Are private investments right for you?

Adding private investments to your portfolio may enhance and diversify returns.

There are structural reasons why private investments have outperformed public markets historically over medium and long terms. We believe this outperformance will continue, and here we outline a few reasons why private investments may help to achieve your long-term financial goals.

Connect with your J.P. Morgan advisor to discuss which private investments may be right for you.

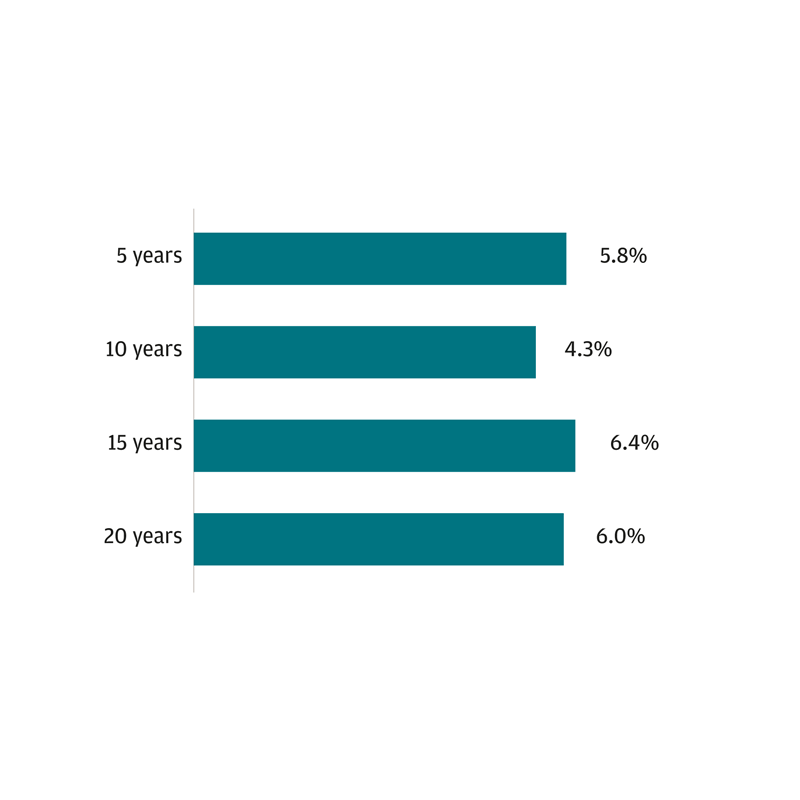

Excess Annualized Returns of Buyout/Growth Equity over the MSCI All Country World Index

Global Buyout & Growth Equity consists of global buyout and growth equity funds tracked by Cambridge Associates LLC. Indices are not investment products and may not be considered for direct involvement. Past performance is not a guarantee of future results.

Source: Cambridge Associates LLC as of June 30, 2019

Structural drivers of outperformance

Private markets have attributes that may help deliver a return premium over public market investments. A significant one is supply: Companies are opting to stay private longer, a trend that has presented more opportunities for private investment funds relative to public markets.

Once invested, private investment fund managers often are able to actively exert control over assets to attempt to fix, sell or otherwise influence them. And private markets allow for a longer-term focus and informational advantages relative to public markets.

What’s more, private investing may provide access to sectors or industries not broadly represented by public markets.

Companies are staying private longer, which has created more opportunity relative to public markets.

How do I invest?

Investors generally gain exposure to private equity, private credit and private real assets through investing in private investment funds. These are long-term, diversified, pooled investment vehicles that acquire, manage and monetize portfolios of equity or debt in privately held companies or other private real assets.

The nature of private investing

Allocating to a private investment partnership is a long-term commitment with unique cash flow patterns. Investors in private equity funds typically experience capital calls early in a fund’s lifecycle, with distributions beginning in the mid-to-late years. It is typical to have a relationship with a single fund over a 10- to 12-year period. Click on the legend box below for more information.

Importance of a strategic, active, diversified approach

An optimal private investments portfolio is diversified by fund manager, investment strategy, industry sector, market capitalization and vintage year of commitment.

Assess your investment goal, risk appetite and cash flow needs before committing to invest in the private markets. At J.P. Morgan, we can help you determine which private investments may be appropriate for your portfolios.

Want to know more about private investing? Contact your J.P. Morgan advisor to discuss how these opportunities might help you achieve your goals.

An introduction to private investments

An alternative source of opportunity and return potential

IMPORTANT INFORMATION

Securities-based lines of credit are extended at the discretion of JPMorgan Chase Bank, N.A. (“Chase Bank”) and Chase Bank has no commitment to extend a line of credit or make loans available to you under a line of credit. Any loan extended under a securities-based line of credit is subject to credit approval by Chase Bank and, if approved, the terms and conditions contained in definitive loan documentation governing the line of credit. Proceeds from a securities-based line of credit cannot be used to purchase, carry or trade securities. A line of credit collateralized by the securities in your investment account(s) involves certain risks and may not be suitable for all borrowers. Chase Bank assigns values to these securities and, at any time and without notice to you, may increase or decrease these values or change the eligibility of these securities as collateral. A decline in the value of these securities collateralizing your securities-based line of credit (whether due to a market downturn, market volatility or otherwise) directly impacts the amount of credit available to you and may require you to provide additional collateral and/or pay down your line of credit in order to avoid the forced sale of these securities by Chase Bank. The securities in your account may be sold to meet a collateral shortfall, and Chase Bank may sell your securities without contacting you. Some or all of the securities sold to meet a collateral shortfall may be sold at prices higher than their initial cost, which may result in adverse tax consequences. You should consult your tax advisor to fully understand the tax implications associated with pledging securities in connection with a loan. Please review these and other risks in more detail with your advisor, and make sure to read your line of credit documentation carefully so that you fully understand your obligations and the risks associated with this opportunity. An exercise of remedies by Chase Bank in connection with your securities-based line of credit may a ect the performance of your investment management or investment advisory account(s), and may cause such accounts to no longer conform to applicable investment guidelines. When selling securities, Chase Bank is not required to act in accordance with any fiduciary duty Chase Bank and its a liates might otherwise have as your investment manager or investment advisor. It is important to note that Chase Bank and its a liates may earn more if you borrow against your securities and other assets rather than liquidate assets to meet your cash needs. The Secured Overnight Financing Rate (“SOFR”) is a broad measure of the cost of borrowing cash overnight collateralized by U.S. Treasury securities. The SOFR is published by the Federal Reserve Bank of New York and is determined based on certain transactions in the U.S. dollar Treasury repo market. Since the SOFR is an overnight rate, it is published every Banking Day, but is e ective for the Banking Day prior to the date of publication. Refer to your definitive loan documentation for a definition of “Banking Day.” Because the SOFR is administered by the Federal Reserve Bank of New York, the Bank has no control over its determination, calculation or publication, and the Federal Reserve Bank of New York may alter the methods of calculation, publication schedule, rate revision practices or availability of the SOFR at any time without notice. The SOFR is a floating interest rate option, and changes in the SOFR can lead to a higher or lower cost of borrowing.

LEARN MORE ABOUT OUR FIRM AND INVESTMENT PROFESSIONALS AT FINRA BROKERCHECK.

To learn more about J.P. Morgan’s investment business, including our accounts, products and services, as well as our relationship with you, please review our J.P. Morgan Securities LLC Form CRS (PDF) and Guide to Investment Services and Brokerage Products.

This website is for informational purposes only, and not an offer, recommendation or solicitation of any product, strategy service or transaction. Any views, strategies or products discussed on this site may not be appropriate or suitable for all individuals and are subject to risks. Prior to making any investment or financial decisions, an investor should seek individualized advice from a personal financial, legal, tax and other professional advisors that take into account all of the particular facts and circumstances of an investor's own situation.

This website provides information about the brokerage and investment advisory services provided by J.P. Morgan Securities LLC (JPMS). When JPMS acts as a broker-dealer, a client's relationship with us and our duties to the client will be different in some important ways than a client's relationship with us and our duties to the client when we are acting as an investment advisor. A client should carefully read the agreements and disclosures received (including our Form ADV disclosure brochure, if and when applicable) in connection with our provision of services for important information about the capacity in which we will be acting.

J.P. Morgan Wealth Management is a business of JPMorgan Chase & Co., which offers investment products and services through J.P. Morgan Securities LLC (JPMS), a registered broker-dealer and investment adviser, member FINRA, and SIPC. Insurance products are made available through Chase Insurance Agency, Inc. (CIA), a licensed insurance agency, doing business as Chase Insurance Agency Services, Inc. in Florida. Certain custody and other services are provided by JPMorgan Chase Bank, N.A. (JPMCB). JPMS, CIA and JPMCB are affiliated companies under the common control of JPMorgan Chase & Co. Products not available in all states.

Bank deposit accounts, such as checking and savings, may be subject to approval. Deposit products and related services are offered by JPMorgan Chase Bank, N.A. Member FDIC.

JPMorgan Chase Bank, N.A. Member FDIC. This is not a commitment to lend. All extensions of credit are subject to credit approval. Bank products and services are offered by JPMorgan Chase Bank, N.A. and its bank affiliates.

Investments in alternative investment strategies is speculative, often involves a greater degree of risk than traditional investments including limited liquidity and limited transparency, among other factors and should only be considered by sophisticated investors with the financial capability to accept the loss of all or part of the assets devoted to such strategies.

Borrowing with securities as collateral involves certain risks, including the possibility that you may need to deposit additional securities and/or cash in the account to meet a maintenance call, and that securities in the account may be sold to meet the maintenance call. Proper management of your account and a thorough understanding of the conditions that may affect your investments will assist you in effectively using the margin lending program.

Please read additional Important Information in conjunction with these pages.

INVESTMENT AND INSURANCE PRODUCTS ARE:

• NOT FDIC INSURED • NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY • NOT A DEPOSIT OR OTHER OBLIGATION OF, OR GUARANTEED BY, JPMORGAN CHASE BANK, N.A. OR ANY OF ITS AFFILIATES • SUBJECT TO INVESTMENT RISKS, INCLUDING POSSIBLE LOSS OF THE PRINCIPAL AMOUNT INVESTED