The tough sanctions that have been imposed on Russia and the market volatility following its invasion of Ukraine on February 24 have hit the Russian economy hard, severely damaging its growth outlook and ability to trade and do business internationally. But the economic impact of the conflict will also be felt by people around the world, as the sharp rise in the price of commodities is expected to push up the cost of many everyday items from food to petrol and heating. In this report, J.P. Morgan Research looks at how Russia’s invasion of Ukraine is impacting gasoline and food prices for consumers.

Why is the price of gas going up?

The Russian invasion of Ukraine sharply increased global commodity prices, particularly for oil, sending the cost of crude oil and in turn, prices at the gasoline pump, soaring. Gas prices in the U.S. have averaged around 20% higher than where they were prior to the invasion on February 24. The implied additional dollar burden of higher gas prices, assuming no change in the quantity of gas consumed, is around $7 billion per month.

“This represents a non-trivial drag on consumer demand, first at the individual level given the direct compression in discretionary income and then from a societal vantage point, as the initial drag on consumption propagates and accumulates through the economy,” said Peter McCrory, U.S. Economist at J.P. Morgan Research.

Gas is an essential purchase for the majority of U.S. consumers, so demand for gas at the pump does not tend to dip initially when prices rise. Nominal spending at gas stations initially jumped alongside the spike in gas prices, even after accounting for pre-pandemic gas station spending patterns in March.

“After taking into account the modest reduction in gas volume consumption, we think the 20% spike in gas prices may be lowering nominal non-gas consumption by $9.6 billion per month—shaving 0.26% off of overall nominal consumption on an annualized basis, concentrated in the second quarter. Despite the buffer of excess savings, elevated gas prices nevertheless appear to be weighing on real consumption,” said McCrory.

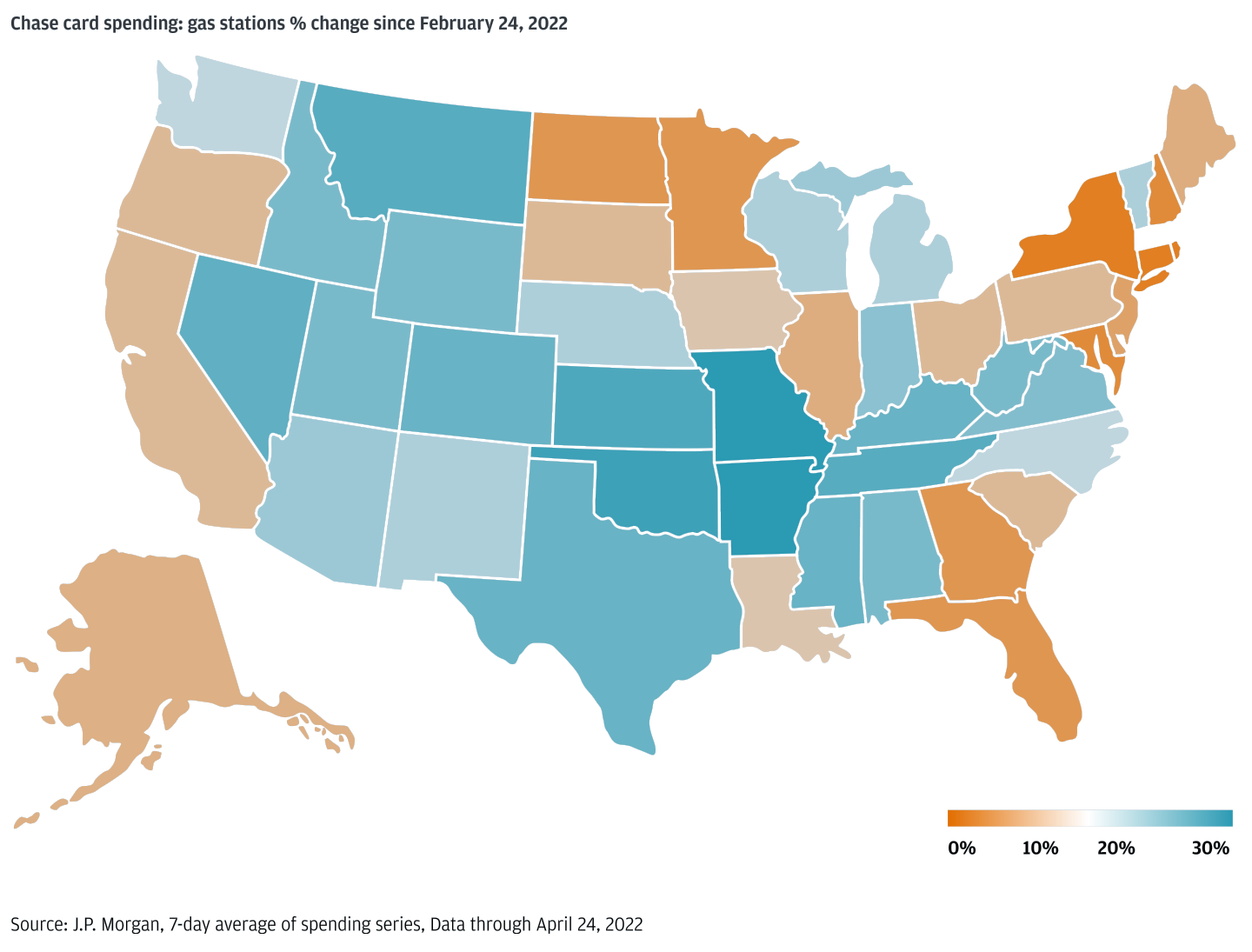

Chase card spending on gas since Russia's invasion

Chase card spending on gas rose in the majority of U.S. states between February 24 and April 24, 2022. It increased by more than 30% in Arkansas and Missouri, but by less than 10% in Connecticut, Massachusetts and New York.

J.P. Morgan analysis suggests that the effect of higher gas prices on consumption excluding gas takes some time to accumulate, with the drag from higher gas prices not clearly evident until two to three months following an increase. This means real consumer spending growth may be choppy in months to come.

“We estimate an aggregate excluding gas consumption multiplier of 1.6 from higher gas prices. This estimate implies that each $1 of additional spending on gasoline following a gas price spike lowers non-gas consumption by $1.6. Gasoline prices rise, consumers pay more for gas and pull back on non-gas spending,” said McCrory.

J.P. Morgan estimates, based on Chase card spending data, imply that nominal consumption falls by $.60 for each additional $1 of gasoline spending due to higher prices. Perhaps unsurprisingly, the states where gas consumption is larger as a share of overall consumption tend to exhibit less sensitivity to higher gas prices—a reminder that the effects of higher gas prices have distributional consequences as well, imposing greater hardship on those less able to adjust real gas consumption. Arkansas and Missouri have seen the largest increase in spending at gas stations since February, while spending in Connecticut, Massachusetts and New York increased the least, according to Chase data.

“The hit from higher gas prices is twofold for high-gas-consuming states. Not only do higher prices reduce real income by more than elsewhere, such states appear to be less able to offset higher prices by reducing real demand,” added McCrory.

Will gas prices keep rising?

Oil prices are down from the record highs seen shortly after the invasion, where the Russian supply risk shot prices towards $130 per barrel (bbl) and gas towards 300 euros/MWh, with brent crude now trading around the $110/bbl mark, following the European Union’s plan to cease using Russian oil and products by year end. U.S. President Joe Biden announced plans to allow expanded sales of higher-ethanol gasoline in an effort to lower fuel prices in April, but drivers are not likely to see gasoline prices dip in the short term, as inflationary pressures are set to keep costs elevated.

The backdrop of spiking inflation and rising rates poses downside risks to growth in the near-term.

Joe Lupton

Global Economist, J.P. Morgan

Inflation is spiking to levels not seen since the early 1980s, while increasingly hawkish central bank guidance is leading to a steep tightening in borrowing costs. In developed markets, inflation is set to surge 7.6% annualized in the first half of 2022, the highest in nearly 40 years.

“The backdrop of spiking inflation and rising rates poses downside risks to growth in the near-term,” said Joe Lupton, Global Economist at J.P. Morgan Research.

Developed market consumer spending growth looks to have stalled last quarter and is at risk of remaining week in the current quarter. The immediate threat to higher inflation and weaker growth comes from the surge in commodity prices. Oil prices in March stood 70% above their year-ago levels and are projected to remain near the current level into mid-year.

The average across regions suggests global natural gas prices in March are 360% higher than year-ago levels. However, in Europe, where the stress is most acute, TTF natural gas prices in March surged a stunning 640% since a year ago. At the same time, global agriculture prices have jumped 40% since mid-2021.

Beyond commodity prices, inflationary pressures have been building for over a year now. Even if the geopolitical crisis eases, inflation is likely to stay elevated. However, while remaining higher than pre-pandemic norms, inflation is likely to fall sharply from the current multi-decade highs after mid-year. “If our forecast is right,” notes Lupton, “inflation could fall sharply in 2H22 and allow the strong fundamentals of robust job growth, rising wages, and healthy balance sheets to boost spending.”

Food prices are also rising for consumers

As well as gasoline prices, food costs have also soared, as record high prices in the key staple markets of wheat and corn and vegetable oils are passed onto consumers at the checkout. Russia and Ukraine usually account for 30% of wheat on the world market, along with 80% of sunflower oil, while Ukraine alone supplies 20% of the corn sold internationally.

Ukraine’s logistical challenges are likely to leave agricultural trade flows in disarray for some time. The first half of the calendar year is a seasonally weak period of wheat exports from the Black Sea, but pre-committed sales of Russian wheat are leaving ports. It is typically a more active period for corn and sunflower oil, however—and these exports from Ukraine are not flowing.

New crop sales have been very limited, and it is difficult to tell whether importers are being cautious on price or origin. Ukrainian seaports remain closed, preventing meaningful export flows, while the upcoming corn and sunflower planting seasons remain in jeopardy.

“We hold concerns for the consistent availability of corn and sunflower oil exports through the peak period of shipments in the second half of this year,” said Tracey Allen, Agricultural Commodities Strategist at J.P. Morgan Research.

Ukrainian seaports remain closed and only 50% of corn exports had been shipped pre-conflict

Pre-conflict, Ukraine’s 2021/2022 corn export volumes were broadly in line with 2020/2021, 2019/2020 and the five-year average. However, meaningful export has ceased due to port closures.

According to Ukraine’s Ministry for Agrarian Policy and Food, spring crops have been planted on 4.7 million hectares, accounting for over 30% of intended area as of May 2nd. The Ukrainian Agribusiness Club has estimated that 70% of 2021 area could be planted. Planting of the major spring crops corn and sunflowers are likely approaching the halfway mark, having been reported at 37% complete on 2 million hectares and 2.4 million hectares, respectively, on May 2nd.

“The Ministry has published a very useful account on farming on the front line of the conflict, a stark reminder of the reality for Ukrainian farmers, risking their lives in an effort to feed their country and the world. While there is no shortage of challenges to overcome, the planting effort is one of national priority. Diesel supply shortages remain a primary issue – particularly in the east. More widespread however is the challenge of accessing farm credit, particularly in an environment of rising domestic agricultural inventories as seaports remain closed, hampering export sales indefinitely,” said Allen.

Are food prices set to keep rising?

Price rises are likely to continue, as mounting inflationary pressures stemming from food markets and supply-side risks are now becoming inevitabilities as the conflict persists.

Adding further complications to the unprecedented supply side challenges for agricultural markets, La Niña is lingering for longer than originally projected and now threatens U.S. spring crops, after wreaking havoc across South American grain and oilseed production earlier in the year.

In yet another extension, the National Oceanic and Atmospheric Administration (NOAA) now suggests that the seasonal climate pattern entrenched for much of the last two years, which drives rainfall and temperature anomalies across the Tropical Pacific, will persist through the Northern Hemisphere summer. Climate models suggest that there are even chances of a La Niña state lingering through the autumn – which must be monitored for new season Latin American crops. The combination of elevated fertilizer and input prices with uncertainty over fertilizer application rates in a La Niña seasonal pattern raises important questions for U.S. yield potential and abandonment rates.

“Drought is already entrenched across the U.S. Plains – typical of a La Niña winter. The outlook according to our in-house meteorologist suggests that this will likely intensify into early summer, particularly across the Southwest, parts of the Plains and Texas, weighing on yield potential for winter wheat, cotton and corn particularly. We continue to see further upside price risks for milling wheat amid persistent challenging growing conditions in the U.S.,” said Allen.

Corn remains the market most physically exposed of agricultural commodities to the Russian conflict in Ukraine and to shortage risks on a longer-term basis, due to challenges for the imminent spring planting in Ukraine (April – May).

We hold concerns for the consistent availability of corn and sunflower oil exports through the peak period of shipments in the second half of this year.

Tracey Allen

Agricultural commodities strategist, J.P. Morgan

However, wheat prices are expected to rise the most of all agricultural markets over the coming months, potentially by more than an additional 40%, as consumers have limited forward coverage and are buying hand to mouth amid a deteriorating production outlook.

Equally, vegetable oil markets have a more bullish outlook after the shock decision of Indonesia to ban edible oil exports from April 28th - including palm oil, which will draw on global soybean oil and rapeseed exports as replacement oils. This adds to the existing loss of Ukrainian sunflower oil exports on the world market.

J.P. Morgan maintains its forecast for 23 million tonnes of Ukrainian corn exports for 2021/22 ending September, albeit with caution. New crop production remains the primary risk with the planting season opening through April and May.

“To reach our 23 million tonne 2021/22 export forecast, one million tonnes of corn (approaching maximum line capacity) would have to be exported each month for the remaining five of the marketing year,” added Allen.

Related insights

-

From market outlooks and economic forecasts to commodities deep dives and equity research, J.P. Morgan Global Research provides industry-leading analysis from market experts & analysts.

-

Global Research

The Russia-Ukraine crisis: What does it mean for markets?

March 22, 2022

Explore the macro and market implications of the Russia-Ukraine conflict with J.P. Morgan Global Research.

This communication is provided for information purposes only. Please read J.P. Morgan research reports related to its contents for more information, including important disclosures. JPMorgan Chase & Co. or its affiliates and/or subsidiaries (collectively, J.P. Morgan) normally make a market and trade as principal in securities, other financial products and other asset classes that may be discussed in this communication.

This communication has been prepared based upon information, including market prices, data and other information, from sources believed to be reliable, but J.P. Morgan does not warrant its completeness or accuracy except with respect to any disclosures relative to J.P. Morgan and/or its affiliates and an analyst's involvement with any company (or security, other financial product or other asset class) that may be the subject of this communication. Any opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This communication is not intended as an offer or solicitation for the purchase or sale of any financial instrument. J.P. Morgan Research does not provide individually tailored investment advice. Any opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. You must make your own independent decisions regarding any securities, financial instruments or strategies mentioned or related to the information herein. Periodic updates may be provided on companies, issuers or industries based on specific developments or announcements, market conditions or any other publicly available information. However, J.P. Morgan may be restricted from updating information contained in this communication for regulatory or other reasons. Clients should contact analysts and execute transactions through a J.P. Morgan subsidiary or affiliate in their home jurisdiction unless governing law permits otherwise.

This communication may not be redistributed or retransmitted, in whole or in part, or in any form or manner, without the express written consent of J.P. Morgan. Any unauthorized use or disclosure is prohibited. Receipt and review of this information constitutes your agreement not to redistribute or retransmit the contents and information contained in this communication without first obtaining express permission from an authorized officer of J.P. Morgan.