Contributors

Managing Director, Head of Wealth Planning and Advice, J.P. Morgan Wealth Management

Associate, Wealth Planning & Advice

When putting together an estate plan or any financial plan, you and your tax and legal advisors should consider the various different state laws that could impact the plan in addition to federal laws. Here are some important items to think about for individuals with ties to New York State.

Estate taxes and calculation of estate taxes

New York is one of 15 states (and the District of Columbia) that imposes a state level estate or inheritance tax on its residents (and even some non-resident property owners) at the time of death. This tax is in addition to the estate tax imposed by the Federal government. The top New York estate tax rate is 16%.

The New York estate tax is calculated quite differently from the Federal estate tax. Generally, for New York estate tax purposes, if the value of assets passing to beneficiaries other than a spouse or charity is below a certain threshold ($7.16 million in 2025), the assets are fully exempt from tax and no New York estate taxes will be due. However, the exemption begins to phase out at values over the threshold, and if an estate is more than 5% over the threshold (which is $7.518 million in 2025), the estate completely loses the exemption and the full value of the estate’s assets will be subject to New York estate tax. Because of this drastic drop in estate tax protection for estates over the New York threshold, the New York estate tax is often called a “cliff tax.” Estates whose values fall between the threshold amount and the 5% excess will be partially subject to New York estate tax.

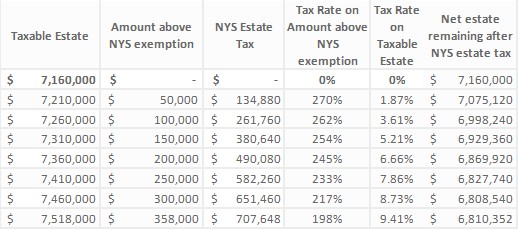

Very few people understand how this works in practice. The table below can help illustrate the impact of the New York “cliff tax” on estates valued between the threshold ($7.16 million in 2025) and 105% of that amount ($7.518 million in 2025).

Taxable estate value compared to a variety of different categories related to New York taxes

This chart shows a taxable estate value, compared with the amount above the New York State (NYS) exemption, NYC estate tax, tax rate on amount above NYC exemption, tax rate on taxable estate and net estate remaining after NYC estate tax.

- Taxable Estate: $7,160,000

- Amount above NYS exemption: $0

- NYS Estate Tax: $0

- Tax Rate on Amount above NYS exemption: 0%

- Tax Rate on Taxable Estate: 0%

- Net estate remaining after NYS estate tax: $7,160,000

- Taxable Estate: $7,210,000

- Amount above NYS exemption: $50,000

- NYS Estate Tax: $134,880

- Tax Rate on Amount above NYS exemption: 270%

- Tax Rate on Taxable Estate: 1.87%

- Net estate remaining after NYS estate tax: $7,075,120

- Taxable Estate: $7,260,000

- Amount above NYS exemption: $100,000

- NYS Estate Tax: $261,760

- Tax Rate on Amount above NYS exemption: 262%

- Tax Rate on Taxable Estate: 3.61%

- Net estate remaining after NYS estate tax: $6,998,240

- Taxable Estate: $7,310,000

- Amount above NYS exemption: $150,000

- NYS Estate Tax: $380,640

- Tax Rate on Amount above NYS exemption: 254%

- Tax Rate on Taxable Estate: 5.21%

- Net estate remaining after NYS estate tax: $6,929,360

- Taxable Estate: $7,360,000

- Amount above NYS exemption: $200,000

- NYS Estate Tax: $490,080

- Tax Rate on Amount above NYS exemption: 245%

- Tax Rate on Taxable Estate: 6.66%

- Net estate remaining after NYS estate tax: $6,869,920

- Taxable Estate: $7,410,000

- Amount above NYS exemption: $250,000

- NYS Estate Tax: $582,260

- Tax Rate on Amount above NYS exemption: 233%

- Tax Rate on Taxable Estate: 7.86%

- Net estate remaining after NYS estate tax: $6,827,740

- Taxable Estate: $7,460,000

- Amount above NYS exemption: $300,000

- NYS Estate Tax: $651,460

- Tax Rate on Amount above NYS exemption: 217%

- Tax Rate on Taxable Estate: 8.73%

- Net estate remaining after NYS estate tax: $6,808,540

- Taxable Estate: $7,518,000

- Amount above NYS exemption: $358,000

- NYS Estate Tax: $707,648

- Tax Rate on Amount above NYS exemption: 198%

- Tax Rate on Taxable Estate: 9.41%

- Net estate remaining after NYS estate tax: $6,810,352

Source: New York State, "2024 New York State Tax Return." (2024)

Speak with your J.P. Morgan and legal advisors if you’re interested in discussing strategies that can help mitigate the effects of the New York cliff tax.

Estate tax portability

Portability is the ability for married couples to aggregate their lifetime gift and estate tax exemption amounts. In practice, this means that a surviving spouse inherits any unused portion of the deceased spouse’s estate tax exemption. Portability is only available at the federal level (and only for gift and estate tax; it does not apply to the generation-skipping transfer tax.) Portability also does not apply to the New York estate tax. This means that the New York estate tax exclusion must be used by each spouse at his or her respective death; if the first spouse to die does not use his or her exclusion, it is wasted.

If the first spouse to die leaves all assets to the surviving spouse – whether directly under a will or revocable trust or because assets are held jointly with rights of survivorship – that spouse would not use up his or her exclusion amount since there is no estate tax imposed on transfers between U.S. citizen spouses. Therefore, married New Yorkers who think they may be subject to New York’s estate tax may want to structure their estate plans so that the first spouse’s exclusion is used on the first spouse’s death while still providing the surviving spouse access to the funds during his or her lifetime. Note that certain information must be filed with the IRS on the first spouse’s death in order to get the benefit of portability.

Gift tax

There is no New York gift tax, meaning that New York taxpayers can make gifts to beneficiaries during their lifetimes without the imposition of a New York gift tax. However, the value of gifts made within three years before death are included when calculating the New York estate tax, thereby imposing a “de facto” gift tax on assets given away within three years before death. A donor will need to survive for at least three years from the date of a gift to ensure that the value of a gift avoids New York estate tax upon their death. Note that there is a Federal gift tax on transfers during lifetime.

There are some exceptions to this rule, notably for real property or tangible personal property located outside of New York State. If you are concerned that you may be subject to the New York clawback, work with your tax and legal advisors to determine whether you may be able to make gifts of non-New York assets to bring your estate below the threshold.

Income tax

New York levies a state personal income tax in addition to the Federal income tax. New York applies two distinct tests to determine whether an individual is subject to the New York income tax in a given year. The first test is called the domicile test, and this covers individuals who are domiciled in New York – that is, individuals who always expect to come back to New York and treat New York as their home, regardless of whether they are physically located in New York. This is a subjective test so it is important to work with a tax advisor to understand whether you are considered domiciled in New York for New York income tax purposes.

The second test is the statutory residency test, which covers individuals who are not domiciled in New York but who both spend at least 183 days in New York and maintain a residence in New York for 10 or more months of the year. This test is more objective and should be considered with your tax advisor as you plan your income taxes each year.

Rights of spouses upon death or divorce

Death: New York typically entitles the surviving spouse to an outright one-third of a deceased spouse’s assets upon death regardless of what the deceased spouse’s estate planning documents dictate. While many spouses may decide to provide less than this in their estate planning documents (or provide assets in trust rather than outright), the surviving spouse will have the option – unless it’s been waived in a marital or other agreement – to take what is given to them in the documents or elect to take their one-third outright.

Divorce: When a couple divorces in New York, each spouse typically receives by default one-half of the couple’s marital property – that is, the assets that the couple acquired during the marriage, plus any appreciation on both the couple’s marital property and separate property. A spouse’s separate property – that is, the property with which they entered the marriage – typically will be kept by that spouse upon divorce. Inheritances and gifts are generally considered a spouse’s separate property and, unless they were converted to marital property, should be protected from division upon divorce. The application of this rule is beyond the scope of this document; you should consult a family lawyer to discuss your personal situation.

Regardless of the rights upon death or divorce in New York, spouses can negotiate different rights under a pre- or post-nuptial agreement (and often do when the defaults under New York law may not be desirable).

This article discusses only a number of the many special considerations for New York residents and taxpayers as they think about their tax, trust and estate planning. Your J.P. Morgan professional is here to partner with you and your tax and legal advisors to ensure that your wealth plan takes into account these and other important state nuances.

Connect with a Wealth Advisor

Reach out to your Wealth Advisor to discuss any considerations for your current portfolio. If you don’t have a Wealth Advisor, click here to tell us about your needs and we’ll reach out to you.

IMPORTANT INFORMATION

This material is for informational purposes only, and may inform you of certain products and services offered by J.P. Morgan’s wealth management businesses, part of JPMorgan Chase & Co. (“JPM”). Products and services described, as well as associated fees, charges and interest rates, are subject to change in accordance with the applicable account agreements and may differ among geographic locations. Not all products and services are offered at all locations. If you are a person with a disability and need additional support accessing this material, please contact your J.P. Morgan team or email us at accessibility.support@jpmorgan.com for assistance. Please read all Important Information.

GENERAL RISKS & CONSIDERATIONS. Any views, strategies or products discussed in this material may not be appropriate for all individuals and are subject to risks. Investors may get back less than they invested, and past performance is not a reliable indicator of future results. Asset allocation/diversification does not guarantee a profit or protect against loss. Nothing in this material should be relied upon in isolation for the purpose of making an investment decision. You are urged to consider carefully whether the services, products, asset classes (e.g. equities, fixed income, alternative investments, commodities, etc.) or strategies discussed are suitable to your needs. You must also consider the objectives, risks, charges, and expenses associated with an investment service, product or strategy prior to making an investment decision. For this and more complete information, including discussion of your goals/situation, contact your J.P. Morgan representative.

NON-RELIANCE. Certain information contained in this material is believed to be reliable; however, JPM does not represent or warrant its accuracy, reliability or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. No representation or warranty should be made with regard to any computations, graphs, tables, diagrams or commentary in this material, which are provided for illustration/reference purposes only. The views, opinions, estimates and strategies expressed in this material constitute our judgment based on current market conditions and are subject to change without notice. JPM assumes no duty to update any information in this material in the event that such information changes. Views, opinions, estimates and strategies expressed herein may differ from those expressed by other areas of JPM, views expressed for other purposes or in other contexts, and this material should not be regarded as a research report. Any projected results and risks are based solely on hypothetical examples cited, and actual results and risks will vary depending on specific circumstances. Forward-looking statements should not be considered as guarantees or predictions of future events.

Nothing in this document shall be construed as giving rise to any duty of care owed to, or advisory relationship with, you or any third party. Nothing in this document shall be regarded as an offer, solicitation, recommendation or advice (whether financial, accounting, legal, tax or other) given by J.P. Morgan and/or its officers or employees, irrespective of whether or not such communication was given at your request. J.P. Morgan and its affiliates and employees do not provide tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any financial transactions.

Legal Entity and Regulatory Information.

J.P. Morgan Wealth Management is a business of JPMorgan Chase & Co., which offers investment products and services through J.P. Morgan Securities LLC (JPMS), a registered broker-dealer and investment adviser, member FINRA and SIPC. Insurance products are made available through Chase Insurance Agency, Inc. (CIA), a licensed insurance agency, doing business as Chase Insurance Agency Services, Inc. in Florida. Certain custody and other services are provided by JPMorgan Chase Bank, N.A. (JPMCB). JPMS, CIA and JPMCB are affiliated companies under the common control of JPMorgan Chase & Co. Products not available in all states.

Bank deposit accounts and related services, such as checking, savings and bank lending, are offered by JPMorgan Chase Bank, N.A. Member FDIC.

This document may provide information about the brokerage and investment advisory services provided by J.P. Morgan Securities LLC (“JPMS”). The agreements entered into with JPMS, and corresponding disclosures provided with respect to the different products and services provided by JPMS (including our Form ADV disclosure brochure, if and when applicable), contain important information about the capacity in which we will be acting. You should read them all carefully. We encourage clients to speak to their JPMS representative regarding the nature of the products and services and to ask any questions they may have about the difference between brokerage and investment advisory services, including the obligation to disclose conflicts of interests and to act in the best interests of our clients.

J.P. Morgan may hold a position for itself or our other clients which may not be consistent with the information, opinions, estimates, investment strategies or views expressed in this document. JPMorgan Chase & Co. or its affiliates may hold a position or act as market maker in the financial instruments of any issuer discussed herein or act as an underwriter, placement agent, advisor or lender to such issuer.

Check the background of our firm and investment professionals on FINRA's BrokerCheck

To learn more about J. P. Morgan Wealth Management’s investment business, including our accounts, products and services, as well as our relationship with you, please review our J.P. Morgan Securities LLC Form CRS and Guide to Investment Services and Brokerage Products.

This website is for informational purposes only, and not an offer, recommendation or solicitation of any product, strategy service or transaction. Any views, strategies or products discussed on this site may not be appropriate or suitable for all individuals and are subject to risks. Prior to making any investment or financial decisions, an investor should seek individualized advice from a personal financial, legal, tax and other professional advisors that take into account all of the particular facts and circumstances of an investor's own situation.

This website may provide information about the brokerage and investment advisory services provided by J.P. Morgan Securities LLC ("JPMS"). When JPMS acts as a broker-dealer, a client's relationship with us and our duties to the client will be different in some important ways than a client's relationship with us and our duties to the client when we are acting as an investment advisor. A client should carefully read the agreements and disclosures received (including our Form ADV disclosure brochure, if and when applicable) in connection with our provision of services for important information about the capacity in which we will be acting.

INVESTMENT AND INSURANCE PRODUCTS ARE:

• NOT FDIC INSURED • NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY • NOT A DEPOSIT OR OTHER OBLIGATION OF, OR GUARANTEED BY, JPMORGAN CHASE BANK, N.A. OR ANY OF ITS AFFILIATES • SUBJECT TO INVESTMENT RISKS, INCLUDING POSSIBLE LOSS OF THE PRINCIPAL AMOUNT INVESTED

J.P. Morgan Wealth Management is a business of JPMorgan Chase & Co., which offers investment products and services through J.P. Morgan Securities LLC (JPMS), a registered broker-dealer and investment adviser, member FINRA and SIPC Insurance products are made available through Chase Insurance Agency, Inc. (CIA), a licensed insurance agency, doing business as Chase Insurance Agency Services, Inc. in Florida. Certain custody and other services are provided by JPMorgan Chase Bank, N.A. (JPMCB). JPMS, CIA and JPMCB are affiliated companies under the common control of JPMorgan Chase & Co. Products not available in all states.

Please read additional Important Information in conjunction with these pages.