State of the exit market report: Europe, Middle East and Africa

Mergers and acquisitions remain the primary exit avenue for EMEA venture-backed companies, while IPOs fall to a decade low.

Mergers and acquisitions remain the primary exit avenue for EMEA venture-backed companies, while IPOs fall to a decade low.

October 06, 2025

M&A dominates EMEA venture exits, U.S. buyers lead

Across EMEA, mergers and acquisitions (M&A) continue to be the primary exit strategy for venture-backed companies. M&A accounts for over 85% of venture-backed exits in the last five years. U.S.-based companies have emerged as the leading acquirers of EMEA startups, driven by their desire to expand into new markets, products and geographies. While corporations predominantly lead these acquisitions, venture-backed companies are becoming increasingly active in the EMEA market.

In contrast, EMEA-based, venture-backed companies going public are at a decade low. This decline is influenced by factors such as geopolitics, economic uncertainty and market volatility, which have collectively dampened investor sentiment. Although recent venture-backed IPO valuations have shown signs of recovery, the number of companies listing remains limited.

The market's ability to accommodate larger IPOs is a positive sign, even though overall activity remains subdued. Despite the general outperformance of U.S. stock markets compared to those in EMEA, the stock prices of venture-backed companies in both regions tend to decline over time. This trend persists regardless of whether companies meet the Rule of 40. The challenging market conditions have contributed to a slowdown in venture-backed IPOs since 2021. In response, secondary activity has increased, as these transactions can help bridge the liquidity gap.

As venture-backed companies consider going public, two important factors to consider are selecting a suitable exchange to list on and preparing a corporate governance plan. Preparation is also crucial for founders, as there are several financial, operational and personal considerations to think through to ensure a well-planned exit.

- Roshan Wijayarathna, Co-Head of Innovation Economy, EMEA

Gabor Pogany, Co-Head of Innovation Economy, EMEA

Alex McCracken, Head of Venture Capital Relationships, EMEA

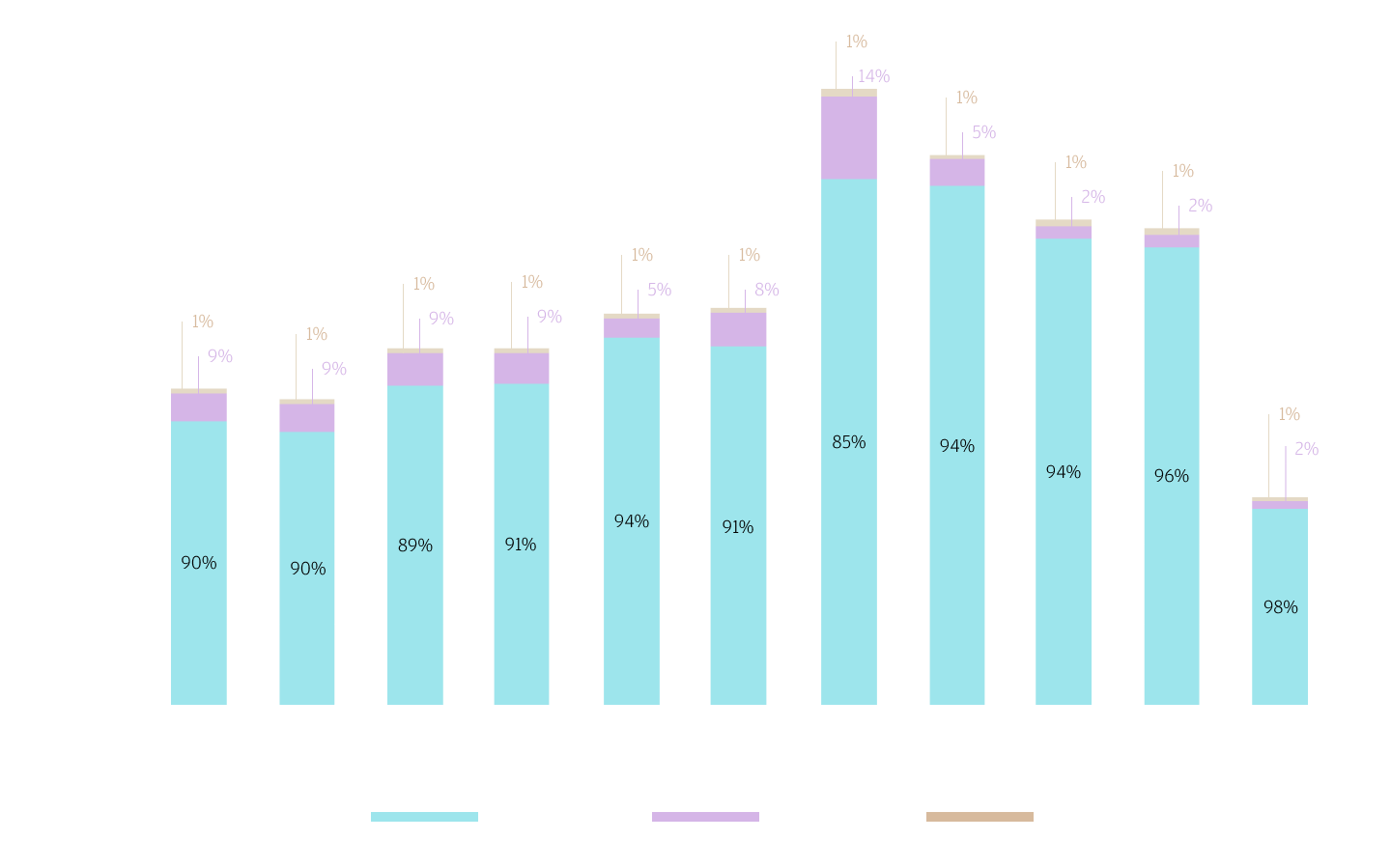

M&A remains the primary exit strategy for venture-backed, EMEA-based companies—accounting for over 85% of venture-backed exits in the last five years. Although activity is healthy, startups are taking longer to exit via M&A, surpassing the time to exit via IPO in 2022. Most acquiring companies are based in the U.S., with the remainder spread across Europe.

Meanwhile, the number of EMEA-based companies going public is at a decade low. Geopolitics, economic uncertainty and market volatility have all contributed to dampened investor sentiment, creating a challenging backdrop.

EMEA-based, venture-backed company exit by count type

Stacked bar chart showing exit strategies for EMEA venture-backed startups from 2015 to first half 2025. Each bar is divided into three segments representing M&A (light blue, largest portion), IPO (purple, middle section), and Buyout (dark teal, smallest section). M&A dominates throughout, growing from 90% in 2015 to 98% in H1 2025. IPOs peaked at 14% in 2021 but declined sharply to just 2% by 2024 and H1 2025. Buyouts remain minimal at 1% or less across all years. Bar heights suggest deal activity was lowest in 2015-2018 at around 800 deals, increased significantly through 2021-2022 reaching approximately 1,500 deals, then declined in 2023-2024 before dropping to around 500 deals in H1 2025. The chart demonstrates a clear trend toward M&A as the preferred exit strategy, with public offerings becoming increasingly rare in recent years.

32%

S&P 500 market capitalization in the IT sector

8%

STOXX 600 market capitalization in the IT sector

1%

FTSE market capitalization in the IT sector

Strong governance is key to smooth exits

Startups are often characterized by their "work fast and break things" culture. However, as they expand and move toward an exit strategy, such as a merger, acquisition or IPO, the demand for strong corporate governance becomes increasingly important. Effective corporate governance can attract investors, mitigate risks, enhance trust among investors and buyers, and facilitate a smoother and more successful exit. Governance practices typically evolve alongside the company, with the board adapting to the startup's stage and requirements. Therefore, it’s important to plan ahead for effective governance, as poor governance can result in undesirable consequences, including loss of shareholder value, legal liabilities and diminished market share.

| Select board decision areas | Questions to ask |

|---|---|

| Listing jurisdiction (in case of an IPO) | Where should the company be listed? |

| Size and leadership | What size should the board be? And who should occupy Board leadership positions? (board chair, committee chairs) |

| Independence | How independent should the board be? |

| Diversity | How diverse should the board be? (gender, nationality, age) |

| Expertise | What are the current and likely future needs of the business and what skills will directors need? (technical, industry, etc.) |

| Committees | What committees should be established? (legally required, other) And what specific director skills are needed for each committee? |

Download the report

Hide

Download the report

Hide