Utility companies typically collect payments from their customers. But when utilities need to make payments back to their customers, it may be to resolve an overpayment, return security deposits, pay damage claims or rebates, send efficiency bonuses or help with disaster recovery. And with payments still mainly being made manually by check, it’s a labor-intensive responsibility that may create a poor customer experience for the end-user. It also requires customer support teams to service any queries about the payments.

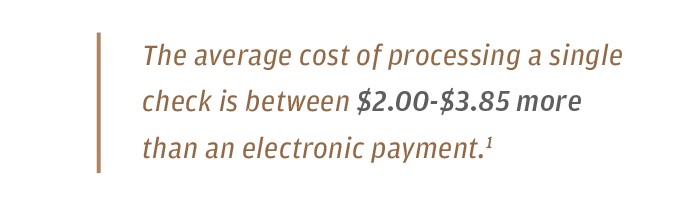

Considering the average cost of processing a single check is between $2.00-$3.85 more than an electronic payment, it’s also costly.1 The average-sized utility can send thousands of checks a month, and the costs start to stack up. Additionally, uncashed checks can create escheatment reporting burdens for utilities, which can be costly and time-intensive to resolve.

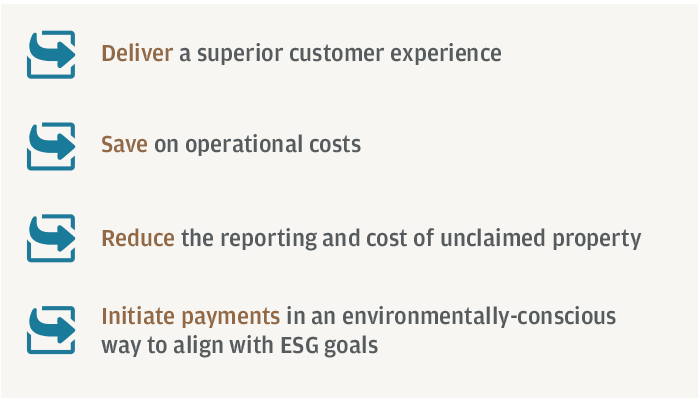

As a result, utilities have a unique opportunity to shift to digital payments. This approach can help them:

As a result, utilities have a unique opportunity to shift to digital payments. This approach can help them:

- Deliver a superior customer experience

- Save on operational costs

- Reduce the reporting and cost of unclaimed property

- Initiate payments in an environmentally-conscious way to align with ESG goals

The average cost of processing a single check is between $2.00-$3.85 more than an electronic payment.1

Digital Platforms Offer Wider Range of Payment Methods

Whether buying a product, resolving an issue, purchasing groceries or ordering a ride home, customers now expect to access the services they need online. For many customers, paper checks are now an antiquated payment method. Waiting for a check to arrive, then physically taking it to the bank and waiting for it to clear, represents an unacceptable amount of time and friction for consumers used to sending and receiving money instantly with their smartphone.

By switching to a digital platform, utilities can offer a wide range of convenient payment methods, based on their customers preferences—whether that’s ACH, RTP, PayPal, Venmo, Zelle, prepaid card or their smartphone’s online banking app. It also gives customers access to 24/7 support. A customer with a query can easily resolve it via information and support services on the portal or utility’s app, rather than being required to sit on a phone line during business hours. Reducing the need for phone calls to service centers helps drive down service costs and helps improve customer satisfaction. There is also the potential for further digital transformation and enhanced customer loyalty opportunities.

Save More, Improve Your ESG Ratings

Every cost counts for the regulated utilities industry. Eliminating or at least significantly reducing check usage is an opportunity to create operating efficiencies and reduce costs, which can then be reinvested into the business and community.

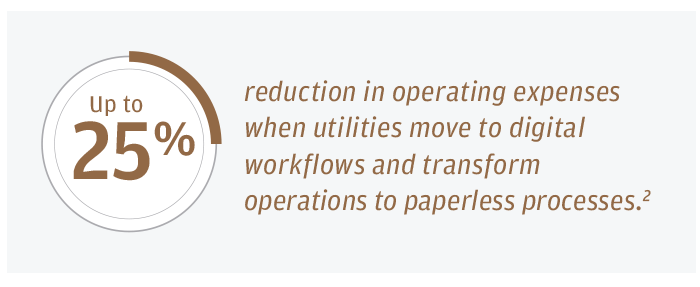

Moving to digital workflows and transforming operations to paperless processes can reduce utility operating expenses by up to 25 percent.2 Digital payments can help drive this reduction.

Up to 25 percent reduction in operating expenses when utilities move to digital workflows and transform operations to paperless processes.2

Additionally, digitalization creates an opportunity for utilities to add capital investments in technology to their rate base—the value of property on which a public utility is permitted to earn a specified rate of return. Prudent cost management may also help demonstrate good stewardship of customer prices to regulators.

It’s also important to recognize that checks are paper-intensive and generate carbon via postal delivery. For example, according to calculations from International Post Corporation (IPC), on average sending a single letter generates 40.1 grams of CO2.3 High paper usage is fast becoming untenable in a climate where both regulators and customers are asking tougher questions of companies’ environmental efforts.

Reduce Unclaimed Property—and Heighten Security

Unclaimed property, including uncashed checks must be reported to the local state, which creates a heavy administrative and cost burden for utilities.

Digital payment platforms resolve this by ensuring reimbursements go immediately to the person it’s intended for. Checks no longer sit on doormats or desks, waiting to be cashed; real-time online payments mean both the utility and their customers know the exact status of their money. Unclaimed property and escheatment burdens are greatly reduced by offering digital payment options to customers.

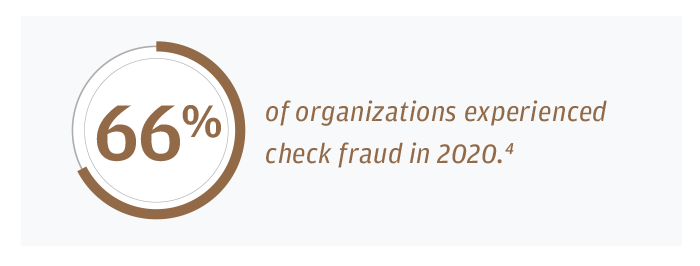

As a mail and paper-based payment method, checks are also frequently exposed to delays and fraud. In fact, 66 percent of organizations experienced check fraud in 2020.4 For both utilities and customers, accessing accounts via digital portals inherently reduces fraud risk as such devices and channels require passwords and multi-factor authentication. All information flows can be closely tracked and audited. Utilities also benefit from being removed from the need to secure customer data, and can instead lean on their payment partner’s banking industry-grade cybersecurity.

Sixty-six percent of organizations experienced check fraud in 2020.5

Moving Forward on the Path to Digital Transformation

Customers now expect frictionless interactions with their utilities, in the same way that they can handle an insurance claim pay-out from their laptop, order from their favorite restaurant via smartphone, or pause their monthly subscription services at the tap of a button.

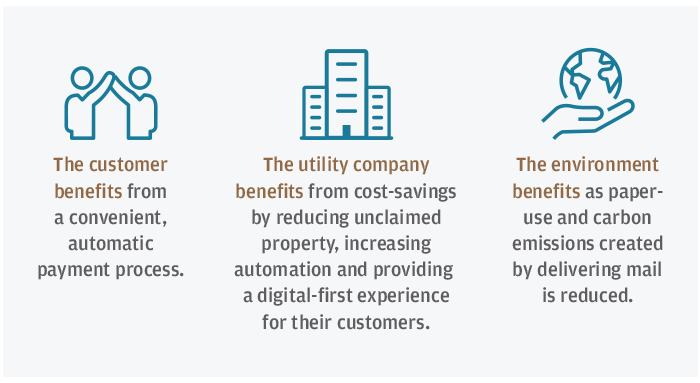

For utilities, payment digitization is how these customers’ expectations can be met. It’s a win-win-win scenario:

- The customer benefits from a convenient, automatic payment process.

- The utility company benefits from cost-savings by reducing unclaimed property, increasing automation, and providing a digital-first experience for their customers.

- The environment benefits as paper-use and carbon emissions created by delivering mail is reduced.

Our industry experts have served the U.S. utility industry for over a century. Leveraging our deep understanding and experience of the market, we constantly move with the times in order to provide market-leading digital solutions for our clients.

Our digital payments solution helps remove the need for paper checks, giving choice and support to the end customer and empowering utilities with best-in-class online payments functionality.

Connect with your J.P. Morgan representative to move towards digital payments.

References

“The Hidden Costs of Cheques For Your Business,” Finextra, February 2019. https://www.finextra.com/blogposting/16747/the-hidden-costs-of-cheques-for-your-business#:~:text=According%20to%20Payments%20Canada%2C%20cheques,cheque%20printing%20and%20mailing%20costs

“The Digital Utility: New challenges, capabilities and opportunities,” McKinsey & Company, June 2018. https://www.mckinsey.com/~/media/McKinsey/Industries/Electric%20Power%20and%20Natural%20Gas/

Our%20Insights/The%20Digital%20Utility/The%20Digital%20Utility.ashx

“Sustainability,” International Post Corporation. https://www.ipc.be/sector-data/sustainability

“2021 AFP Payments Fraud and Control Survey Report,” Association of Financial Professionals, 2021. https://www.jpmorgan.com/content/dam/jpm/commercial-banking/documents/fraud-protection/2021-afp-payments-fraud-and-control-survey-report-highlights.pdf

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of J.P. Morgan, its affiliates, or its employees. The information set forth herein has been obtained or derived from sources believed to be reliable. Neither the author nor J.P. Morgan makes any representations or warranties as to the information’s accuracy or completeness. The information contained herein has been provided solely for informational purposes and does not constitute an offer, solicitation, advice or recommendation, to make any investment decisions or purchase any financial instruments, and may not be construed as such.

JPMorgan Chase Bank, N.A. Member FDIC.

JPMorgan Chase Bank, N.A., organized under the laws of U.S.A. with limited liability.