- Centralizes treasury control by consolidating balances from multiple accounts into a master account.

- Reduces external borrowing and overdraft funding cost.

- Allows for increased efficiency by automatically investing excess cash.

- Reduces administrative burdens in managing intra-group entrust loans.

Staging the journey

With multinational corporates (MNCs) continuing to generate strong cash flows from China operations, the need for proper liquidity solutioning has never been greater—particularly for companies with multiple locally established entities in various stages of the enterprise life cycle. It has become mission-critical for these companies to achieve full cash visibility by centralizing domestic balances.

Domestic liquidity structures within China have been the de-facto option to achieve this, ranging from manual bilateral entrustment loan arrangements to fully automated multilateral cash sweep schemes.

"With multinational corporates continuing to generate strong cash flows from China operations, the need for proper liquidity solutioning has never been greater."

As China’s cross-border liberalization continues, the advancement of sweeping mechanisms has given treasurers flexibility to respond to changing needs and unique business models. This is evidenced in the evolution and acceptance of Dynamic Sequence Structures. Additionally, as policy has gradually relaxed, China-domiciled entities have become eligible to participate in cross-border liquidity structures, allowing idle cash balances to join global cash pools to facilitate overseas funding requirements.

China’s liquidity evolution: Sweeping mechanisms

- Centralizes treasury control by consolidating balances from multiple accounts into a master account.

- Reduces external borrowing and overdraft funding cost.

- Increases efficiency by automatically investing excess cash.

- Comparative cost savings arising from the entrust loan interest income.

- Centralizes treasury control by consolidating balances from multiple accounts into a master account.

- Reduces external borrowing and overdraft funding cost.

- Increases efficiency by automatically investing excess cash.

- Comparative cost savings arising from the entrust loan interest income.

- Reduce external borrowing and overdraft funding costs.

- Meet requirements of decentralized group structure for individual cashflow control.

- Highest potential cost savings arising from the entrust loan interest income.

Preparing for a successful implementation

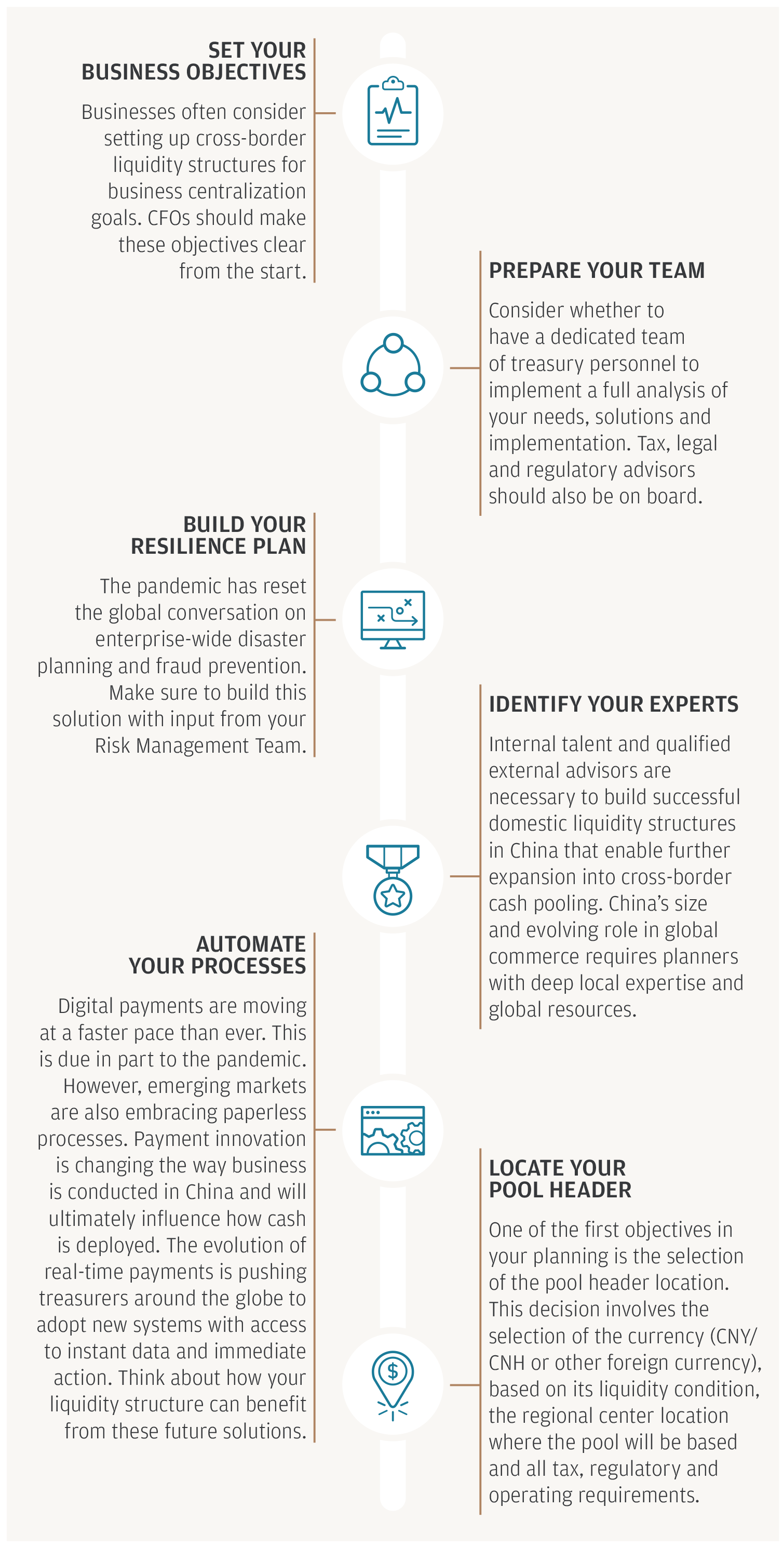

MNCs should plan at least a year in advance in order to identify new liquidity models and what financial, legal and IT upgrades may be necessary. During this process, consider how you will:

SET YOUR BUSINESS OBJECTIVES—Businesses often consider setting up cross-border liquidity structures for business centralization goals. CFOs should make these objectives clear from the start.

PREPARE YOUR TEAM—Consider whether to have a dedicated team of treasury personnel to implement a full analysis of your needs, solutions and implementation. Tax, legal and regulatory advisors should also be on board.

BUILD YOUR RESILIENCE PLAN—The pandemic has reset the global conversation on enterprise-wide disaster planning and fraud prevention. Make sure to build this solution with input from your Risk Management Team.

IDENTIFY YOUR EXPERTS—Internal talent and qualified external advisors are necessary to build successful domestic liquidity structures in China that enable further expansion into cross-border cash pooling. China’s size and evolving role in global commerce requires planners with deep local expertise and global resources.

AUTOMATE YOUR PROCESSES—Digital payments are moving at a faster pace than ever. This is due in part to the pandemic. However, emerging markets are also embracing paperless processes. Payment innovation is changing the way business is conducted in China and will ultimately influence how cash is deployed. The evolution of real-time payments is pushing treasurers around the globe to adopt new systems with access to instant data and immediate action. Think about how your liquidity structure can benefit from these future solutions.

LOCATE YOUR POOL HEADER—One of the first objectives in your planning is the selection of the pool header location. This decision involves the selection of the currency (CNY/CNH or other foreign currency), based on its liquidity condition, the regional center location where the pool will be based and all tax, regulatory and operating requirements.

Depending on the options, scope and complexity of the cross-border liquidity model you choose, it usually takes three to six months from planning to implementation, including China’s regulatory approval process. The timeline will also depend on whether your company already benefits from the experience of an established liquidity structure elsewhere in the group.

Navigating the regulatory landscape

There are currently two governing bodies that monitor cross-border physical cash pooling in China. PBOC (People’s bank of China) manages the CNY cross-border scheme and SAFE (State Administration of Foreign Exchange) manages a separate multi-currency scheme that includes FCY and CNY.

The two governing bodies have set forth specific criteria and eligibility standards for pool participants and it’s on a case-by-case pre-regulatory approval and filing basis to set up the cash pool subject to applicable regulations, excluding the Shanghai Free trade zone scheme.

China has been gradually easing controls on capital accounts to incentivize multinational corporations to invest in local business and take local firms global. In and outbound capital flow rules have been relaxed, creating opportunities for businesses to utilize working capital more efficiently in ways which were previously inaccessible.

But as all things ebb and flow, rules and conditions are constantly evolving.

Getting the execution right

Perhaps nothing is as important than picking an experienced transaction bank with a track record of navigating the market. Recently, a leading chemical company was seeking innovative and cost-effective solutions to help them manage their resources to promote efficiency in their crop yield and quality control processes. The client’s Asia Pacific operations spanned across 14 markets and contributed 25 percent of global revenue. The client’s objectives were to:

- Mobilize CNY liquidity between China and global regions and minimize FX costs currently incurred.

- Centralize liquidity to maximize yield with intercompany reporting to track positions.

- Implement a flexible solution that allows for additional entities to participate in the future.

In collaboration with J.P. Morgan, the client implemented a structure that only required one China onshore entity to participate in a CNY cross-border pool (typical engagements require a domestic cash pool to have a minimum of two entities).

The client was able to mobilize trapped cash with only one onshore entity with the flexibility to effectively fund two offshore entities. Idle balances were released in participating countries through Singapore to fund regional working capital needs. The client was additionally able to minimize FX conversion costs and offset short positions by leveraging an aggregate pool balance.

Looking ahead

As the Chinese market continues to liberalize and new treasury innovations become increasingly accessible and accepted, the way cash is managed is set to undergo a dramatic transformation. Centralization, flexibility and automation are top-of-mind for corporate treasurers doing business in China now more than ever. The evolution and proliferation of sweeping mechanisms and digitalization of transactions is just the beginning. The adoption of real-time-payments is accelerating treasurers towards a cohesive “real-time treasury” mindset and the toolbox to match.

This calls for the right transaction banking relationship—one that builds on the modern treasurer’s mandate with a digitally-driven, human-first approach.

This calls for the right transaction banking relationship—one that builds on the modern treasurer’s mandate with a digitally-driven, human-first approach. We are proud to continue to support our global multinational clients with their global liquidity needs through thoughtful expertise, detailed knowledge of the landscape, and ideas to help them win.

To learn more about our growing suite of solutions for your cross-border liquidity challenges, please contact your J.P. Morgan representative.

This material was prepared exclusively for the benefit and internal use of the JPMorgan client to whom it is directly addressed (including such client’s subsidiaries, the “Company”) in order to assist the Company in evaluating a possible transaction(s) and does not carry any right of disclosure to any other party. In preparing this material, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Company or which was otherwise reviewed by us. This material is for discussion purposes only and is incomplete without reference to the other briefings provided by JPMorgan. Neither this material nor any of its contents may be disclosed or used for any other purpose without the prior written consent of JPMorgan.

J.P. Morgan, JPMorgan, JPMorgan Chase and Chase are marketing names for certain businesses of JPMorgan Chase & Co. and its subsidiaries worldwide (collectively, “JPMC”). Products or services may be marketed and/or provided by commercial banks such as JPMorgan Chase Bank, N.A., securities or other non-banking affiliates or other JPMC entities. JPMC contact persons may be employees or officers of any of the foregoing entities and the terms “J.P. Morgan”, “JPMorgan”, “JPMorgan Chase” and “Chase” if and as used herein include as applicable all such employees or officers and/or entities irrespective of marketing name(s) used. Nothing in this material is a solicitation by JPMC of any product or service which would be unlawful under applicable laws or regulations.

Investments or strategies discussed herein may not be suitable for all investors. Neither JPMorgan nor any of its directors, officers, employees or agents shall incur in any responsibility or liability whatsoever to the Company or any other party with respect to the contents of any matters referred herein, or discussed as a result of, this material. This material is not intended to provide, and should not be relied on for, accounting, legal or tax advice or investment recommendations. Please consult your own tax, legal, accounting or investment advisor concerning such matters.

Not all products and services are available in all geographic areas. Eligibility for particular products and services is subject to final determination by JPMC and or its affiliates/subsidiaries. This material does not constitute a commitment by any JPMC entity to extend or arrange credit or to provide any other products or services and JPMorgan reserves the right to withdraw at any time. All services are subject to applicable laws, regulations, and applicable approvals and notifications. The Company should examine the specific restrictions and limitations under the laws of its own jurisdiction that may be applicable to the Company due to its nature or to the products and services referred herein.

Notwithstanding anything to the contrary, the statements in this material are not intended to be legally binding. Any products, services, terms or other matters described herein (other than in respect of confidentiality) are subject to the terms of separate legally binding documentation and/or are subject to change without notice.

Changes to Interbank Offered Rates (IBORs) and other benchmark rates: Certain interest rate benchmarks are, or may in the future become, subject to ongoing international, national and other regulatory guidance, reform and proposals for reform. For more information, please consult: https://www.jpmorgan.com/global/disclosures/interbank_offered_rates.

JPMorgan Chase Bank, N.A. Member FDIC.

JPMorgan Chase Bank, N.A., organized under the laws of U.S.A. with limited liability.