Globally, the way we shop, work, travel, socialize and access services - among many other facets of daily life - has been overturned during the past two years. This is reshaping the payments industry in myriad ways. A reassessment of our priorities is inevitable in the aftermath of a transformational event, and in the payments industry it is no different.

As global economies recover from the struggles of the pandemic, we are set to enter a new phase in the payments industry. If 2021 was about making businesses as robust and resilient as possible, then the focus for the next 18 months is likely to be on sustainable growth, powered by digital technology.

Different regions are at different stages of digital maturity, just as different industries are at different stages of disruption. J.P. Morgan’s FastForward virtual forums have identified the five overarching trends – regardless of region – that we believe will influence how businesses across all industries position themselves for growth for the year ahead. We explore these trends and the role of payments in bringing these trends to life.

Digital as a culture

Working capital and liquidity have always and will continue to be a key focus for Finance and Treasury professionals regardless of the size of their company. As working patterns and supply chains evolve in the wake of the pandemic, businesses may have to adjust their own working capital and liquidity strategies to help ensure they can handle the new normal and their businesses’ growth strategies.

For businesses, the pandemic has made the acceleration of digital projects a necessity, not a choice, and this will continue as consumers and businesses alike have become increasingly aware of the conveniences and opportunities that digital services can provide.

From an infrastructure standpoint, there is a clear shift towards a ‘holistic digital’ approach. Whether they are financial institutions, B2C or B2B companies, or even government agencies, many businesses are trying to ensure that they have the right digital ecosystem in place for the customers they serve.

Companies that are earlier in their digitization journey are at what we call the ‘discovery’ stage and have been pushed into digitization over the past few years. This is creating a mindset shift within smaller and medium-sized businesses. Rather than try and solve individual and siloed issues, or digitize a discrete piece of their business to make it less paper-oriented, smart businesses are asking instead, 'How do we think about our business as a whole and how do we enable it with technology?'

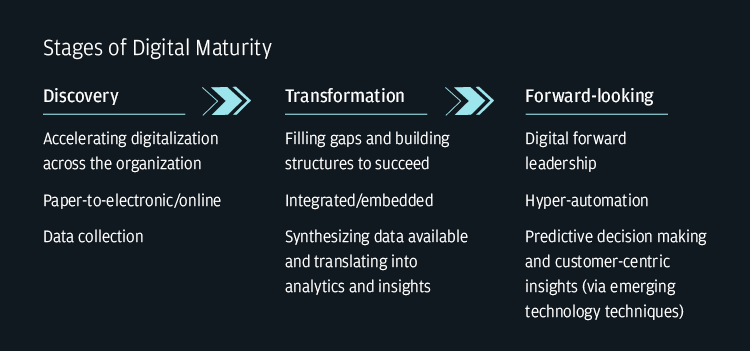

Stages of digital maturity

1. Discovery

Accelerating digitalization across the organization

Paper-to-electronic/online

Data collection

2. Transformation

Filling gaps and building structures to succeed

Integrated/embedded

Synthesizing data available and translating into analytics and insight

3. Forward-looking

Digital forward leadership

Hyper-automation

Predictive decision making and customer-centric insights (via emerging technology techniques)

Then there are those at the ‘transformation’ stage: many of J.P. Morgan’s clients are embarking on bigger technology projects, such as enterprise resource planning (ERP) rollouts to standardize processes across their organization. They are implementing new solutions that automate their cash processes, whether it is payables, receivables or treasury. Crucially, they are leaning on their banking partners and talking to players in the fintech market in order to find digital solutions to problems that they have not been able to solve for decades.

Businesses that were ahead of the curve with digitization – or were digital natives to begin with – found themselves in the strongest position during the pandemic, and will continue to enjoy first-mover advantage going forward. We call these the ‘visionaries’, and these businesses are now exploring and integrating advanced technologies into their offerings, such as AI, predictive decision-making or blockchain. We are seeing Financial institutions in this stage creating digital ecosystems, forming strategic partnerships between banks, fintechs and insurance companies. To fully exploit these relationships, Financial Institutions need to think beyond the headlines, to deliver a truly integrated experience to their clients who can be institutions or every day consumers.

Asia Pacific (APAC) is the regional leader in digital-as-a-culture1. QR code-based, contactless and digital payments are at their highest penetration in this region2. This is because many countries went straight from cash to digital, skipping the debit/credit card phase. APAC is also the home of super-apps like Wechat and Alipay, that have mastered the integration of multiple digital and physical services, including payments, within a single platform. We are seeing this movement gain momentum in other regions, especially the Americas. Many businesses have expanded during the pandemic and are branching out into new areas to create their own ecosystem. For example, in Latin America, Rappi started as a delivery app, but is moving into offering financial services to build the foundation of its ecosystem.

Europe, Middle East and Africa (EMEA) is also an advanced region for digital-as-a-culture, which often translates as a ‘go-to’ market. But in EMEA, visionary businesses are also leveraging their digital data and analytics on their customers to predict spending patterns, including certain types of sales growth – or lack thereof – and so they can really pivot and hone their marketing strategies.

The best strategy we’ve seen across organizations wanting to master digital as a culture is to ensure digitalization permeates and improves every aspect of your infrastructure and customer strategy. In other words, make digital a part of your business’ DNA.

Anything-as a-Service

Think of a super-app like Grab in APAC – they started like Uber, offering users the ability to book a ride home, but have since grown to allow users to order a meal to eat at home, buy travel insurance, or to pay for goods and service using Grab’s proprietary digital wallet – GrabPay – on a single platform.

As consumers and businesses alike look for increasing personalization, flexibility and convenience in the goods & service they want, as-a-service models will continue its growth. The growth of As-a-Service models is seven times the growth of traditional companies3 because of the efficiencies they create. As they grow, they are able to create cohesive ecosystems on easy-to-use platforms, knitting different niche solutions together. According to McKinsey, 71% of consumers are ready for ecosystem offerings.4

As many companies pivot to the ecosystem and ‘platform of platforms’ models by bringing the different as-a-service models together, payments become the essential connective tissue. Payments-as-a-service and Banking-as-a-service models are increasing in demand, especially as businesses are looking to offer financial services solutions to their clients to amplify their loyalty. For instance, creating a digital wallet to make a marketplace ecosystem more stick to buyers and sellers.

As-a-service models also help to open doors to new revenue opportunities for many industries and are changing the way they engage with clients. For instance, large financial institutions are expanding their offerings by providing banking or payments as a service to their clients. They are leveraging existing relationships to allow their clients to compete in new markets. In other industries, this might create a usership economy from the historic ownership models – like how streaming did for entertainment, and how some automakers are creating a subscription option alongside their traditional purchasing option, opening doors to a new demographic and market. For some companies, this is also a way to venture into a new business – for instance, from a traditionally hardware based company to a software based new business, like we’ve seen in the technology industry in the last decade, and are seeing in industrials and energy space now.

As companies look to pivot their business models or to open new revenue streams, increasing as-a-service models have the potential to become the vehicle of choice.

Payments as a revenue driver

Payments are evolving from a necessary part of a business to a component which actively adds value and appeal to consumers and supply chains. Many companies are now viewing payments as a way to differentiate themselves from the competition, to improve the user experience and to generate revenue.

Payments are now directly a contributor to top-line growth – this is partly being driven by the aforementioned rise of subscriptions, where an increasing number of companies are migrating into either direct-to-consumer or subscription-based models, and payments are not only critical levers to enable those pivots but also are key to helping ensure operational efficiency once the pivots are made. These businesses are now tasked with asking, 'How do I facilitate a better experience for my customers – without sacrificing the efficiency of my back office, when we now have many more transactions than before going through our system?'

As companies change their offerings and change the way they operate within the market, they're leveraging payments to help drive differentiation. Another example is the ability to go direct-to-consumer, which can be transformative for brands and business-to-business firms. This is only possible if they can build-out their own consumer-based payment infrastructure.

Payments are helping to drive their top-line growth not only through their customers, but also through their suppliers and their vendors. Particularly with ongoing supply chain disruptions, companies are partnering more with their suppliers and their vendors to come up with payment terms and payment methods that work beneficially for both parties. In a supply-constrained market, suppliers currently hold a lot of power, because they can prioritize or de-prioritize businesses according to the terms they’re offered.

For businesses that have flexible or ‘gig economy’ workers, giving employees access to their funds in a real-time manner can now also make a huge competitive differentiator. If your business is competing with others for talent, your ability to pay once the task – whether that’s a ride or a food deliver, as an example – is completed versus the regular bi-weekly pay cycle may well be the benefit which makes a worker choose your company over a rival. This is a trend that is being seen strongly in North America.

APAC remains the global leader in real-time payments, with India and China together accounting for approximately 60% of real-time transactions in 2020.5Companies with the analytical tools in place are taking advantage of the real-time transactions to generate real-time data analytics for better customer engagement and to identify operational issues.

Aligning working capital & liquidity

Working capital and liquidity have always and will continue to be a key focus for Finance and Treasury professionals regardless of the size of their company. As working patterns and supply chains evolve in the wake of the pandemic, businesses may have to adjust their own working capital and liquidity strategies to help ensure they can handle the new normal and their businesses’ growth strategies.

Adding to the challenge for corporates is to readjust and normalize the disrupted working capital cycles and balancing of the increased cash buffers from the last two years while managing the continued supply chain disruption. As the economy recovered and demand increases, many businesses have not been able to build up their inventories back to pre-pandemic levels. The disruptions and delays will likely continue through 2022, especially across Europe and North America (who bore the brunt of the delays) 6. As businesses evaluate their working capital and liquidity strategies, they will not only need to think about their supply chain strategy to mitigate the disruption, but also the needs of their business for organic and inorganic growth.

Best practices have seen treasurers focus on visibility, agility, and resilience; gaining visibility and access through centralization, such as shared service centers and automation of the liquidity management. Bolstering resilience not only means forecasting and stress-testing working capital scenarios, but also focusing on the stabilization of the supply chain and key suppliers.

Supply chain strategy plays a large role as part of this stabilization – in two ways. First, moving away from one-size-fits-all strategies and band-aid solutions put in place for the last two years to a targeted strategy. For example, for businesses with many smaller suppliers, meeting their increased demand for short-term corporate lending, such as commercial cards and supply chain financing to help improve their suppliers’ liquidity and bolster the health of suppliers.

Second, considering the regional diversification of supply chain, especially given the continued geopolitical tension and the continued delays. This is leading some to consider regionalization and shift away from centralized liquidity hubs to better support new supply chain. Rather than base everything in cities such as London, New York or Singapore, we are seeing more regionalization, in an effort to open up multiple cash pools.

Another factor driving the need for access to diverse sources of capital is the sharp growth in mergers, acquisitions, and divestitures. In 2021, global M&A deals shattered records according to Dealogic. M&A was viewed as key growth strategy, especially to acquire technology and innovative models / solutions, but also as a way to refocus the business through divestitures and spin-offs. This is only set to continue throughout 2022.

Technology (especially in the Buy-Now-Pay-Later space), fintechs and healthcare are among the most active sectors7– which is perhaps unsurprising, as these areas became even more prominent in 2020 and 2021, and are continuing to evolve rapidly and maintain their relevance today. Acquiring technology which will enable businesses to best serve their clients is a key theme driving many acquisitions, to make digital a core part of their future growth and value.

As organizations re-evaluate their working capital and supply chain strategies, consider the alignment with the supply chain strategy, future M&A or divestitures, and growth plans to help ensure not only access to sufficient capital but also visibility into and flexibility to shift as needed.

Building an ESG strategy for your business

The concept of environmental, social and governance (ESG) and its potential for positive impact on businesses was introduced in a landmark 2005 study named ‘Who Cares Wins.8Seventeen years later, the study’s thesis is being borne out around the globe: the share of sustainably invested assets among investors worldwide was 18% in 2020, a figure that is set to more than double to 37% by 2025.

ESG considerations have become mainstream and at the core of corporate strategy. The Great Resignation has been one of the biggest shifts of the pandemic in Western markets – and it is still ongoing. With record numbers of people leaving jobs which no longer align with their needs and values,9 companies have to work harder than ever to attract and retain talented people. It’s worth noting, too, that resignation rates are highest among the technology and healthcare sectors10 – the sectors which, as we mentioned earlier, are seeing some of the highest rates of M&A activity.

In 2022, businesses that rely on tech talent will have to ensure they can offer what employees are flexibility, a sense of purpose, adequate healthcare and compensation.

Meanwhile, consumers are demanding more transparency from companies about their products and services, to ensure that they are ethically sourced and respect workers’ rights. Annual sales of sustainable-marketed products are set to reach US$140.5 billion in 2023.11

The different aspects of ESG have varying weight and importance in different geographies. In Europe, for example, environmental factors tend to be viewed as the most important, whilst US firms are focusing more on social factors, like diversity, equity, and inclusion. In APAC, China has announced a Net Zero 2060 target and ESG disclosures for listed companies are starting to become the norm in Singapore & Hong Kong. Even different countries within a region have different priorities: for example, Malaysia and Indonesia’s environmental concerns focus on rainforest preservation and palm oil, whereas in Australia, mining and water and energy resources are highly relevant. As ESG varies across regions, approaches also vary by industry. Institutions responsible for financing ESG initiatives will play a critical role in their success or failure. The weight on the shoulders of Financial Institutions will be heavy and they must navigate the way forward thoughtfully.

Around the globe, regulations are coming which will further the ESG agenda. In Europe, the new EU Sustainable Finance Disclosure Regulation will see disclosure requirements becoming tougher, to ensure investors can compare the sustainability profile of different investments more clearly. In APAC, the IMF and the World Bank are among those running the Global Challenge for Retail CBDC, to promote financial inclusion and payment efficiencies. Globally, world leaders came together at the end of 2021 for the United Nations Climate Change Conference (COP26) to strategize on global action that can be taken to address the climate crisis.

It’s clear that consumers, regulators, and businesses are now taking ESG seriously. Who cares, wins.

‘Digital first’ approach for payments

As payments evolve into a key differentiator and revenue driver, they can no longer be an afterthought, or exist in the background. Payments need to be front and center of your business strategy, and powered by digital innovations to help prepare your Treasury for the future.

In our fast-moving, unpredictable global environment, staying ahead of the latest developments in digital treasury, payments technology and cultural shifts is vital for business to succeed. J.P. Morgan is a global leader in payments processing and technology, equipping our clients with the knowledge, services and tools they need to prosper in these challenging times. For more information, contact your local J.P. Morgan representative.

Missed our recent FastForward webinar series? Listen to the playback here

Stay informed and stay ahead with our monthly newsletter

Receive key updates and news with relevant actionable insights and best practices — including the latest intelligence on payments trends, digital innovation, regulatory change, ESG and sustainable financing and much more.

References

McKinsey, October 2021. ‘The 2021 McKinsey Global Payments Report.’ Accessed February 2022

Mastercard, May 2021. ‘Mastercard New Payments Index.’ Accessed February 2022

Zuora Subscription Index 2021

McKinsey Digital Insights 2020

BFSI.com, ‘Real-time Payment transactions witness 41% surge in 2020: ACI Worldwide.’ Available at:

IHS Markit, July 2021. ‘Understanding … PMI suppliers' delivery times: A widely used indicator of supply delays, capacity constraints and price pressures.’ Accessed February 2022.

Dealogic, December 2021.

Harvard Business School, September 2021. ‘Who is Driving the Great Resignation.’ Accessed February 2022

Transformative Mega Trends shaping Post-COVID Consumer behaviour by Frost and Sullivan

MNP, February 2021. ‘Building a competitive edge through ESG.’ Accessed February 2022

weforum.org, November 2021. ‘What is 'The Great Resignation'? An expert explains.’ Accessed February 2022.

Harvard Business School, September 2021. ‘Who is Driving the Great Resignation.’ Accessed February 2022

Transformative Mega Trends shaping Post-COVID Consumer behaviour by Frost and Sullivan

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of J.P. Morgan, its affiliates, or its employees. The information set forth herein has been obtained or derived from sources believed to be reliable. Neither the author nor J.P. Morgan makes any representations or warranties as to the information’s accuracy or completeness. The information contained herein has been provided solely for informational purposes and does not constitute an offer, solicitation, advice or recommendation, to make any investment decisions or purchase any financial instruments, and may not be construed as such.

JPMorgan Chase Bank, N.A. Member FDIC.

JPMorgan Chase Bank, N.A., organized under the laws of U.S.A. with limited liability.