Advanced Programmable Payments: Capital that moves on signals, not schedules1

Replace manual interventions and batch cycles with event-driven

automation that moves funds the moment your strategy says “now.”

Find out more

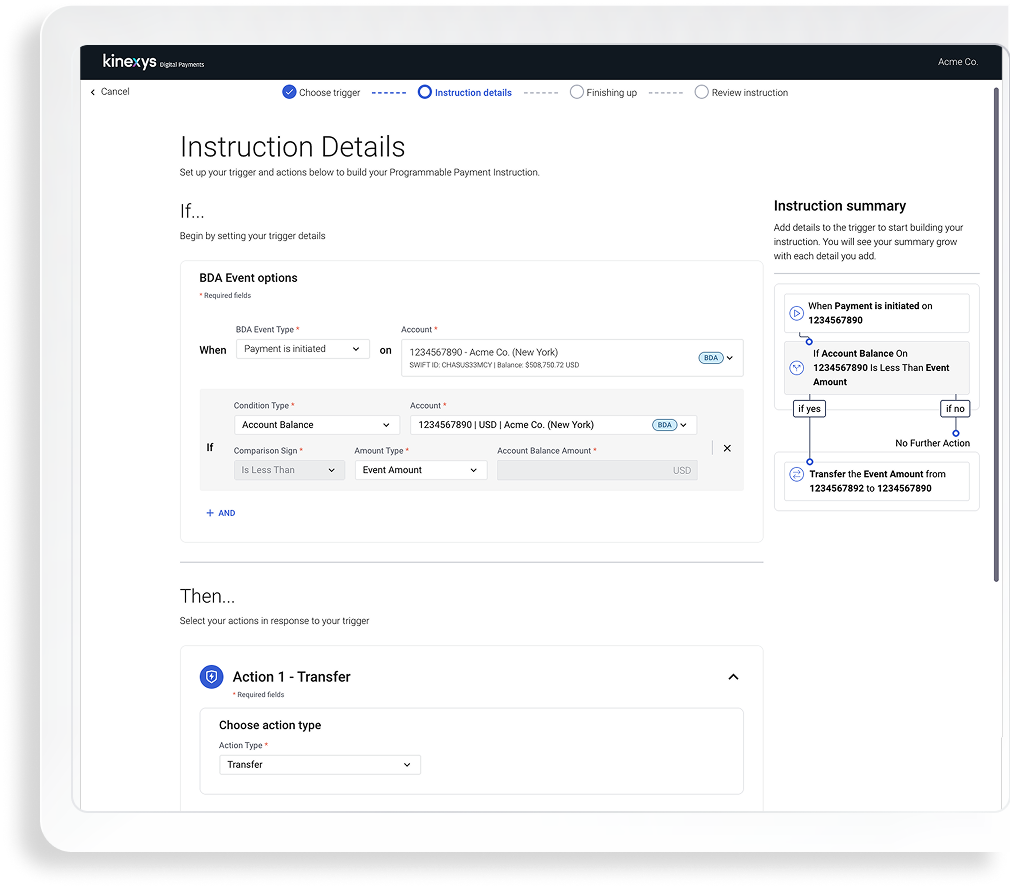

When real events occur, Programmable Payments responds according to predefined rules you set that govern how and when your money moves—such as upon receipt of a payment or when a specific date and time is reached.

Use event-driven programmability to streamline workflows, reducing manual processing, improving timeliness and lowering operational friction.

Create consistent workflows with programmable conditions that help reduce human error and improve control.

Consolidate programmable payment events and actions into an auditable history, reducing manual tracking and improving visibility across teams.