a clearer picture of a customer’s digital footprint and flag when something seems off, such as if a counterparty is making a payment in a different location than normal.

Verified data

Password

Biometric identifier

Authenticator apps

One-time passcodes

SMS/text messages

Hardware keys

Push notifications

Different location/geography

Unusual transaction amount

Unusual transaction time

Nontypical purchases

Repeated login attempts

Different typing speed/swipe gestures

In the U.S., the U.S. NIST SP 800-63 Digital Identity Guidelines provide technical requirements for meeting digital identity assurance levels.

In Europe, legislation is being passed to support the launch of an EU Digital Identity Wallet. In India, the Aadhaar national ID scheme is already underpinning around 3 billion payment authentications every month.

“When you are using something like A2A payments, you need to onboard people carefully and ensure that the information being provided is validated. And then you also need the behavioral component, which is, ‘Are they behaving correctly? Are they acting like themselves?’ Getting this right is vital, as no one’s going to want to do business with a company if they don't feel like they can trust being on their platform.”

Vincent Meluzio

Payments Product Solutions Director and Trust & Safety Solutions Lead at J.P. Morgan

Digital transformation is changing the way people make payments, and consumers now expect fluid omnichannel experiences with seamless payment processes.

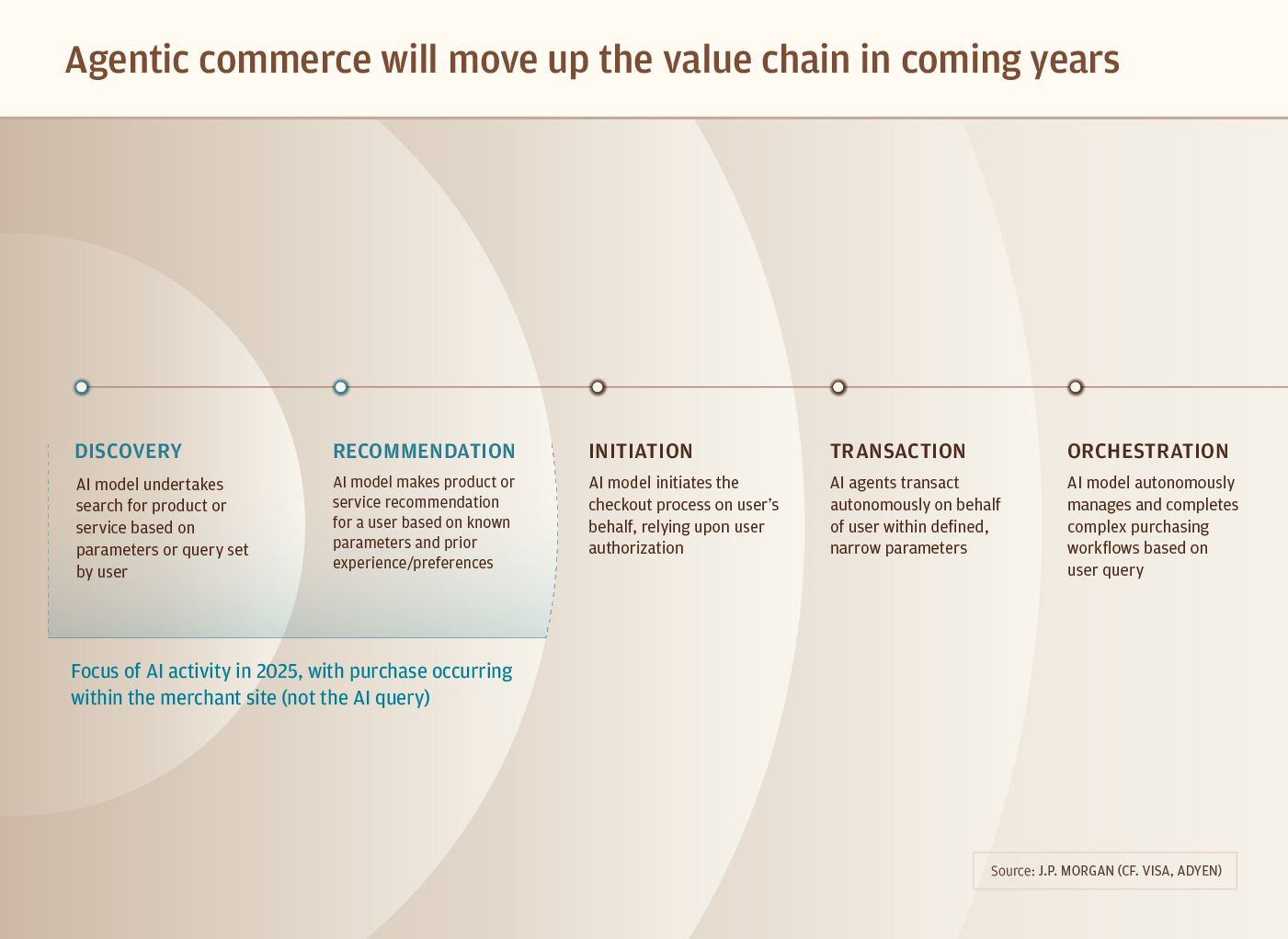

Part of this shift involves agentic commerce, where consumers ask agentic AI to autonomously find, research, recommend and purchase products on their behalf. Agentic AI is predicted to be responsible for up to a quarter of the U.S. e-commerce market by 2030.10 We expect this to begin with repeat, low-risk items like groceries, before evolving to high-value items like tickets and automobiles.

Infographic titled “Agentic commerce will move up the value chain in coming years.” A horizontal value-chain timeline shows five stages: Discovery, Recommendation, Initiation, Transaction, and Orchestration. Discovery: AI model searches for a product or service based on user parameters or query. Recommendation: AI model makes product or service recommendations based on known parameters and prior user experience/preferences. Initiation: AI model initiates checkout on the user’s behalf, relying on user authorization. Transaction: AI agents transact autonomously on behalf of the user within defined, narrow parameters. Orchestration: AI model autonomously manages and completes complex purchasing workflows based on user query. Discovery and Recommendation are highlighted with a note: “Focus of AI activity in 2025, with purchase occurring within the merchant site (not the AI query).”

Source: J.P. Morgan (CF. VISA, ADYEN)

For businesses, adapting to agentic commerce means adopting “sell-side” AI agents that will manage inventory and pricing, and marketing to “buy-side” agents to ensure their products are chosen over a competitor’s.

Brand loyalty will be less powerful as AI agents focus on price, availability and delivery times.

Tailored payment options are an essential part of this new world of commerce.

While 65% of consumers expect frictionless payments, only 45% of merchants are prioritizing this,11 highlighting an area where businesses can differentiate themselves. Companies can offer emerging payment options such as Request for Pay, cryptocurrencies, digital wallets and QR codes, as well as online and in-store buy now, pay later (BNPL) options. Another option is loyalty schemes. By leveraging transaction data, businesses can create programs that offer personalized discounts or rewards if a customer chooses a qualifying payment option.

84%

of consumers say they want one-click checkouts12

25%

of U.S. consumers say the ability to collect points or discounts drives their payments choice13

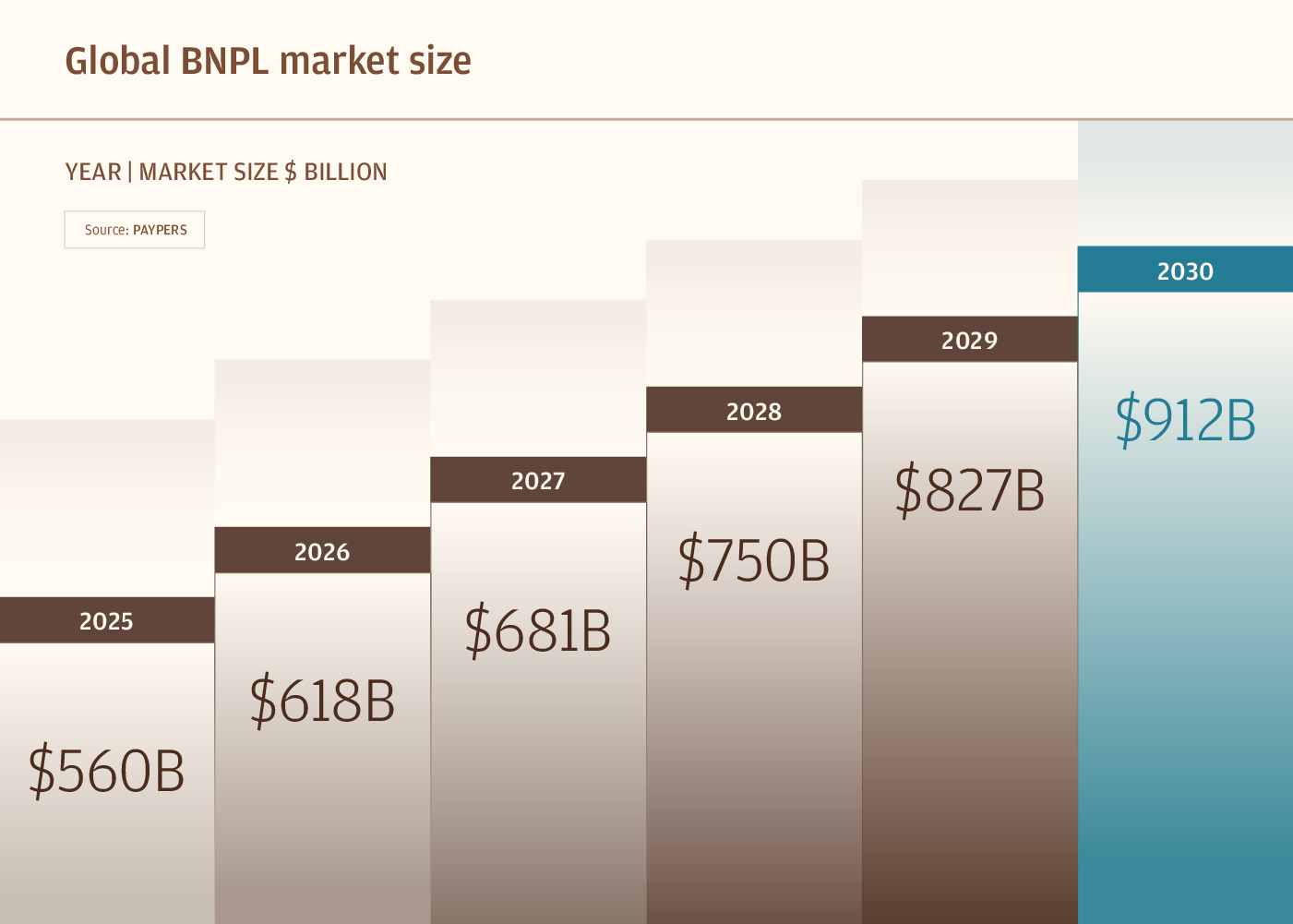

$911.8B

Predicted value of the BNPL market by 2030

Businesses can go one step further when enhancing payments experiences by building new payment ecosystems through embedded finance.

A closed-loop banking network enables merchants to process customer payments without an intermediary, saving costs and streamlining the checkout journey. Closed-loop systems also enable businesses to create extensive marketplaces where they can sell their own goods and goods from other companies. Boston Consulting Group estimates the potential market for embedded finance in the U.S., Canada and Europe is roughly $185 billion across payments, capital solutions, accounts and card issuing.14

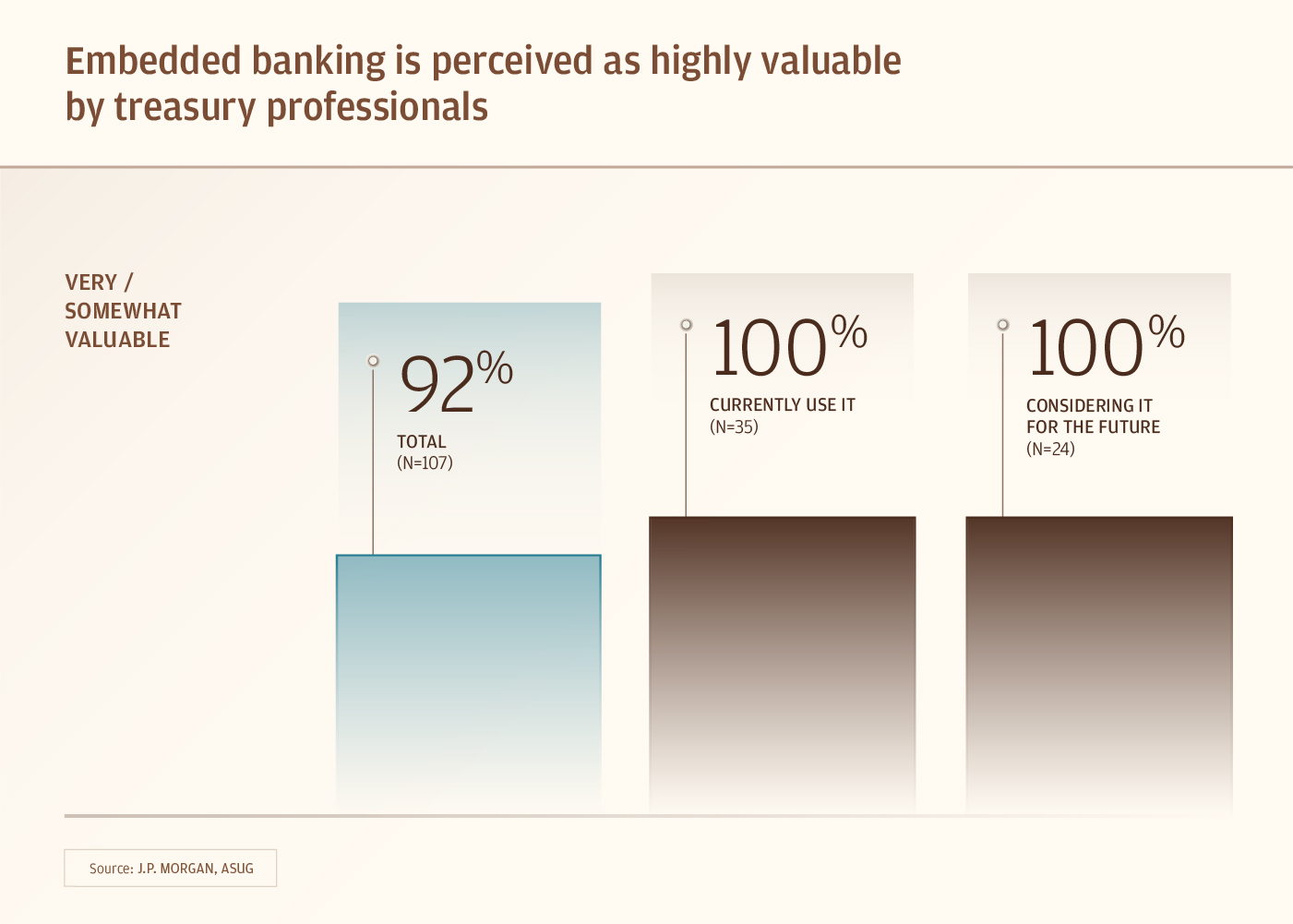

Infographic titled “Embedded banking is perceived as highly valuable by treasury professionals.” Under the label “Very / somewhat valuable,” three vertical bars summarize survey results: 92% of total respondents (N=107) rate embedded banking as very or somewhat valuable; among those who currently use embedded banking, 100% (N=35) rate it valuable; among those considering it for the future, 100% (N=24) rate it valuable.

Source: J.P. Morgan and ASUG.

In addition to offering multiple payment methods, businesses can consider other options such as installment plans.

While BNPL was once a feature solely of online checkouts, it is now increasingly being offered in stores, too. To that end, the size of the global BNPL market is expected to grow to $911.8 billion by 2030 from $560 billion in 2025.15

“Payments have to evolve with what consumers want, and they have to evolve to continue to be seamless. People also want their payments to follow them across channels. They don’t want to have to use a different payment instrument just because they are shopping online.”

Oseyi Ikuenobe

Managing Director, Head of Omnichannel Solutions at J.P. Morgan

Infographic titled “Global BNPL Market Size.” A stepped bar chart labeled “Year | Market Size $ Billion” shows projected global market size increasing each year: 2025 $560B, 2026 $618B, 2027 $681B, 2028 $750B, 2029 $827B, and 2030 $912B (highlighted in teal).

Source: Paypers

Organizations are increasingly undergoing digital transformation to create always-on, digital-first and data-enabled treasury operations, characterized by connectivity, automation and embedded banking.

While needs vary by business size, transformation can drive time and cost efficiencies and unlock greater clarity and control. New systems will need the capacity to process enormous amounts of data. Data harmonization initiatives such as the ISO 20022 data standard are reliant on digital transformation. As the flow of data expands, organizations need systems with the capacity to process it.

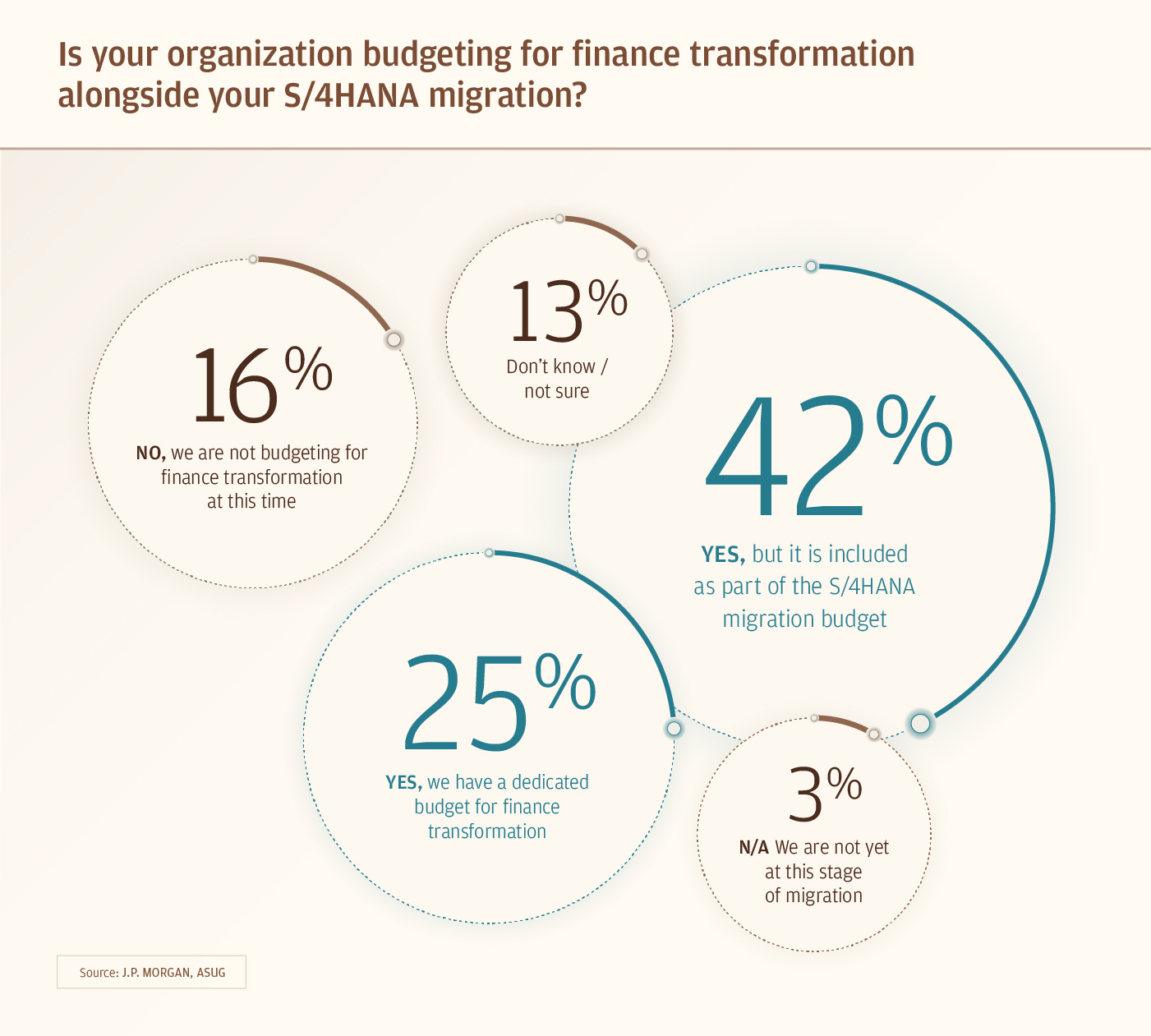

Infographic asks: “Is your organization budgeting for finance transformation alongside your S/4HANA migration?” Five bubble callouts show survey responses: 42% “Yes, but it is included as part of the S/4HANA migration budget”; 25% “Yes, we have a dedicated budget for finance transformation”; 16% “No, we are not budgeting for finance transformation at this time”; 13% “Don’t know / not sure”; 3% “N/A, we are not yet at this stage of migration.”

Source: J.P. Morgan, ASUG

“Legacy systems are like yesterday’s phones—functional, but fundamentally limiting. If we want real-time intelligence, AI-driven automation and always-on resiliency, we can’t build it on yesterday’s architecture. Transformation is what turns us from basic connectivity into intelligent, scalable, future-ready platforms.”

Patrick Burgess

Global Head of Connectivity and Developer Experience at J.P. Morgan

With data processing capabilities in place, teams can take advantage of AI tools in areas like risk management, transaction analysis and cash flow forecasting.

This can free people up to focus on more value-added work, allowing them to be more efficient and effective at what they do.

“AI has the potential to reshape the treasury function by making finance teams more productive and better informed, enabling them to move away from traditional data-entry tasks and focusing more on strategic advisory work.”

Chip McArthur

Head of Product, Treasury Services Data & Analytics at J.P. Morgan

Part of the digital-first treasury experience will include embedding banking and finance capabilities into ERP or TMS software. As many as 92% of treasury professionals view this as very or somewhat valuable.16

Embedding services can improve real-time visibility into an organization’s financial position, giving an instant snapshot of a business’s financial health. It can also unlock new innovation opportunities, for example automating cross-border reconciliation and accessing non-traditional payment rails such as blockchain.

Nearly 60% of Fortune 500 companies say they are planning to implement blockchain initiatives, with many of those focused on payments and settlements.17

Blockchain-powered tokenized money—such as deposit tokens, Blockchain Deposit Accounts (BDAs) and central bank digital currencies (CBDCs)—is speeding up payments and making it easier to move funds across borders, 24/7. This can avoid potential delays due to banking hours, settlement frictions or foreign exchange, improve cash flow and make payments more cost efficient.

Tokenization is picking up speed. The market for tokenized assets is gaining momentum, with 60% of institutions looking to increase their exposure to digital assets.18

Currently the market is still in a nascent phase, with a total market cap of around $25 billion.19 In the future, all assets will evolve with tokenization.

Finance teams can use tokenization to improve liquidity (due to the speed at which tokenized assets can be bought and sold, compared to the underlying assets). Meanwhile, for the asset management industry, tokenization could represent a $400 billion opportunity by making it easier to distribute alternative investments to individuals, such as private equity.20

Blockchain is making it possible to move away from the disparate systems-based world that underpins banking today to a connected, network-based world.

With network-based infrastructure, customers can use a single wallet as a digital ID and a single account to store all their assets in one place, all held on a shared ledger and governed by smart contracts. This could mean less friction, better customer experiences and more innovation opportunities.

The journey to a fully tokenized blockchain future

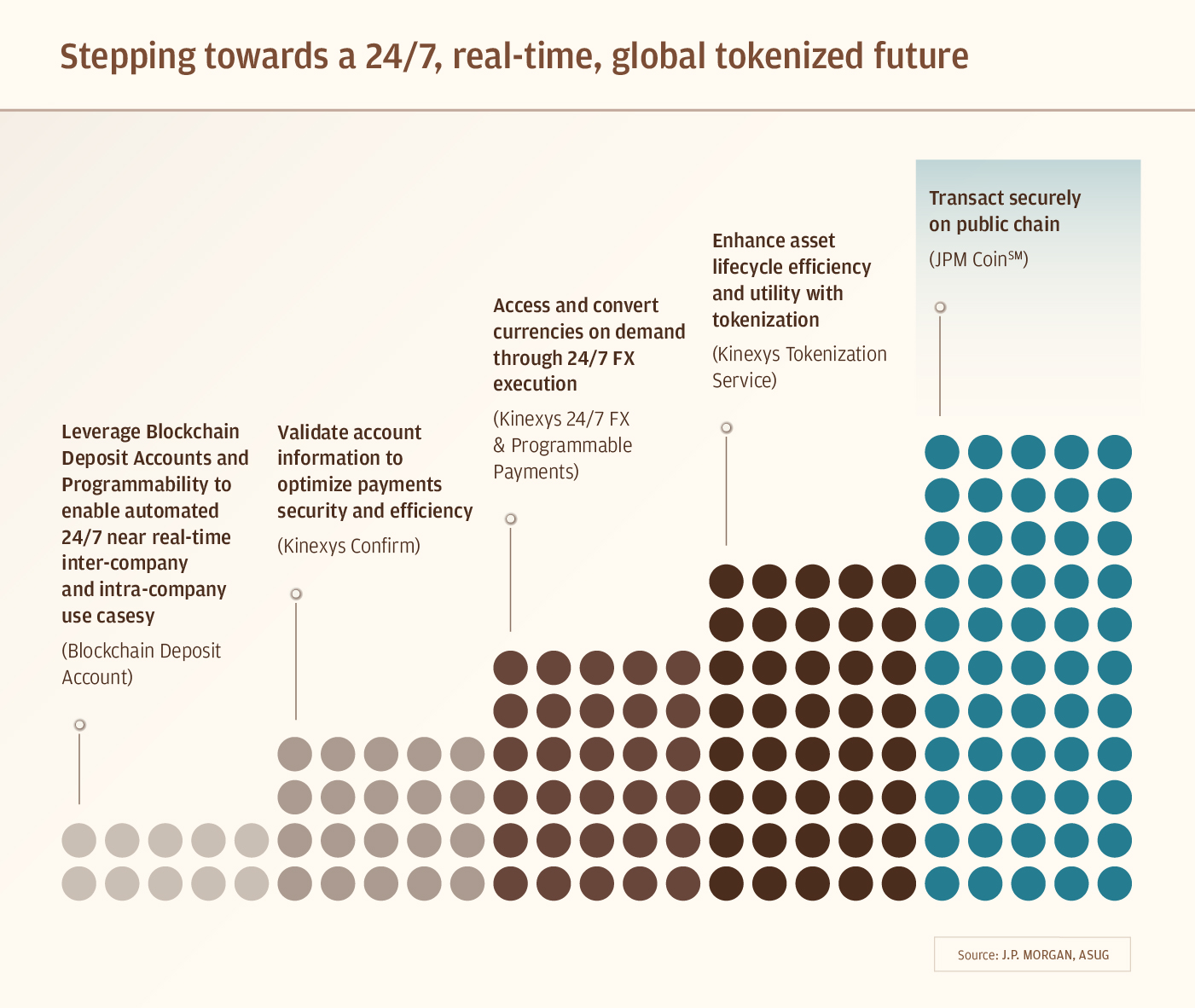

Given the scale of transformation involved in moving to a fully tokenized blockchain future, businesses will adapt incrementally. For example, organizations can ease into this technology by implementing intra-company 24/7, multicurrency, near real-time settlements through blockchain deposit accounts. They can then selectively start to explore and interoperate with use cases where they can leverage deposit tokens for payments on public blockchain.

Infographic titled “Stepping towards a 24/7, real-time, global tokenized future.” A left-to-right progression uses rising blocks of colored dots (light gray to dark brown to teal) to show stages and capabilities: “Leverage Blockchain Deposit Accounts and programmability to enable automated 24/7 near real-time inter-company and intra-company use cases (Blockchain Deposit Account)”; “Validate account information to optimize payments security and efficiency (Kinexys Confirm)”; “Access and convert currencies on demand through 24/7 FX execution (Kinexys 24/7 FX & Programmable Payments)”; “Enhance asset lifecycle efficiency and utility with tokenization (Kinexys Tokenization Service)”; and “Transact securely on public chain (JPM Coin℠).”

Source: J.P. Morgan, ASUG

“When existing payment systems and on-chain instruments, such as deposit tokens, interoperate, money stops being constrained by infrastructure and becomes a lever to power entirely new use cases.”

Abhinav Natarajan

Global Product Lead at Kinexys by J.P. Morgan

The pace and scale of technological change is creating new risks for businesses, but it is also opening up an exciting opportunity to modernize payments and the treasury function and transform how treasury and finance teams support their wider organizations.

Across the topics we’ve explored, one theme connects them all: the continual evolution of the role of finance teams. As AI technology, API connectivity and blockchain continue to automate routine functions, leaders will spend more time on strategic decision-making and other value-adding activities. By harnessing the power of technology, payments will become more creative, proactive and insightful—it will become more human, not less.

From being a mainly operational function, treasury and finance will increasingly take a leadership role, guiding the future direction of their organization.

We’ll continue exploring these topics in our Payments Outlook series, examining the latest developments and how organizations across the globe can adapt to the evolving landscape.

Learn more about how these trends are impacting the world of payments in 2026 and beyond.

J.P. Morgan, December 2025. ‘2026 market outlook: A multidimensional polarization.’ Available at: https://www.jpmorgan.com/insights/global-research/outlook/market-outlook. Accessed February 2026.

ASUG, December 2025. ‘Modernizing Payments Infrastructure: Embedded Finance, Automation, and Partner Value – Collaborative Research from ASUG and J.P. Morgan.’ Accessed February 2026.

ASUG, December 2025. ‘Modernizing Payments Infrastructure: Embedded Finance, Automation, and Partner Value – Collaborative Research from ASUG and J.P. Morgan.’ Accessed February 2026.

J.P. Morgan, Europe Equity Research, December 2025. ‘European Tech Hardware &Payments 2026 Outlook.’ Accessed February 2026.

Juniper Research, September 2025. ‘A2A Transaction Value to Reach $195 Trillion in 2030 Globally, Driven by Advanced Value-added Services.’ Available at: https://www.juniperresearch.com/press/a2a-transaction-value-to-reach-195-trillion-in-2030-globally-driven-by-advanced-value-added-services/. Accessed November 2025.

J.P. Morgan Strategic Research, November 2025. ‘J.P. Morgan Perspectives: Digital Future Under Threat: AI, Quantum and Geopolitical Cybersecurity Risks.’ Accessed February 2026.

FTC, March 2025. ‘New FTC data show a big jump in reported losses to fraud to $12.5 Billion in 2024.’ Available at: https://www.ftc.gov/news-events/news/press-releases/2025/03/new-ftc-data-show-big-jump-reported-losses-fraud-125-billion-2024. Accessed November 2025.

Biometricupdate.com, Nov 2025. ‘ Deepfake attacks now occur every five minutes, Entrust report warns.’ Available at: https://www.biometricupdate.com/202411/deepfake-attacks-now-occur-every-five-minutes-entrust-report-warns. Accessed November 2025.

US Bank, May 2025. ‘Fight the battle against payments fraud.’ Available at: https://www.usbank.com/corporate-and-commercial-banking/insights/risk/mitigation/battling-payments-fraud.html. Accessed November 2025.

Bain & Company, ‘2030 Forecast: How Agentic AI Will Reshape US Retail.’ Available at: https://www.bain.com/insights/2030-forecast-how-agentic-ai-will-reshape-us-retail-snap-chart/. Accessed January 2026.

Klarna, October 2021, ‘Retailers and shoppers out of sync on the value of physical stores, Klarna warns.’ Available at: https://www.klarna.com/international/press/retailers-and-shoppers-out-of-sync-on-the-value-of-physical-stores-klarna-warns/. Accessed February 2026.

Pymnts, May 2025. ‘Going Global: How Payments Optimization Can Power an International Commerce Strategy.’ Available at: https://www.pymnts.com/tracker_posts/going-global-how-payments-optimization-can-power-an-international-commerce-strategy/. Accessed February 2026.

McKinsey, October 2024. ‘State of consumer digital payments in 2024.’ Available at: https://www.mckinsey.com/industries/financial-services/our-insights/banking-matters/state-of-consumer-digital-payments-in-2024. Accessed February 2026.

BCG, September 2025. ‘Moving Embedded Finance from Promise to Practice.’ Available at: https://www.bcg.com/publications/2025/moving-embedded-finance-from-promise-practice. Accessed February 2026.

The Paypers, March 2025. ‘Buy Now, Pay Later Report 2025.’ Available at: https://thepaypers.com/payments/reports/buy-now-pay-later-report-2025. Accessed February 2026.

Asug, December 2025. ‘Modernizing Payments Infrastructure: Embedded Finance, Automation, and Partner Value – Collaborative Research from ASUG and J.P. Morgan.’ Accessed February 2026.

Fortune, June 2025. ‘A growing number of Fortune 500 companies are pursuing ‘blockchain initiatives’ as crypto goes mainstream.’ Available at: https://fortune.com/crypto/2025/06/10/fortune-500-companies-pursue-blockchain-initiatives-crypto-mainstream/. Accessed January 2026.

The Block, October 2025. ‘State Street finds institutional investors eye doubling their digital asset exposure within three years.’ Available: https://www.theblock.co/post/374011/state-street-institutional-investors-digital-asset-exposure-to-double-within-three-years. Accessed January 2026.

J.P. Morgan Europe Equity Research

J.P. Morgan, ‘How Tokenization Can Fuel a $400 Billion Opportunity in Distributing Alternative Investments to Individuals.’ Available at: How Tokenization Can Fuel a $400 Billion Opportunity in Distributing AlternativeInvestments to Individuals. Accessed September 2025.

Member FDIC. Deposits held in non-U.S. branches are not FDIC insured. Non-deposit products are not FDIC insured. All rights reserved. The statements herein are confidential and proprietary and not intended to be legally binding. Not all products and services are available in all geographical areas. Visit jpmorgan.com/disclosures/payments for further disclosures and disclaimers related to this content.