Turning the tide:

Revitalizing the

US shipbuilding

industry

With the U.S. shipbuilding industry experiencing a multi-decade

decline, a sea change is needed, especially in light of growing

national security concerns.

Turning the tide:

Revitalizing the

US shipbuilding

industry

With the U.S. shipbuilding industry experiencing a multi-decade

decline, a sea change is needed, especially in light of growing

national security concerns.

May 01, 2026

Yet less than 1% of the global fleet is U.S.-flagged. Instead, the vast majority is handled by European or Asian operators, predominantly using Asian-built ships.

This is largely due to limited shipbuilding capacity. While the U.S. dominated global shipbuilding during the two world wars, production declined after the Second World War ended, and it quickly lost market share to Asian peers. Today, the U.S. has 190 flagged merchant vessels, many of which were built abroad; in contrast, China has more than 7,000.

“This reliance on foreign ships and shippers isn’t necessarily a problem. Global trade thrives on countries specializing in what they do best, boosting efficiency and prosperity for all,” observed Jahangir Aziz, co-head of Economic Research at J.P. Morgan. “But the pandemic, the Russia–Ukraine war, rising tensions with China, and now conflict in the Middle East have all laid bare the vulnerabilities in U.S. supply chains. If access to ships were suddenly cut off, the damage to the U.S. economy would be severe.”

US trade by the numbers

$5.6T

The U.S.’s annual goods imports and exports total $5.6 trillion.

1%

Currently, less than 1% of the global merchant fleet is U.S.-flagged.

190

The U.S. only has 190 flagged merchant vessels, many of which were built abroad.

“The pandemic, the Russia–Ukraine war, rising tensions with China and now conflict in the Middle East have all laid bare the vulnerabilities in U.S. supply chains. If access to ships were suddenly cut off, the damage to the U.S. economy would be severe.”

Jahangir Aziz

Co-head of Economic Research, J.P. Morgan

This is because large commercial vessels can serve dual roles during national emergencies, supporting military operations and delivering essential aid. “Currently, with a commercial fleet of fewer than 200 vessels over 1,000 tons, down from nearly 3,000 in the 1960s, the U.S. risks being unable to guarantee the flow of essential goods or respond effectively to a military crisis,” noted Alexander Wise, who is part of the Long-Term Strategy team at J.P. Morgan.

Then there are the economic benefits to consider. Increased commercial shipbuilding could reduce trade costs for the U.S. and improve supply chain efficiency, in turn boosting economic activity. It could also promote innovation and R&D on a wider scale, with positive spillovers for the rest of the economy.

To this end, the U.S. government has acknowledged the need to rebuild its maritime industrial base to enhance military readiness and economic prosperity. The bipartisan Shipbuilding and Harbor Infrastructure for Prosperity and Security (SHIPS) for America Act was reintroduced on April 2025, with the goal of increasing the U.S.-flagged fleet by 250 ships within the next decade.

Then, in February 2026, the Trump administration launched a broader framework called the Maritime Action Plan. Key elements of the plan include bolstering investment in shipyards, streamlining regulatory processes and reforming workforce training, which could help reverse the long-term decline in U.S. shipbuilding.

This is especially as building ships is a complex process requiring strong organizational expertise, significant capital infrastructure and diverse supplier networks.

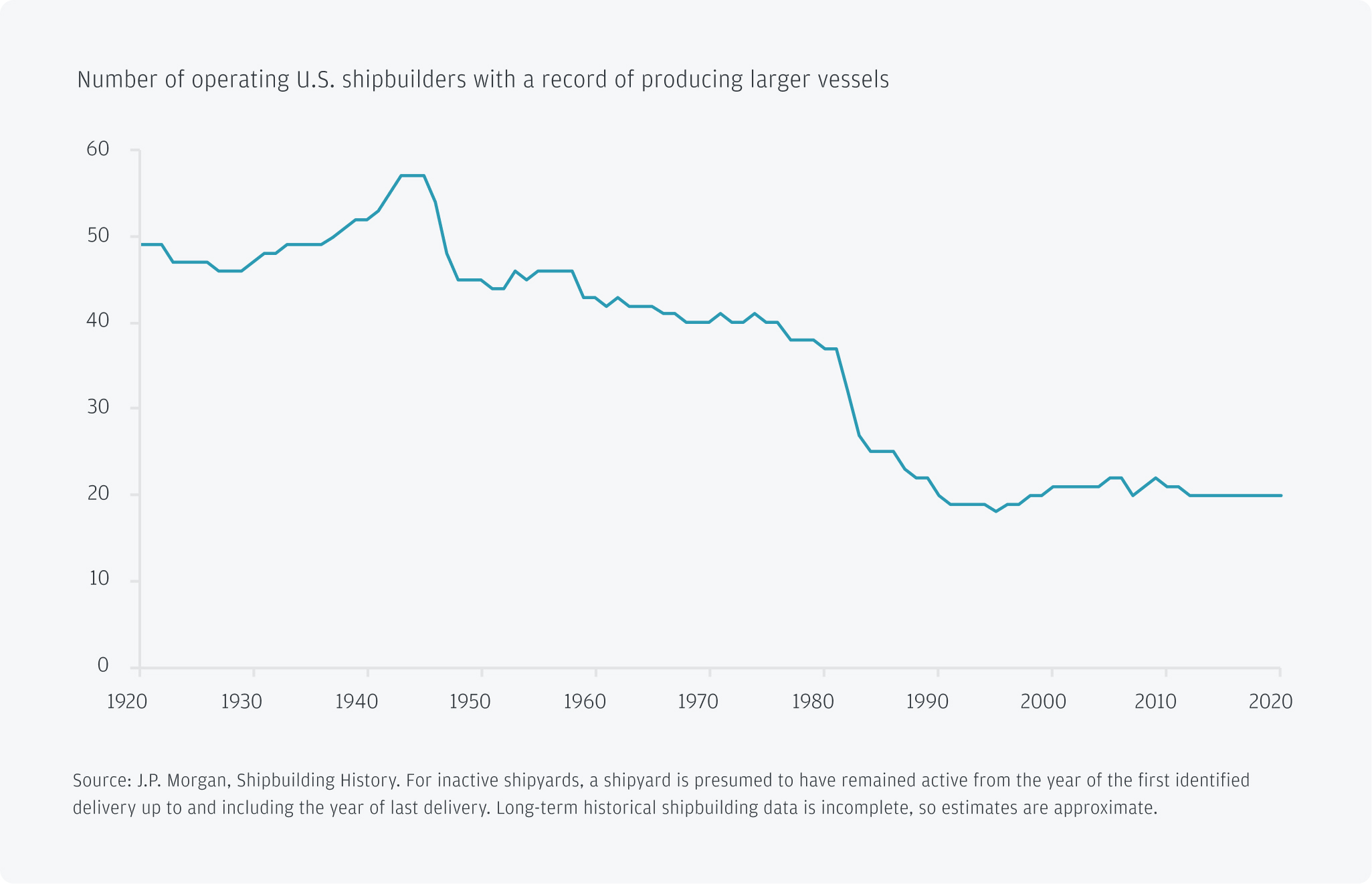

US shipbuilders are declining

The number of operating U.S. shipbuilders with a record of producing larger vessels has declined since the 1940s.

“Overall, by delivering on these fronts, the U.S. can build a resilient maritime industrial base, reduce strategic vulnerabilities and reclaim a competitive position in the global shipping landscape,” Aziz said.

JPMorganChase’s Security and Resiliency Initiative is a $1.5 trillion, 10-year plan to facilitate, finance and invest in industries critical to national economic security and resiliency. This includes a focus on shipbuilding and repair, advanced manufacturing and advanced bulk materials.

Related insights

Global Research

Oil prices have surged, and more volatility could be in store for markets as the conflict continues to unfold.

3:17 - Economy

What is a supply chain, how does it work and what happens when there are issues?

Global Research

The conflict has generated significant impacts far beyond energy markets, creating headwinds for sectors from agriculture to aviation.