The adoption of 5G continues to surge, with a peak in 5G smartphone volumes expected in 2021E. In the future, 5G will likely provide substantial enterprise opportunity which corporates are just beginning to recognize. It is expected that 5G will exceed $180 billion in North America by 2030.

In this report, J.P. Morgan Research examines the future of 5G through the lens of consumer demand and global adoption, sharing market forecasts and exploring enterprise use cases.

Global 5G adoption: Is this the network of the future?

Globally, 119.8 million smartphones (amounting to 32% of all smartphones) were using 5G by the fourth quarter of 2020, with penetration highest in China and North America. This was up from 64.8 million (18% of all smartphones) in the third quarter of 2020.

This growth was helped by new launches such as the 5G iPhone, which saw Apple achieve a 47% share of the 5G smartphone market. 5G adoption correlated with growing smartphone sale volumes – following 1Q and 2Q troughs, volumes reached 355 million in 3Q20 and 374 million in 4Q20.

When considering the future growth of 5G adoption, consumer demand will be key as it can be monetized. For example, Korea, where current consumer demand is strong, has built out 5G enabling speeds that are three to five times faster than 4G. Consumers there are now using two to three times more data, and they’re willing to pay more for it too with an average of a 20% premium on 5G. Looking ahead, a meaningfully higher take rate is now expected, with 5G anticipated to reach 1 billion subscribers faster than the 1.5 to two years it took for 4G.

5G market forecasts

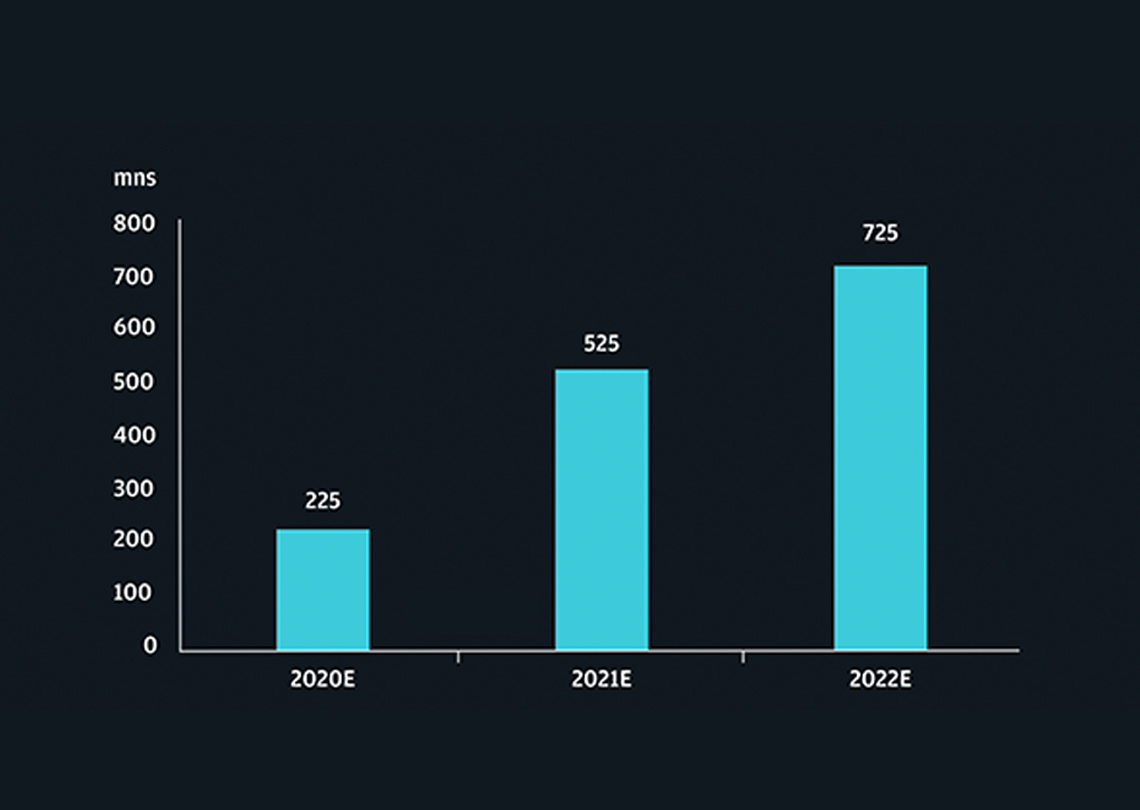

J.P. Morgan North America Equity Research predicts that 5G volume growth will peak in 2021E. “We expect a more pronounced 5G cycle with peak smartphone growth in 2021E,” said Samik Chatterjee, Telecom & Network Equipment/IT Hardware Senior Analyst at J.P. Morgan. “In 2020, we saw around 225 million 5G smartphone units sold globally. 2021 should be the biggest year in terms of growth and we expect to see a steeper ramp in volume. Growth is likely to peak relatively early, and we estimate the total number of 5G smartphone units sold during the year to reach 525 million. This will be followed by moderating increases and we would give a volume estimate of 725 million units for 2022.”

5G smartphone volume estimates

The total number of 5G smartphone units sold globally is expected to reach 725 million in 2022, up from 525 million in 2021 and 225 million in 2020.

Source: J.P. Morgan estimates.

5G market share: North East Asia leading the global adoption of 5G technology

At its Capital Markets Day, Ericsson noted that the North East Asia region has a very advanced 4G network and similar trends are expected with 5G.

-

South Korea is expanding networks following initial deployments and is expected to move to standalone 5G by the end of next year.

-

China remains aggressive in its 5G deployment. 600,000 base stations were deployed in 2020 and standalone 5G was launched by China Telecom, with other operators expected to follow soon.

-

Japan is expected to move to standalone 5G by the end of next year, with acceleration in activity expected following the iPhone launch.

Notably, 5G adoption is also expected to accelerate the Internet of Things (IoT) in the region. By 2025, Japan and South Korea are expected to see 150 million IoT connections, which is +29% in terms of compound annual growth rate (CAGR). China is expected to see 2.5 billion connections (+13% CAGR).

The future of 5G adoption: Trends in North East Asia Key upcoming developments include:

-

Standalone 5G

Already launched by China Telecom, Japan and South Korea are expected to follow soon

-

Internet of things

5G adoption will accelerate connections by up to 29% CAGR (Japan and South Korea)

-

Expanding networks

600,000 base stations were deployed in China in 2020 with more to come

-

Product launches

Activity acceleration is expected in Japan following the 5G iPhone launch

The future of 5G lies in enterprise opportunity

5G is fast becoming the network of choice due to its performance and reliability. In the future, enterprise use cases will become a primary driver for 5G growth. It is estimated that 5G will drive secular growth longer term, even beyond the 2022 timeframe, led by enterprise use cases – this differs from earlier technological transitions.

Ericsson also noted the opportunity for the enterprise market to expand at a 25% CAGR from 2022-2030 through digitalization and high performance mobile connectivity for applications, including connected vehicles, real-time automation and autonomous robotics. One notable development from 4Q20 was the acquisition of CradlePoint. This could be considered a stepping stone, preempting further organic and inorganic investment to address substantial enterprise opportunity over the next few years.

The biggest opportunity for 5G is in enterprise. Companies have only just started to scratch the surface in terms of investing in enterprise use cases. Factory floor automation will be one of the big use cases. Another is fixed wireless, which could boost connectivity through private 5G networks deployed across organizations, regions or campuses.

Samik Chatterjee

Telecom & Network Equipment/IT Hardware Senior Analyst, J.P. Morgan

What’s the scale of the opportunity for 5G enterprise solutions?

Global enterprise opportunity enabled by 5G is expected to exceed $700 billion. North America is a primary driver for enterprise opportunity which could exceed $180 billion by 2030.

Some 5G applications have been noted in the following verticals:

-

Healthcare: 16% cost reductions for healthcare workers using remote monitoring tools for patients

-

Manufacturing: operating income improvements for operators led by AR technology, robotics and autonomy

-

Energy: connectivity applications for solar technology and wind farms.

Harnessing the power of 5G holds enormous potential and many more enterprise use cases are expected to emerge across various verticals. With North America leading the way, enterprise opportunity has the power to shape the future of 5G adoption.

Related insights

-

Global Research

Global Research

Leveraging cutting-edge technology and innovative tools to bring clients industry-leading analysis and investment advice.

-

Global Research

China’s consumers show up for shopping season

January 07, 2021

In a special consumer retail spotlight, J.P. Morgan Asia Equity Research explores the trends that emerged in 2020 and what they mean for momentum in 2021, as economic recovery from COVID-19 continues and China’s “New Retail” wave gains traction.

-

Technology

The future is electric

November 17, 2020

In the past few years, the auto industry’s transformation has accelerated around the world. J.P. Morgan Global Research explores the global electric vehicle market, the key developments driving its progress and expectations for the future.

This communication is provided for information purposes only. Please read J.P. Morgan research reports related to its contents for more information, including important disclosures. JPMorgan Chase & Co. or its affiliates and/or subsidiaries (collectively, J.P. Morgan) normally make a market and trade as principal in securities, other financial products and other asset classes that may be discussed in this communication.

This communication has been prepared based upon information, including market prices, data and other information, from sources believed to be reliable, but J.P. Morgan does not warrant its completeness or accuracy except with respect to any disclosures relative to J.P. Morgan and/or its affiliates and an analyst's involvement with any company (or security, other financial product or other asset class) that may be the subject of this communication. Any opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. This communication is not intended as an offer or solicitation for the purchase or sale of any financial instrument. J.P. Morgan Research does not provide individually tailored investment advice. Any opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. You must make your own independent decisions regarding any securities, financial instruments or strategies mentioned or related to the information herein. Periodic updates may be provided on companies, issuers or industries based on specific developments or announcements, market conditions or any other publicly available information. However, J.P. Morgan may be restricted from updating information contained in this communication for regulatory or other reasons. Clients should contact analysts and execute transactions through a J.P. Morgan subsidiary or affiliate in their home jurisdiction unless governing law permits otherwise.

This communication may not be redistributed or retransmitted, in whole or in part, or in any form or manner, without the express written consent of J.P. Morgan. Any unauthorized use or disclosure is prohibited. Receipt and review of this information constitutes your agreement not to redistribute or retransmit the contents and information contained in this communication without first obtaining express permission from an authorized officer of J.P. Morgan. Copyright 2021 JPMorgan Chase & Co. All rights reserved.

MSCI: The MSCI sourced information is the exclusive property of MSCI. Without prior written permission of MSCI, this information and any other MSCI intellectual property may not be reproduced, redisseminated or used to create any financial products, including any indices. This information is provided on an ‘as is’ basis. The user assumes the entire risk of any use made of this information. MSCI, its affiliates and any third party involved in, or related to, computing or compiling the information hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of this information. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in, or related to, computing or compiling the information have any liability for any damages of any kind. MSCI and the MSCI indexes are services marks of MSCI and its affiliates.