Key takeaways

- The U.S. economy added 177,000 jobs in April, beating expectations of 138,000. However, there were net downward revisions of 58,000 to the prior two months.

- The unemployment rate remained steady at 4.2%, while average hourly earnings grew by a modest 0.2% month-over-month.

- April’s jobs report underscored the labor market’s resilience in the face of trade policy uncertainties and recent market volatility. This reinforces our strategists’ view that the Federal Reserve will keep interest rates on hold in the near-term as it evaluates how recently enacted tariffs impact the health of the economy.

- Although our strategists anticipate a slowdown in U.S. economic growth, they do not see a recession as the base case this year. For investors, they reiterate that building a resilient, diversified portfolio is key during times of elevated market volatility.

Contributors

Associate, Wealth Planning & Advice

The U.S. economy added 177,000 jobs in April, beating expectations of 138,000, according to the Bureau of Labor Statistics (BLS).1

However, there were net downward revisions of 58,000 to the prior two months. Job gains were revised down by 43,000 to 185,000 in March and down by 15,000 to 102,000 in February. Despite the latest revisions, the April jobs number raises the three-month average payroll to 155,000 from 152,000 in March.2

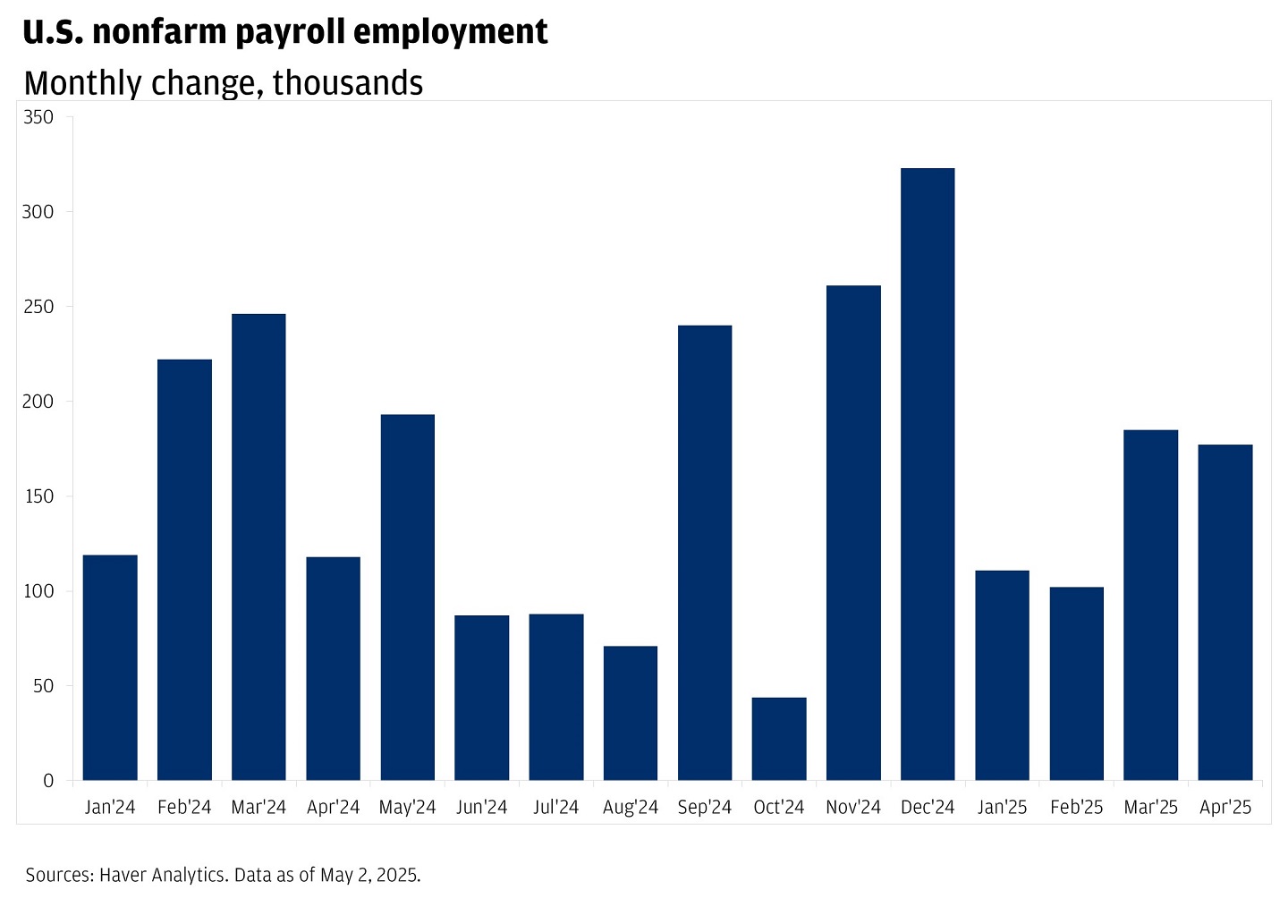

U.S. nonfarm payroll employment

Monthly change, thousands

The bar chart displays the monthly change in U.S. nonfarm payroll employment from January 2024 to April 2025. The numbers represent the change in thousands, ranging from 0 to 350. Each bar corresponds to a specific month, with the following details:

- January 2024: 119,000

- February 2024: 222,000

- March 2024: 246,000

- April 2024: 118,000

- May 2024: 193,000

- June 2024: 87,000

- July 2024: 88,000

- August 2024: 71,000

- September 2024: 240,000

- October 2024: 44,000

- November 2024: 281,000

- December 2024: 323,000

- January 2025: 111,000

- February 2025: 102,000

- March 2025: 185,000

- April 2025: 177,000

Sources: Haver Analytics. Data as of May 2, 2025.

Overall, April’s jobs report underscored the labor market’s resilience in the face of trade policy uncertainties and recent market volatility. Although our strategists anticipate a slowdown in U.S. economic growth, they still do not see a recession as the base case this year.

Sectors that gained and lost jobs

Payroll gains in April were concentrated in the health care, transportation and warehousing, social assistance and financial activities sectors.3 Notably, transportation and warehousing jobs grew by the most since December, as some businesses likely front-loaded trade in anticipation of tariffs.

Total government employment rose, boosted by state and local government employment. However, federal government jobs declined for a third consecutive month, down by 9,000. Since January, federal government employment has declined by a total of 26,000.4 This reflects continued measures from the Department of Government Efficiency (DOGE) to reduce the size of the federal civilian workforce.

Elsewhere, jobs gains were little changed or unchanged, including in mining, oil and gas extraction and manufacturing, among other industries.5

Household survey remains steady

The household survey, measuring the unemployment rate, pointed to a stable labor market. The unemployment rate was unchanged at 4.2%.6 It’s been roughly in the 4% range for the past several months, which reaffirms the labor market’s solid footing.

The labor force participation rate, which indicates the percentage of working-age individuals who are employed or actively seeking work, was little changed. It ticked up slightly from 62.5% in March to 62.6% in April, consistent with the range seen in the past few years. The participation rate for prime-age workers (ages 25 to 54) increased to the highest level in the past seven months.7

Average hourly earnings increased by a moderate 0.2% month-over-month (MoM), decelerating from a 0.3% MoM rise in March. The year-over-year change in average hourly earnings was unchanged at 3.8%, still roughly in the range of where wages have been growing for the past year.8 The latest data highlights that wages continue to grow at a healthy pace that should support near-term consumer spending.

How could the Federal Reserve (Fed) react to February 2025's jobs report?

This report reinforces our strategists’ view that the Fed will keep interest rates on hold in the near-term as it evaluates how recently enacted tariffs impact the health of the economy. Still, they expect the Fed to lower rates throughout the second half of the year.

After the upcoming Federal Open Market Committee meeting on May 6 and 7, the Fed will pay close attention to the next Consumer Price Index (CPI) release on May 13. CPI is a key inflation measure, which the Fed will use to monitor inflation’s progress towards its 2% goal.

What does February 2025's job report mean for investors?

For investors, building a resilient, diversified portfolio remains key during times of elevated market volatility.

Our strategists continue to expect slowing but positive economic growth in 2025. Going forward, investors will continue to closely monitor upcoming employment reports to examine how the labor market is reacting to recently enacted tariffs.

For investors, our strategists continue to see benefits in a globally diversified multi-asset portfolio to mitigate potential market volatility and reduce being overly exposed to any single market or event.

As always, consult with a J.P. Morgan advisor to understand how this data could impact your portfolio.

Connect with a Wealth Advisor

Reach out to your Wealth Advisor to discuss any considerations for your current portfolio. If you don’t have a Wealth Advisor, click here to tell us about your needs and we’ll reach out to you.

IMPORTANT INFORMATION

This material is for informational purposes only, and may inform you of certain products and services offered by J.P. Morgan’s wealth management businesses, part of JPMorgan Chase & Co. (“JPM”). Products and services described, as well as associated fees, charges and interest rates, are subject to change in accordance with the applicable account agreements and may differ among geographic locations. Not all products and services are offered at all locations. If you are a person with a disability and need additional support accessing this material, please contact your J.P. Morgan team or email us at accessibility.support@jpmorgan.com for assistance. Please read all Important Information.

GENERAL RISKS & CONSIDERATIONS. Any views, strategies or products discussed in this material may not be appropriate for all individuals and are subject to risks. Investors may get back less than they invested, and past performance is not a reliable indicator of future results. Asset allocation/diversification does not guarantee a profit or protect against loss. Nothing in this material should be relied upon in isolation for the purpose of making an investment decision. You are urged to consider carefully whether the services, products, asset classes (e.g. equities, fixed income, alternative investments, commodities, etc.) or strategies discussed are suitable to your needs. You must also consider the objectives, risks, charges, and expenses associated with an investment service, product or strategy prior to making an investment decision. For this and more complete information, including discussion of your goals/situation, contact your J.P. Morgan representative.

NON-RELIANCE. Certain information contained in this material is believed to be reliable; however, JPM does not represent or warrant its accuracy, reliability or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. No representation or warranty should be made with regard to any computations, graphs, tables, diagrams or commentary in this material, which are provided for illustration/reference purposes only. The views, opinions, estimates and strategies expressed in this material constitute our judgment based on current market conditions and are subject to change without notice. JPM assumes no duty to update any information in this material in the event that such information changes. Views, opinions, estimates and strategies expressed herein may differ from those expressed by other areas of JPM, views expressed for other purposes or in other contexts, and this material should not be regarded as a research report. Any projected results and risks are based solely on hypothetical examples cited, and actual results and risks will vary depending on specific circumstances. Forward-looking statements should not be considered as guarantees or predictions of future events.

Nothing in this document shall be construed as giving rise to any duty of care owed to, or advisory relationship with, you or any third party. Nothing in this document shall be regarded as an offer, solicitation, recommendation or advice (whether financial, accounting, legal, tax or other) given by J.P. Morgan and/or its officers or employees, irrespective of whether or not such communication was given at your request. J.P. Morgan and its affiliates and employees do not provide tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any financial transactions.

Legal Entity and Regulatory Information.

J.P. Morgan Wealth Management is a business of JPMorgan Chase & Co., which offers investment products and services through J.P. Morgan Securities LLC (JPMS), a registered broker-dealer and investment adviser, member FINRA and SIPC. Insurance products are made available through Chase Insurance Agency, Inc. (CIA), a licensed insurance agency, doing business as Chase Insurance Agency Services, Inc. in Florida. Certain custody and other services are provided by JPMorgan Chase Bank, N.A. (JPMCB). JPMS, CIA and JPMCB are affiliated companies under the common control of JPMorgan Chase & Co. Products not available in all states.

Bank deposit accounts and related services, such as checking, savings and bank lending, are offered by JPMorgan Chase Bank, N.A. Member FDIC.

This document may provide information about the brokerage and investment advisory services provided by J.P. Morgan Securities LLC (“JPMS”). The agreements entered into with JPMS, and corresponding disclosures provided with respect to the different products and services provided by JPMS (including our Form ADV disclosure brochure, if and when applicable), contain important information about the capacity in which we will be acting. You should read them all carefully. We encourage clients to speak to their JPMS representative regarding the nature of the products and services and to ask any questions they may have about the difference between brokerage and investment advisory services, including the obligation to disclose conflicts of interests and to act in the best interests of our clients.

J.P. Morgan may hold a position for itself or our other clients which may not be consistent with the information, opinions, estimates, investment strategies or views expressed in this document. JPMorgan Chase & Co. or its affiliates may hold a position or act as market maker in the financial instruments of any issuer discussed herein or act as an underwriter, placement agent, advisor or lender to such issuer.

Check the background of our firm and investment professionals on FINRA's BrokerCheck

To learn more about J. P. Morgan Wealth Management’s investment business, including our accounts, products and services, as well as our relationship with you, please review our J.P. Morgan Securities LLC Form CRS and Guide to Investment Services and Brokerage Products.

This website is for informational purposes only, and not an offer, recommendation or solicitation of any product, strategy service or transaction. Any views, strategies or products discussed on this site may not be appropriate or suitable for all individuals and are subject to risks. Prior to making any investment or financial decisions, an investor should seek individualized advice from a personal financial, legal, tax and other professional advisors that take into account all of the particular facts and circumstances of an investor's own situation.

This website may provide information about the brokerage and investment advisory services provided by J.P. Morgan Securities LLC ("JPMS"). When JPMS acts as a broker-dealer, a client's relationship with us and our duties to the client will be different in some important ways than a client's relationship with us and our duties to the client when we are acting as an investment advisor. A client should carefully read the agreements and disclosures received (including our Form ADV disclosure brochure, if and when applicable) in connection with our provision of services for important information about the capacity in which we will be acting.

INVESTMENT AND INSURANCE PRODUCTS ARE:

• NOT FDIC INSURED • NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY • NOT A DEPOSIT OR OTHER OBLIGATION OF, OR GUARANTEED BY, JPMORGAN CHASE BANK, N.A. OR ANY OF ITS AFFILIATES • SUBJECT TO INVESTMENT RISKS, INCLUDING POSSIBLE LOSS OF THE PRINCIPAL AMOUNT INVESTED

J.P. Morgan Wealth Management is a business of JPMorgan Chase & Co., which offers investment products and services through J.P. Morgan Securities LLC (JPMS), a registered broker-dealer and investment adviser, member FINRA and SIPC Insurance products are made available through Chase Insurance Agency, Inc. (CIA), a licensed insurance agency, doing business as Chase Insurance Agency Services, Inc. in Florida. Certain custody and other services are provided by JPMorgan Chase Bank, N.A. (JPMCB). JPMS, CIA and JPMCB are affiliated companies under the common control of JPMorgan Chase & Co. Products not available in all states.

Please read additional Important Information in conjunction with these pages.